We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

45 years NI contributions required for full state pension?

Comments

-

The question asked is "why 45 years" when the maximum, according to this site, is 44.

Please read links in my post above - this may clarify matters.

0 -

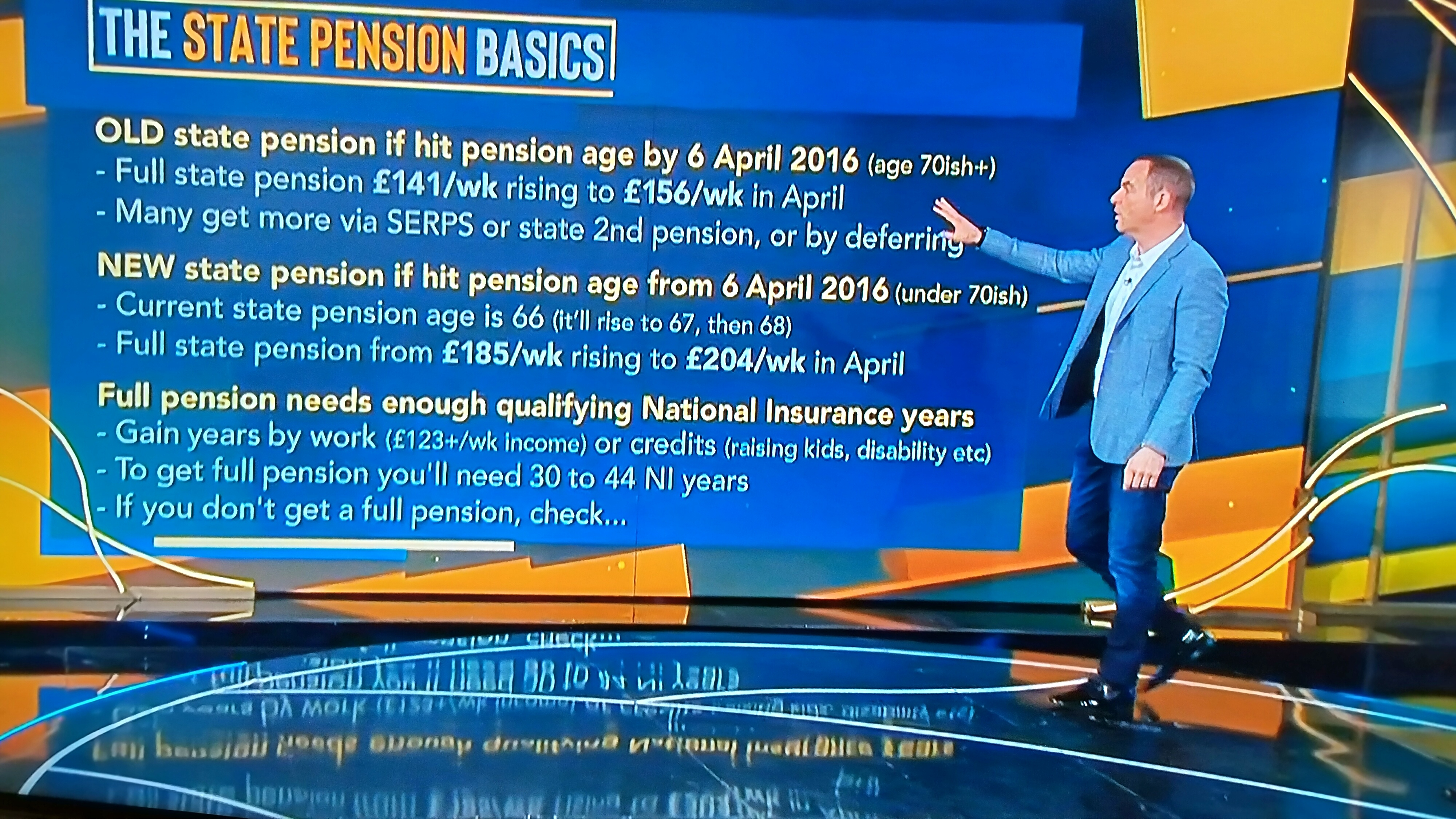

Plus the fact that under the old rules, it's the BASIC state pension that's £141.85 a week (if you're going to round, Martin, be consistent - why is £141.85 rounded down to £141, but £203.85 rounded up to £204?).Dazed_and_C0nfused said:

No it's not, there are other factual inaccuracies with that graphic. For example,Billportland said:I should've posted this pic in the OP, would've maybe kept the answers on subject.

The confusing part is "to get full pension you'll need 30-44 years". Appears not to be true according to several posts.

The standard new State Pension is £185.15/week not £185.

From April 2023 it will be £203.85/week, not £204.

You could get to £185.15 with less than 30 years.

Calling it the FULL state pension leads to the misunderstanding that is all everyone under the old rules got, when in fact many got much more than that with SERPS/S2P, leading to the 'hard done by/unfair ' complaints we see on this board from time to time.

Now I remember why I never watch the program - my blood pressure couldn't take it...2 -

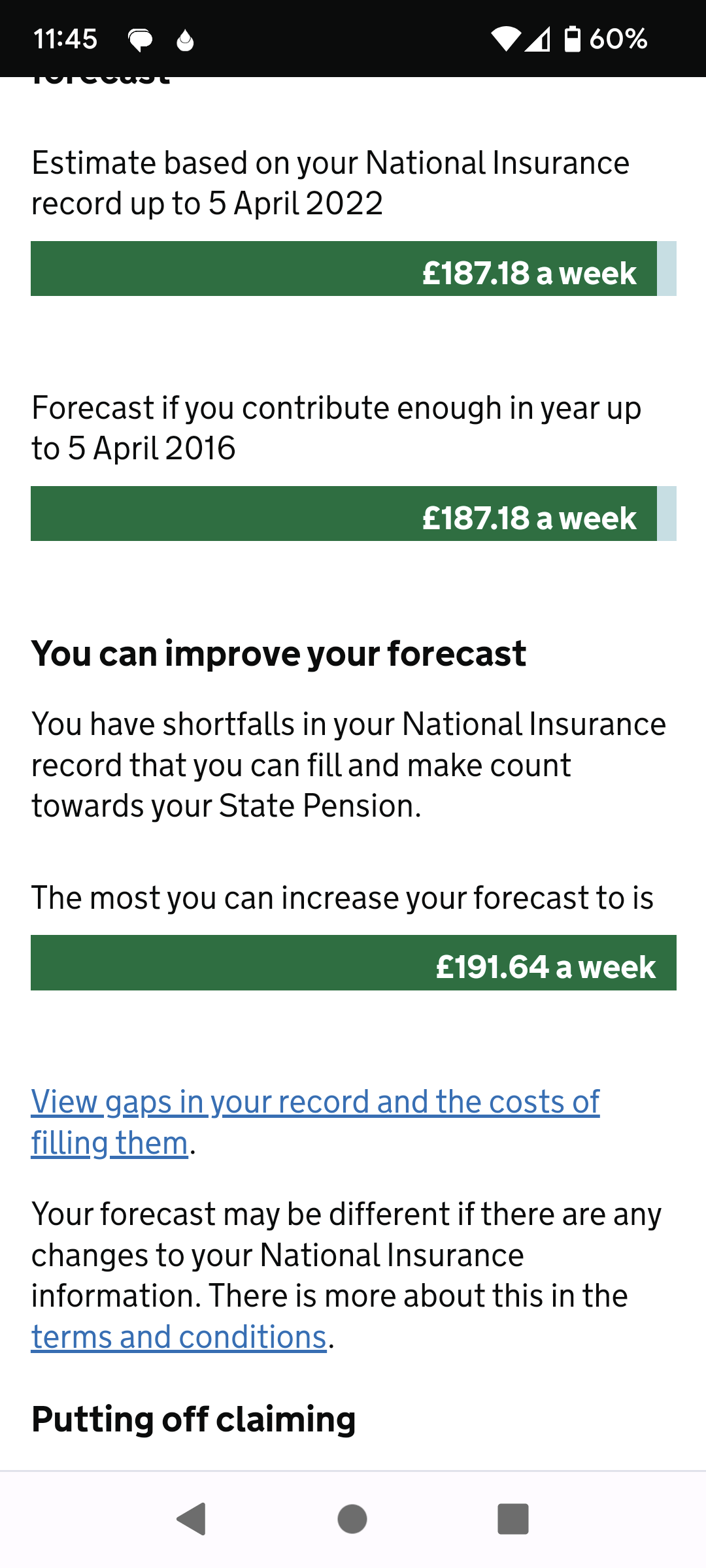

Here's two screen shots of what mine says today. I currently have 31 years paid, and reach S.P.A. in 2025.

0 -

Billportland said:Billportland said:

The question asked is "why 45 years" when the maximum, according to this site, is 44.zagfles said:Because she was in a contracted out occupational scheme which took over responsibility for paying part of the state pension and got NI rebates to do so.Search the forum, the same question is asked every week.I should've posted this pic in the OP, would've maybe kept the answers on subject.

The confusing part is "to get full pension you'll need 30-44 years". Appears not to be true according to several posts.

Martin Lewis has nothing to do with this site - he sold it in 2012.0 -

That's quite an unusual one.eastcorkram said:Here's two screen shots of what mine says today. I currently have 31 years paid, and reach S.P.A. in 2025.

The fact that you current have more than the £185.15 maximum indicates that you had already reached that amount by April 2016 and so have a 'protected payment'. I presume that it must be the possibility of filling the additional year 2006-2007 that would result in the further increase (earlier years are no longer available to buy, and you only have until April to buy 2006-7).

In contrast to what we tell a lot of people on these boards, in this particular case, post-2016 years aren't going to increase your forecast any further (but you have to continue to pay NI until you reach State Retirement Age if you are working)2 -

I have 43 years of full contributions and an estimate of £158.68 for a SRA of April 2027, suggesting something like 49 years for a 'full' pension ... It definitely is complicated but who said anything in this life is fair?Debt Free Wannabe by 1 December 2027

Satisfied customer of Octopus Agile - past savings on average 33% of standard tarrif

Deep seated hatred of Scottish Power and all who sail in her - would love to see Ofgem grow a pair and actually do something about it.1 -

True, I suspect there will be some people who don't like the fact you have (almost certainly) paid reduced NI for many years but now have the chance to increase your State Pension.MikeyPGT said:I have 43 years of full contributions and an estimate of £158.68 for a SRA of April 2027, suggesting something like 49 years for a 'full' pension ... It definitely is complicated but who said anything in this life is fair?

But that's not your concern, you've probably just struck gold with the transitional rules.5 -

Dazed_and_C0nfused said:

True, I suspect there will be some people who don't like the fact you have (almost certainly) paid reduced NI for many years but now have the chance to increase your State Pension.MikeyPGT said:I have 43 years of full contributions and an estimate of £158.68 for a SRA of April 2027, suggesting something like 49 years for a 'full' pension ... It definitely is complicated but who said anything in this life is fair?

But that's not your concern, you've probably just struck gold with the transitional rules.It's strange how the big winners from the transition always seem to be ones who always come on here complaining "it's not's fair" etc whereas the losers don't, probably because the vast majority don't realise they're losers!4 -

That's quite an unusual one.

And has been discussed on previous occasions!

https://forums.moneysavingexpert.com/discussion/comment/78998704/#Comment_78998704

https://forums.moneysavingexpert.com/discussion/comment/79803882/#Comment_79803882

And I think that she was pointed in the direction of

https://www.dpf.org.uk/explorer/files/TOPPING-UP-YOUR-STATE-PENSION-GUIDE.pdf and notes.

I wonder did eastcorkram ever follow the suggestion made a year or so back to do as this poster and get chapter and verse from DWP?

https://forums.moneysavingexpert.com/discussion/comment/79394659/#Comment_79394659

1 -

eastcorkram said:Here's two screen shots of what mine says today. I currently have 31 years paid, and reach S.P.A. in 2025.I hope you are arranging to pay that gap ( which if had been done before the 2019 "soft" cut off would have cost a mere £392.60 !)And as for "it's complicated", note the increase is only £4.46 where we normally state a pre 2016 year will add £4.73

")

Never associate with idiots on their own level, because, being an intelligent man, you'll try to deal with them on their level - and on their level they'll beat you every time.

Being hated by idiots is the price you pay for not being one of them.

Jean Cocteau 1889-1963

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards