We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Is my Pension Pot too Small?

Comments

-

I tend to “guess” based upon my own experience of my own investing and historical factual figures.

FTSE100 7.8% annualised total return for example (1984-2019).

Anyhow, we don’t have crystal balls so best to have low, mid and high scenarios; guess you’re more pessimistic than I.0 -

The 7.8% has to be minus inflation over the same period, to give a meaningful result.ader42 said:I tend to “guess” based upon my own experience of my own investing and historical factual figures.

FTSE100 7.8% annualised total return for example (1984-2019).

Anyhow, we don’t have crystal balls so best to have low, mid and high scenarios; guess you’re more pessimistic than I.0 -

I want between 2 and 3 times that and I don’t think my lifestyle is extravanganrt so doesnt it all boil down to what you want? As it could be £330 or it could be £990k?kinger101 said:

Seems we "guess" in very similar ways as if I change it to 60, it also comes out around £330K.Albermarle said:

In an earlier post I 'guessed' at a pot of £330,000 at age 60 (also in real terms, )so we are approx in the same area.kinger101 said:

Planning using a 7% growth rate is a little optimistic, and you have not factored in inflation.ader42 said:Finger in the air maths…

Current pot is £73k, expecting to pay in circa £7k a year for 15 years, gives a pot of approx. £200k

You can hope the pot doubles in size over that time period (around 7% growth) so becoming approx £400k.

£400k would buy a pension of about £16k a year.

That’s assuming you hope to retire at age 55 of course. If retiring at state pension age then you are in a much better position.

All predictions will be wrong, but they do need to be useful (NB they cannot access pensions at 55 anyway).

I plan growth at 2.5% above inflation, which by my calculations would give OP an inflation adjusted pot of around £420K at 67. At a drawdown rate of 3.5% pa, would mean £14,700 pa. On top of state pension of ca. £9650 per year, then I'd say OP's plans are reasonable to give the a strong plan for a comfortable retirement at state pension age. But it would be useful if they can work out their expenditure too. Of course, I'll be wrong too, but hopefully wrong in a more useful way.0 -

These values more or less described my spreadsheet exactly! I use a return rate of 80% of my SIPP's 3 year historical annualised growth rate.bd10 said:My personal assumptions are: long term inflation rate of 3% and for asset returns 5-6% nominal. For 2023 I am using 6.3% inflation, 4-5% for 2024 and then 3% thereafter. As you will notice, my nominal equity returns are below historical averages and here I make a judgement call to err on the cautious side. The era of QE and cheap money is over, we have an accelerating demographic change to deal with, re-shoring of supply chains keeping the costs higher and thus corporate profits lower and last but not least the huge costs of trying to achieve net zero. So I end up using 2-3% real returns which may sound poor and I may be well below the actual returns which we may see in the future, totally agree. Who knows. But here's the thing: I am more likely to over-save than under-save and if I keep at my own pace of aggressive savings I may be able to retire a few years before 65 instead of being overly optimistic and then realising I am behind target.You can have a look at Vanguard's returns outlook, even Jack Bogle had a chapter partially dedicated to that in his Little Book of Common Sense Investing. Credit Suisse's outlooks are similar to both as well.0 -

With this approach, does that mean that the pension contributions have to increase with inflation each year to get the calculated inflation adjusted pot?kinger101 said:

Planning using a 7% growth rate is a little optimistic, and you have not factored in inflation.ader42 said:Finger in the air maths…

Current pot is £73k, expecting to pay in circa £7k a year for 15 years, gives a pot of approx. £200k

You can hope the pot doubles in size over that time period (around 7% growth) so becoming approx £400k.

£400k would buy a pension of about £16k a year.

That’s assuming you hope to retire at age 55 of course. If retiring at state pension age then you are in a much better position.

All predictions will be wrong, but they do need to be useful (NB they cannot access pensions at 55 anyway).

I plan growth at 2.5% above inflation, which by my calculations would give OP an inflation adjusted pot of around £420K at 67. At a drawdown rate of 3.5% pa, would mean £14,700 pa. On top of state pension of ca. £9650 per year, then I'd say OP's plans are reasonable to give the a strong plan for a comfortable retirement at state pension age. But it would be useful if they can work out their expenditure too. Of course, I'll be wrong too, but hopefully wrong in a more useful way.

0 -

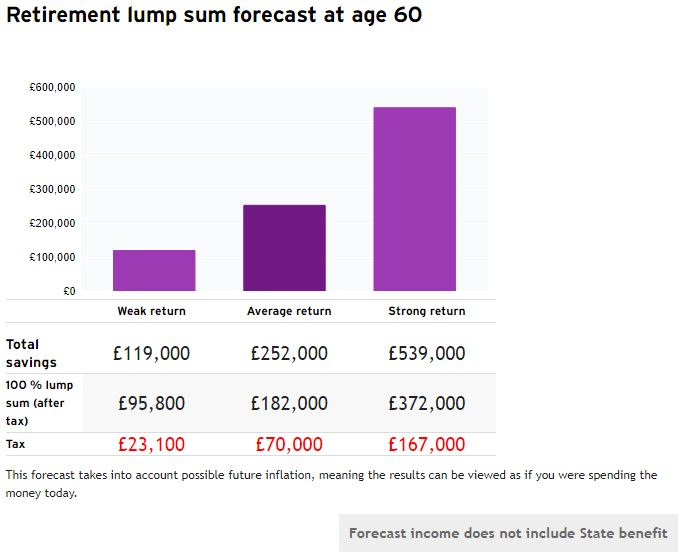

I have been spending some time looking into my pension pot and I have discovered the follow:

1. Weak Return preddiction = £118k, average return = £251k and strong return = £538k. The following caveat is included:

This forecast takes into account possible future inflation, meaning the results can be viewed as if you were spending the money today.

2. AVC + Pre97 SCC + Core ER Contributions + Transfer in contributions + ER Matching Contributions + EE Saver Contributions - Growth Fund (Drawdown L/S). I do not know what any of this means.

3. I wish to transfer some savings across to my pot, I assume this is allowed without any penalties?

4. I just realised I worked for a company in 2013 but I have not accessed their pension pot. I assume there would be one as it was a government requirement at this stage?

0 -

I wish to transfer some savings across to my pot, I assume this is allowed without any penalties?

It is only worth transferring savings into a pension if you will get tax relief on them. So it depends on your earnings as you can only get tax relief up to 100% of your earnings.

So as a simple example.

You earn £30K pa before tax.

Your total contributions to a pension should not exceed £30K including tax relief. It does not matter whether you make the contributions from earnings, or from savings, or a mixture of the two.

If you are a higher earner than that, and there are employer contributions as well, there are other limits.

Pensions: Everything you need to know for retirement - MSE (moneysavingexpert.com)

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.8K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards