We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Guide discussion: Plan 5 student loans

Comments

-

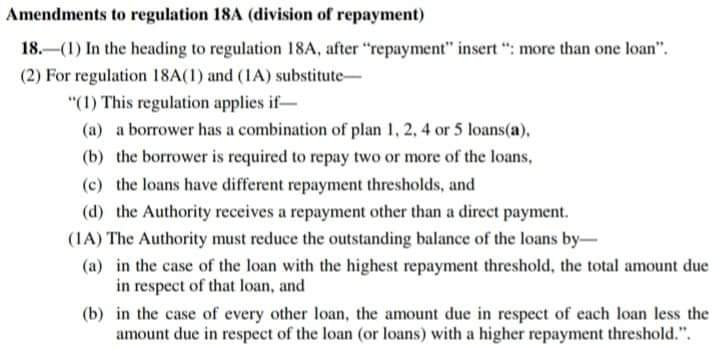

No you pay back 9% over the lowest repayment threshold and the repayments are divided between the loan balances as follows:magpie294 said:If you've already got a plan 2 loan and take out a plan 5 loan (e.g. for a PGCE course) will you have to pay back both loans at the same time once you're above the thresholds?

So if you earn £35000 would you pay back 9% of £10000 on plan 5 PLUS 9% of approx £7700 on plan 2?

0 -

I haven't read the detail but suspect it will work the same ways as if you have plan 1 and plan 2 in that your total deductions are still 9% bot if you breach both plans earnings thresholds the repayments are shared across both.

Note that this is different with postgraduate loans, these have their own earnings threshold and repayment rate of 6% which is paid in addition to any undergraduate loan repayments.0 -

Is there a logic to take the biggest loan you can on the basis that whatever income you are on (unless very large) the '9% tax' you pay towards the loan means it is unlikely you repay it all? For example if you take a masters course over 4 or 5 years the loan taken is much larger and this more unlikely (for more people) it will be repaid?

Also the opposite seems true, taking a smaller loan means all earning levels (unless under £25k) are more likely to repay it over the 40 years.....

Thus the best strategy is to borrow as much as possible unless you go into a high paying profession? Even if you later get it wrong and your child moves into a highly paid job, you then (and only then) pay it down?0 -

I agree. You need to go for one extreme or the other. Take everything you can if you are going to be a relatively low or middle earner, take as little as possible if you are confident you will pay it all back.MarkSSS said:Is there a logic to take the biggest loan you can on the basis that whatever income you are on (unless very large) the '9% tax' you pay towards the loan means it is unlikely you repay it all? For example if you take a masters course over 4 or 5 years the loan taken is much larger and this more unlikely (for more people) it will be repaid?

Also the opposite seems true, taking a smaller loan means all earning levels (unless under £25k) are more likely to repay it over the 40 years.....

Thus the best strategy is to borrow as much as possible unless you go into a high paying profession? Even if you later get it wrong and your child moves into a highly paid job, you then (and only then) pay it down?

The problem is that no one can see the future. You need to be a consistent high earner to repay all the loan plus you need inflation to be at a long term low rate, otherwise salary increases will mean you become a higher earner relative to your loan repayments sooner.

There is also the issue of whether you should use a lump sum as a house deposit or pension contribution to reap long term benefits vs loan repayment.I'm a Forum Ambassador on the housing, mortgages & student money saving boards. I volunteer to help get your forum questions answered and keep the forum running smoothly. Forum Ambassadors are not moderators and don't read every post. If you spot an illegal or inappropriate post then please report it to forumteam@moneysavingexpert.com (it's not part of my role to deal with this). Any views are mine and not the official line of MoneySavingExpert.com.0 -

Hi,I posted similar previously but i think put it in the right place. This board seems much more appropriate!My son is wanting to go to uni, but the huge debt is putting him off.I have explained how they work, and it's like a tax blah blah...We are both trying to work out if it is indeed much better to pay off ASAP with the new plan 5 loans being 40years?He will be living at home so loan will be 27k tuition fees for 3 year degree.He will work plenty and plans to pay £300 per month off during the 1st 2 years then maybe less for 3rd year.We could then look at getting a lower rate loan or 0% credit card transfers if available.Does this make sense to do? It appears the cheapest way of doing it to me! The student loan will soon rack up interest at 7%.I imagine he will be a mid earner (40k ish) working full time for most of the following 40y.Views & ideas welcome!0

-

Personally, if I had cash I wanted to spend on my offspring I would be thinking about a house deposit rather than a student loan.hulkgti said:Hi,I posted similar previously but i think put it in the right place. This board seems much more appropriate!My son is wanting to go to uni, but the huge debt is putting him off.I have explained how they work, and it's like a tax blah blah...We are both trying to work out if it is indeed much better to pay off ASAP with the new plan 5 loans being 40years?He will be living at home so loan will be 27k tuition fees for 3 year degree.He will work plenty and plans to pay £300 per month off during the 1st 2 years then maybe less for 3rd year.We could then look at getting a lower rate loan or 0% credit card transfers if available.Does this make sense to do? It appears the cheapest way of doing it to me! The student loan will soon rack up interest at 7%.I imagine he will be a mid earner (40k ish) working full time for most of the following 40y.Views & ideas welcome!

If in any way it will be a struggle or you could make better use of the money, don't think of clearing the loan or not taking it.

The worst option could be to take some of the loan and not all of it. The repayments will be the same until you get to a point where the loan is cleared, if you never get to that point your loan is written off, you could have had more loan money for no cost.I'm a Forum Ambassador on the housing, mortgages & student money saving boards. I volunteer to help get your forum questions answered and keep the forum running smoothly. Forum Ambassadors are not moderators and don't read every post. If you spot an illegal or inappropriate post then please report it to forumteam@moneysavingexpert.com (it's not part of my role to deal with this). Any views are mine and not the official line of MoneySavingExpert.com.1 -

The interest rate is linked to inflation so while it is high at the moment, it will fall in future years probably to around 2-3%.hulkgti said:Hi,I posted similar previously but i think put it in the right place. This board seems much more appropriate!My son is wanting to go to uni, but the huge debt is putting him off.I have explained how they work, and it's like a tax blah blah...We are both trying to work out if it is indeed much better to pay off ASAP with the new plan 5 loans being 40years?He will be living at home so loan will be 27k tuition fees for 3 year degree.He will work plenty and plans to pay £300 per month off during the 1st 2 years then maybe less for 3rd year.We could then look at getting a lower rate loan or 0% credit card transfers if available.Does this make sense to do? It appears the cheapest way of doing it to me! The student loan will soon rack up interest at 7%.I imagine he will be a mid earner (40k ish) working full time for most of the following 40y.Views & ideas welcome!0 -

hulkgti said:Hi,I posted similar previously but i think put it in the right place. This board seems much more appropriate!My son is wanting to go to uni, but the huge debt is putting him off.I have explained how they work, and it's like a tax blah blah...We are both trying to work out if it is indeed much better to pay off ASAP with the new plan 5 loans being 40years?He will be living at home so loan will be 27k tuition fees for 3 year degree.He will work plenty and plans to pay £300 per month off during the 1st 2 years then maybe less for 3rd year.We could then look at getting a lower rate loan or 0% credit card transfers if available.Does this make sense to do? It appears the cheapest way of doing it to me! The student loan will soon rack up interest at 7%.I imagine he will be a mid earner (40k ish) working full time for most of the following 40y.Views & ideas welcome!

The change in repayment schedule up to forty years has definitely changed the landscape somewhat. Unlike Plan 2 loans, Plan 5 loan repayments will continue through someone's 50's, traditionally the period where someone is at maximum earning potential. This is one major factor in why the number of student loans repaid in full are expected to increase from around 15% to 50%

Given all that, I still think it's important to reinforce the fact that it does operate like a tax in that your son will only ever repay anything if their earning. We can all have life and career paths planned out and try to calculate to the n'th degree about what would be the best (cheapest) option, but forty years is awfully long time for life to throw a curve ball and change those best laid plans. .

For that reason I totally agree with @Silvercar, If you want to help your son and can do so, I think helping with something towards a house deposit is a far better option than overpaying a student loan that he may not ever repay anyway.

Definitely don't take out other loans or credit cards to pay off the student loans, that's the worst thing you could do.0 -

My son is going to university this September. He has applied for student loan and we are aiming to borrow maximum amount allowed. Anything I save now for him, instead of paying for university costs, will go to a fund to help him with housing after uni. He will need to manage housing no matter what, whilst paying back the student loan is dependable on income (so yes it is just like paying graduation tax/ contribution).I am still wondering how we normally manage the timing of student loan versus renting payment. My son starts in early September, meaning he should be in the hall from 1 Sep, paying perhaps before, but the first maintenance loan goes to his account on 9 Sep. And we may need to pay half a year in advance, which is higher than the first installment of the loan. Anyone has experience or idea how to manage this? Do parents pay the half year rent, then the student pays back when they receive the loan? We aim for the maintenance loan to cover rent plus travel, books, emergencies. I as parent to up by paying for food shopping each week.0

-

If this is university owned student halls, I would expect that the payments tie in with the loan dates. As many, many students wouldn’t be able to make the payments otherwise.LL_USS said:My son is going to university this September. He has applied for student loan and we are aiming to borrow maximum amount allowed. Anything I save now for him, instead of paying for university costs, will go to a fund to help him with housing after uni. He will need to manage housing no matter what, whilst paying back the student loan is dependable on income (so yes it is just like paying graduation tax/ contribution).I am still wondering how we normally manage the timing of student loan versus renting payment. My son starts in early September, meaning he should be in the hall from 1 Sep, paying perhaps before, but the first maintenance loan goes to his account on 9 Sep. And we may need to pay half a year in advance, which is higher than the first installment of the loan. Anyone has experience or idea how to manage this? Do parents pay the half year rent, then the student pays back when they receive the loan? We aim for the maintenance loan to cover rent plus travel, books, emergencies. I as parent to up by paying for food shopping each week.I'm a Forum Ambassador on the housing, mortgages & student money saving boards. I volunteer to help get your forum questions answered and keep the forum running smoothly. Forum Ambassadors are not moderators and don't read every post. If you spot an illegal or inappropriate post then please report it to forumteam@moneysavingexpert.com (it's not part of my role to deal with this). Any views are mine and not the official line of MoneySavingExpert.com.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.6K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.7K Work, Benefits & Business

- 603.2K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards