We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Which of the following lenders is likely to give the highest limit?

Comments

-

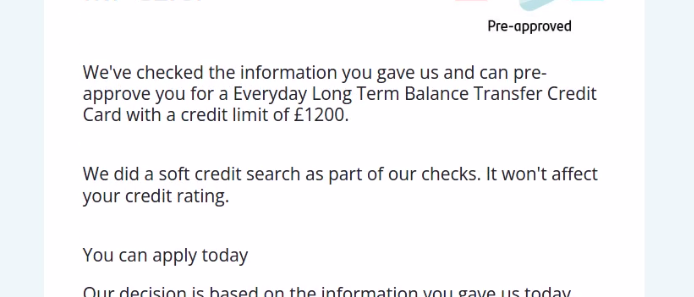

blue.peter said:I'm not at all sure that you should pay any attention to that £1,200 figure. I've often seen it used simply as an illustrative figure, by different banks, and then found that the actual limit offered was higher. I think that it's simply a standard number used as a basis for illustrating costs. Here, for example, is a screenshot from NatWest's:

No no, that was after their eligibility check...

EPICA - the best symphonic metal band in the world !0 -

No, they do not. I have a fairly good experience of dealing with underwriters questioning balances already paid off, accounts closed, not seeing the difference about paid in full monthly and rolling balances, even could not recognise their own issues credit card from the Experian query they had in front of them..Alex9384 said:Marchitiello said:Aside of the reputation that MBNA and Barclaycard had in the past of being very generous with their initial limits, my experience in the recent past made me conclude that post Covid even more of a factor is definitely your total Credit limit across all your card provider and obviously your utilisation, but assuming the same amount of credit use on a rolling basis, the same provider has offered me about £15k when my total credit limit was about 120% of my annual income and about 1/3 of the above when my total credit limits across all cards was just above 150% of my income. I appreciate that depending on credit profile no everyone will get to this level of credit lines, but you would potentially know what is likely to be (mine has been over 110% of my income more or less for 15 years at least.So I would say if your existing credit portfolio means you are already towards the top of your total credit limit profile for most lenders, that is when you get limits of £1200 or even less when on other cards you may have 10 times that.

unfortunately, if the new credit line is needed fairly urgently, closing an unused Card to create extra room for a new card limit won’t help as it will take 2/3 months to actually update properly on your credit file.

My combined credit limits across 6 cards were exactly 2x my gross annual income until the end of December when I closed 7k Amex CC.

I thought lenders see these changes much sooner than you can see it yourself on your free credit reports?1 -

Marchitiello said:

No, they do not. I have a fairly good experience of dealing with underwriters questioning balances already paid off, accounts closed, not seeing the difference about paid in full monthly and rolling balances, even could not recognise their own issues credit card from the Experian query they had in front of them..Alex9384 said:Marchitiello said:Aside of the reputation that MBNA and Barclaycard had in the past of being very generous with their initial limits, my experience in the recent past made me conclude that post Covid even more of a factor is definitely your total Credit limit across all your card provider and obviously your utilisation, but assuming the same amount of credit use on a rolling basis, the same provider has offered me about £15k when my total credit limit was about 120% of my annual income and about 1/3 of the above when my total credit limits across all cards was just above 150% of my income. I appreciate that depending on credit profile no everyone will get to this level of credit lines, but you would potentially know what is likely to be (mine has been over 110% of my income more or less for 15 years at least.So I would say if your existing credit portfolio means you are already towards the top of your total credit limit profile for most lenders, that is when you get limits of £1200 or even less when on other cards you may have 10 times that.

unfortunately, if the new credit line is needed fairly urgently, closing an unused Card to create extra room for a new card limit won’t help as it will take 2/3 months to actually update properly on your credit file.

My combined credit limits across 6 cards were exactly 2x my gross annual income until the end of December when I closed 7k Amex CC.

I thought lenders see these changes much sooner than you can see it yourself on your free credit reports?A quotation search will be a 'live' snapshot of the credit bureau's records at the time of the search (unlike say MSE Credit Club, Clearscore etc which will typically only search once a week/month).The issue is that your existing lenders might only update the bureau monthly (and the update they provide may also have a lag).1 -

Yes, the issue is that lenders often update Monthly, but I can assure you the debate we had via the Personal banker (I was talking to him whilst he was in conference with the underwriters and I could hear the stupidity…) demonstrated that the data was not current and that some of the things we assume are visible to lenders, actually are not..WillPS said:Marchitiello said:

No, they do not. I have a fairly good experience of dealing with underwriters questioning balances already paid off, accounts closed, not seeing the difference about paid in full monthly and rolling balances, even could not recognise their own issues credit card from the Experian query they had in front of them..Alex9384 said:Marchitiello said:Aside of the reputation that MBNA and Barclaycard had in the past of being very generous with their initial limits, my experience in the recent past made me conclude that post Covid even more of a factor is definitely your total Credit limit across all your card provider and obviously your utilisation, but assuming the same amount of credit use on a rolling basis, the same provider has offered me about £15k when my total credit limit was about 120% of my annual income and about 1/3 of the above when my total credit limits across all cards was just above 150% of my income. I appreciate that depending on credit profile no everyone will get to this level of credit lines, but you would potentially know what is likely to be (mine has been over 110% of my income more or less for 15 years at least.So I would say if your existing credit portfolio means you are already towards the top of your total credit limit profile for most lenders, that is when you get limits of £1200 or even less when on other cards you may have 10 times that.

unfortunately, if the new credit line is needed fairly urgently, closing an unused Card to create extra room for a new card limit won’t help as it will take 2/3 months to actually update properly on your credit file.

My combined credit limits across 6 cards were exactly 2x my gross annual income until the end of December when I closed 7k Amex CC.

I thought lenders see these changes much sooner than you can see it yourself on your free credit reports?A quotation search will be a 'live' snapshot of the credit bureau's records at the time of the search (unlike say MSE Credit Club, Clearscore etc which will typically only search once a week/month).The issue is that your existing lenders might only update the bureau monthly (and the update they provide may also have a lag).1 -

Oh, fair enough. Pure coincidence that it matched the commonly-used illustrative number. Yep, that's certainly well into the range that I'd consider very poor.Alex9384 said:

No no, that was after their eligibility check...

0 -

I think you may find that is not a estimate of your limit, but a guide amount ALL lenders use to show the interest rates & payments.Alex9384 said:

I know no one can tell for sure, but those of you who have applied for many credit cards over years might want to share their experience.

I'm going to do a balance transfer and I'm looking at these:

Sainsbury's

Virgin

Santander

M&SNot sure if I should try TSB as they don't have an eligibility checker.

Santander gave me an estimate of lousy 1200 credit limit which is quite useless and far lower than any of my existing cards.Life in the slow lane0 -

born_again said:I think you may find that is not a estimate of your limit, but a guide amount ALL lenders use to show the interest rates & payments.

No.. I know what you mean, but this is not the case.See my other post to blue.peter, including screenshot.EPICA - the best symphonic metal band in the world !0 -

The days when 10k limits were the norm......0

-

i tend to find banks you already have a connection with like a bank account etc gives you much better credit limits

they know what money goes through the account i bank with halifax and lloyds mostly but my oldest bank is tsb

i started to use tsb bank far more over the past 2 years and when i actually finally did apply for a tsb credit card i got 11k cc limit which is nearly twice what my other banks gave me they have also just increased my limit again 6 months after it was opened but only slightly. so i'd try the banks you already have an account with.

0 -

I've found the opposite, as in the ones I haven't been a banking with are most generous.

Amex gave me a £12k limit, which was about five times the limit my bank had offered on their standard credit card.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards