We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Credit file skullduggery

Markp46

Posts: 4 Newbie

Can anyone tell me if this is right/allowed.

It's from Provident Personal finance, I'm sure people are aware of the back story of all this and payday loans but when they liquidated the just marked it as satisfied rather then removing it.

I missed the time frame for compensation and when I've emailed them they basically say there is nothing they can do now as the remedy period is over.

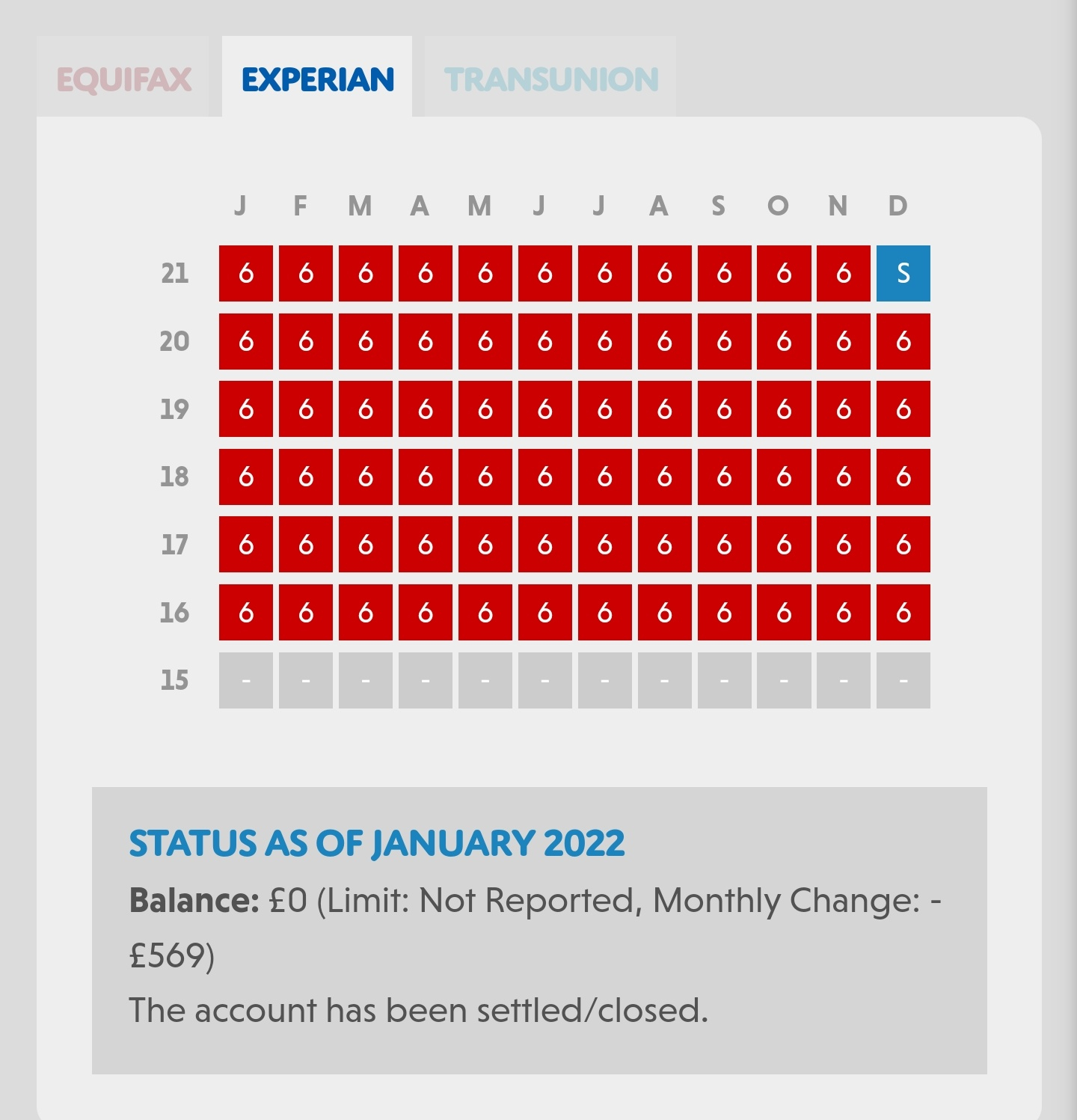

Question is shouldn't this have defaulted years ago and dropped off credit file by now not been reported as 6 miss payments for 72 months straight?

How can I put this right if the company refuses to do anything and says it's not their problem.

It's from Provident Personal finance, I'm sure people are aware of the back story of all this and payday loans but when they liquidated the just marked it as satisfied rather then removing it.

I missed the time frame for compensation and when I've emailed them they basically say there is nothing they can do now as the remedy period is over.

Question is shouldn't this have defaulted years ago and dropped off credit file by now not been reported as 6 miss payments for 72 months straight?

How can I put this right if the company refuses to do anything and says it's not their problem.

0

Comments

-

Ok, I know it's a bit strange for someone to come back and answer their own question but I see alot of people have viewed this but not got a response yet so I turned to ChatGPT.

I explained the situation to it and after some careful prompts I got it to draft me an email I could send to the credit ref agencies. Which I will post below.I am writing to dispute the inaccurate information that is currently being reported on my credit file by Provident Personal Finance. I understand that Provident Personal Finance has reported that I have missed six payments on a loan every month for 71 months, and then reported the account as settled. This information is not accurate and I would like it to be removed from my credit file as soon as possible.I have attempted to contact Provident Personal Finance to resolve this issue but they have refused to help stating that the remedy period has passed.According to the Financial Conduct Authority (FCA) guidelines, credit providers are required to take appropriate action when a customer falls behind on their repayments. Specifically, the FCA requires credit providers to report a customer as being in default if they have taken reasonable steps to help the customer get back on track, and the customer has failed to take advantage of those steps. In this case, Provident Personal Finance has failed to report the loan as defaulted after six missed payments, which is a clear violation of the FCA guidelines and does not reflect the true state of the loan. This is not only unfair to me, but it also negatively impacts my credit score now and does not accurately represent my creditworthiness to potential lenders.Furthermore, reporting missed payments indefinitely without issuing it as a default is not in compliance with the Data Protection Act 1998 and the General Data Protection Regulation, which requires credit reference agencies to conduct a reasonable investigation when a consumer disputes information on their credit file. As such, Provident Personal Finance's actions in this case do not adhere to the legal framework established by these regulations.Defaulting on a loan is a clear indication that the loan is no longer in good standing and that the lender has taken steps to collect or recover the debt. Not reporting the loan as defaulted after six missed payments implies that the loan is still in good standing and does not reflect the borrower's inability to repay the debt.I kindly ask you to investigate this matter and remove the inaccurate information from my credit file as soon as possible. I would appreciate your prompt attention to this matter and look forward to hearing from you soon.Thank you for your time and consideration.Sincerely,

[Name]

Don't get me wrong this is not an air tight arguement but it's alot better then what I could of come up with, anyway if anyone has a similar problem hopefully this helps them. I will send this too all three major credit agencies and report back the results.0 -

Report them to the Information Commissioners Office for reporting incorrect data1

-

It's not an air-tight argument because an AI bot just sent you a load of word salad.Markp46 said:Ok, I know it's a bit strange for someone to come back and answer their own question but I see alot of people have viewed this but not got a response yet so I turned to ChatGPT.

I explained the situation to it and after some careful prompts I got it to draft me an email I could send to the credit ref agencies. Which I will post below.I am writing to dispute the inaccurate information that is currently being reported on my credit file by Provident Personal Finance. I understand that Provident Personal Finance has reported that I have missed six payments on a loan every month for 71 months, and then reported the account as settled. This information is not accurate and I would like it to be removed from my credit file as soon as possible.I have attempted to contact Provident Personal Finance to resolve this issue but they have refused to help stating that the remedy period has passed.According to the Financial Conduct Authority (FCA) guidelines, credit providers are required to take appropriate action when a customer falls behind on their repayments. Specifically, the FCA requires credit providers to report a customer as being in default if they have taken reasonable steps to help the customer get back on track, and the customer has failed to take advantage of those steps. In this case, Provident Personal Finance has failed to report the loan as defaulted after six missed payments, which is a clear violation of the FCA guidelines and does not reflect the true state of the loan. This is not only unfair to me, but it also negatively impacts my credit score now and does not accurately represent my creditworthiness to potential lenders.Furthermore, reporting missed payments indefinitely without issuing it as a default is not in compliance with the Data Protection Act 1998 and the General Data Protection Regulation, which requires credit reference agencies to conduct a reasonable investigation when a consumer disputes information on their credit file. As such, Provident Personal Finance's actions in this case do not adhere to the legal framework established by these regulations.Defaulting on a loan is a clear indication that the loan is no longer in good standing and that the lender has taken steps to collect or recover the debt. Not reporting the loan as defaulted after six missed payments implies that the loan is still in good standing and does not reflect the borrower's inability to repay the debt.I kindly ask you to investigate this matter and remove the inaccurate information from my credit file as soon as possible. I would appreciate your prompt attention to this matter and look forward to hearing from you soon.Thank you for your time and consideration.Sincerely,

[Name]

Don't get me wrong this is not an air tight arguement but it's alot better then what I could of come up with, anyway if anyone has a similar problem hopefully this helps them. I will send this too all three major credit agencies and report back the results.

No disrespect here but if the best you can come up with is a load of guff from an AI, what are you going to do when a human says "that isn't right?" What is your retort going to be?

You've given no information as to your personal circumstances so nobody can realistically give you ay advice.0 -

You need to understand your argument if you're going to make it to a human being, even the stupidest CS representative is going to tell you to stop talking if you quote all that to them.

It's meaningless drivel, but it does look impressive.0 -

Just some follow up, I decided not the send the "word salade" in its current form and did some more research.I do 100% agree that the ChatGPT thing isn't completely accurate but it is a good tool to give you some ideas on how to argue your case but you do need to check it's a valid argument and find the actual legal framework to make sure it's legit.

In this case it was mostly accurate but it's actually the information commissioner's office (ICO) that publishes the guidelines relating to how defaults and missed payments should be registered with the CRAs.

I used what the ChatGPT gave me as a starting point and added in more accurate and relevant information and sent it to provident.

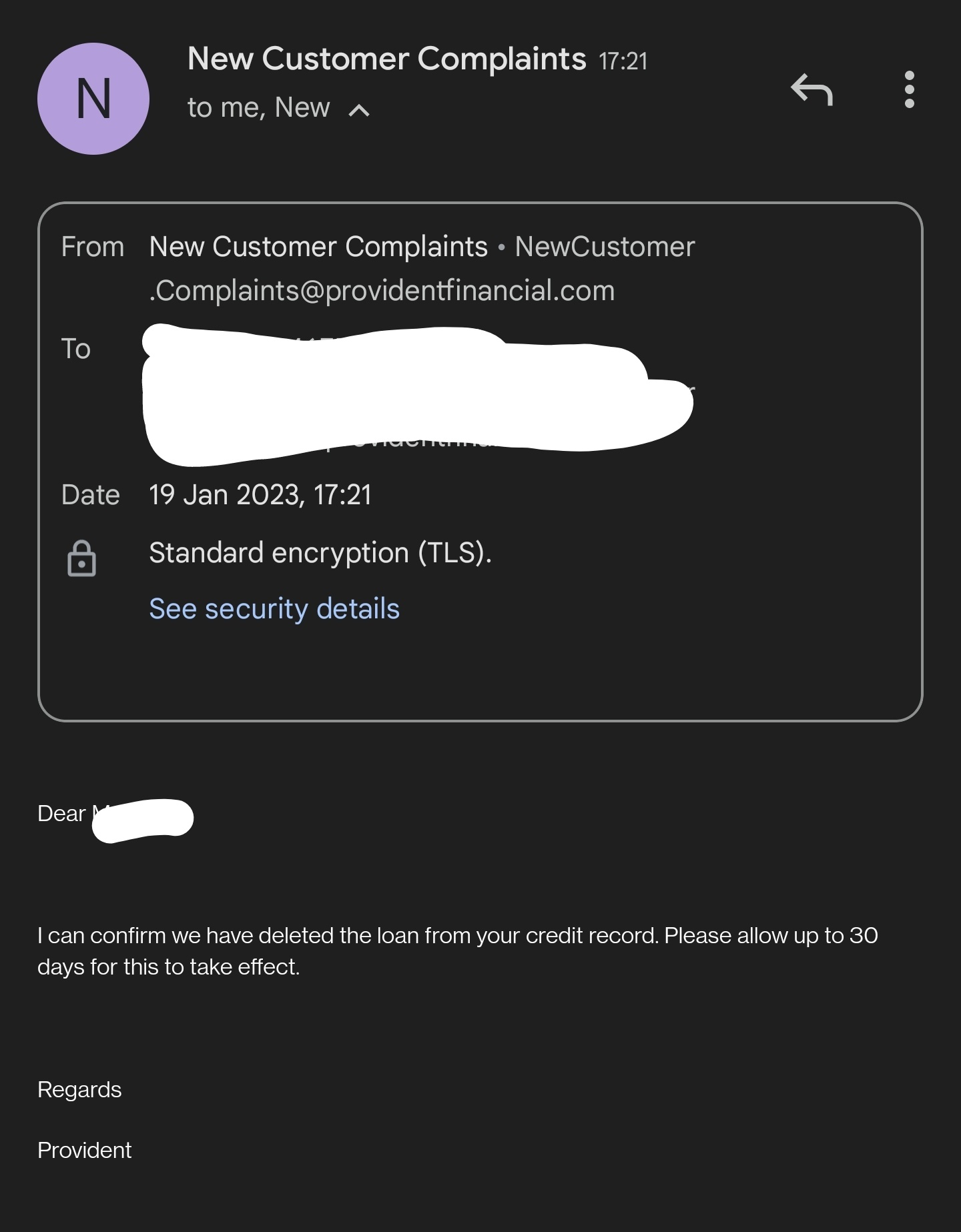

I have just received an email back from them and they are completely removing the report from my credit file (great success!)

I will post the email I sent Provident below and their response to it, so if anyone has a similar problem with their credit file they can use it as a start point in their own argument to have the information removed.*I am writing to dispute the inaccurate information that is currently being reported to the Credit Reporting Agency [CRA] by Provident Personal Finance. I understand that Provident Personal Finance has reported that I have missed six payments on my loan, but they have reported the same information for 71 months straight, when they should have reported it as a default after the 6th missed payment, the loan is now reported as settled but this doesnt remove all the incorrectly reported missed payments.The way this information has been presented to the CRA is not inline with the Information Commissioner's Office [ICO] legal framework, when the loan was past 6 missed payments the loan should have been reported as a default. If this had been done properly and you had followed the guidance as outlined by the ICO then the loan would have dropped off my credit file by now.Defaulting on a loan is a clear indication that the loan is no longer in good standing and that the lender has taken steps to collect or recover the debt. Not reporting the loan as defaulted after six missed payments implies that the loan is still in good standing or an agreement had been made [which it hadn't] failure to report the default does not reflect the borrower's inability to repay the debt.Below I have extracted the relevant guidance from the ICO which relates to my complaint and why I think the information has been reported wrong to the CRA and not inline with the ICOInformation Commissioner's Office [ICO]Principles for the Reporting of Arrears, Arrangements and Defaults at Credit Reference AgenciesThe basis of the principles is that; Lenders that supply data to the CRAs are required to ensure that the data is accurate, up to date and meets agreed quality standards.Principle 2:2. Should a payment not be made as expected, information to reflect this will be recorded on your credit file If you do not make your regular expected payment by the agreed time and/or for the agreed amount according to your terms and conditions, the account may be reported to the CRAs as being in arrears. If this continues over time, the level of reported arrears will increase, which may result in the lender taking some form of action. This could include notification of their intention to report the account as “defaulted”Reporting of arrears over time.Arrears should generally only increase by one month at a time e.g. status code 1 to 2, 2 to 3 etc. There can be exceptions to this such as fraud, bankruptcy, county court judgments [CCJs], returned cheques or direct debits.Principle 4:4. If you fall into arrears on your account, or you do not keep to the revised terms of an arrangement, a default may be recorded to show that the relationship has broken down. As a general guide, this may occur when you are 3 months in arrears, and normally by the time you are 6 months in arrears.A default should not be filed:If you make a payment, in time, that fully meets the terms set out in the default noticeIf jointly with the lender an agreement is reached for an arrangement and you keep to the terms of that arrangementIf the amount outstanding is solely made up of fees or chargesIf a lender is given evidence that a customer is deceased [for example a verifiable death certificate, probate or letter of administration.This means the CRA should show the loan as 1,2,3,4,5,6,D under normal circumstances.currently it shows it as 1,2,3,4,5,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6,6..... you get the picture.if you believe that this is reported accurately, then i want to know what special circumstances you are using to justify why the loan was not reported as defaulted.As you can see from the document it is very clear that after 6 missed payments the loan should have defaulted unless there were special circumstances, which there wasn't.It is for this reason I request my credit file is updated to show the loan defaulted after the 6th missed payment as this would be the appropriate time frame, this would also mean the loan is no longer on my credit file.I do plan on taking this matter to the financial ombudsman service and also the ICO but have been advised to try and sort this matter first with you. There is a nearly identical case as mine that had been settled by the financial ombudsman service not long ago [case number DRN-3125272] they found that the default should have been reported as soon as the 6th missed payment, and ordered provident to update CRA to reflect this.I kindly ask you to investigate this matter and remove the inaccurate information from my credit file as soon as possible. I would appreciate your prompt attention to this matter and look forward to hearing from you soon.Thank you for your time and consideration.Please send all correspondence via email and not phone, so I have electronic copies.Sincerely*

Their response

Sorry for such a long post, I just wanted to make sure that if anyone had a similar problem, hopefully they will find their way to this post and it helps them.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.9K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards