We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

NS&I to increase the Premium Bond prize rate to 3% – here's all you need to know

Comments

-

Not updated yet - more patience needed apparently!Oasis1 said:

It's a shame they don't say when it was last updated on the webpage, like they do with other articles. I can't tell if it's been updated but the comparisons with savings accounts returns hasn't been updated since 1 Dec apparently.eskbanker said:

They always have when there have been changes before, so no reason to believe they won't again, but they just need to get their pet "post-doctoral cosmology statistician" to crunch the numbers first....Oasis1 said:Will MSE be updating their PB calculator?

https://www.moneysavingexpert.com/savings/premium-bonds/We'll update this guide and our calculator on 3 January 2023 to show how the rate increase affects your likelihood of winning.

[...]

The odds in the calculator are based on the prize distribution for the most recent draw1 -

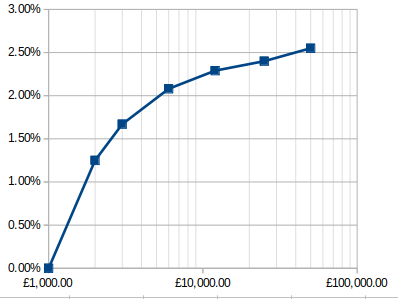

Audaxer said:Is 2.4% only likely if you have the full £50k in PBs?eskbanker said:Not updated yet - more patience needed apparently!To tide us over while we wait for the postdoctoral cosmology statistician, a quick Monte Carlo analysis applied to different holdings (rate is based on the median return, and amounts are £1k, £2k, £3k, £6k, £12k, £25k and £50k):

9

9 -

Good to see our results roughly agree. I got a median 2.55% for a 50k holding over a year with 10% being below 1.75% and 10% being above 3.95% - that's a rather large range of reasonably possible outcomes), although I get slightly higher than you at 2.5% for £25k holding (but that's Monte Carlo for you!), with 80% of outcomes falling in a range from 1.5% to 4.2%.masonic said:Audaxer said:Is 2.4% only likely if you have the full £50k in PBs?eskbanker said:Not updated yet - more patience needed apparently!To tide us over while we wait for the postdoctoral cosmology statistician, a quick Monte Carlo analysis applied to different holdings (rate is based on the median return, and amounts are £1k, £2k, £3k, £6k, £12k, £25k and £50k):

For a BR taxpayer, it appears to be worth holding PBs at the moment - however, what the rates will be after today's BoE announcement is anyone's guess (I note that OakNorth have already pitched in with a 13 basis point increase on their 90 day notice account from 3.07% to 3.2%).

2 -

I had to go through this in the past year after my mum passed. It seems others had differing luck depending on amounts held i.e. some had no issues getting more than £5k without probate. Unfortunately my mum had the full PB holding and some other bonds so we had to get Probate but tbh it wasn't that tough just annoying to have to pay the £270 fee. My dad decided to leave them invested for the additional year.Theatregoer2 said:Everyone considering investing in these should be aware that if you have just £5000 in PBs and you die… even if no inheritance tax is due, you leave everything to your partner and you have no other major assets … NS&I will make your representatives get private - which is both costly and hugely time-consuming. It happened to my elderly mum when my dad died and was a nasty shock.0 -

I have had premium bonds for years and years, and only won £25 prizes, up until this month. I think it makes sense to increase the number of £50 and £100 prizes, if you win, at least you are more likely to win something bigger than £25 or a few of those if you are luckly.

As base rate is now 3.5%, I wonder if rates will increase again after Jan, and if so what the distribution of prizes will be then? Were the odds not worse at 30,0000-to-one before the introduction of £25 prizes.

As base rate increases I assume they will not want to lose big holdings, if holders don't win enough they will sell their bonds, but you could easily find yourself over the £1000 or £500 personal savings allowance for tax with current savings rates.

0 -

Here are the odds of winning an prize in each bracket for a £50,000 holding.All based on perfect average luck. (So expect deviation)

Prize % of fund £1,000,000 0.67% 98721.97 Years to Win £100,000 1.87% 3525.78 Years to Win £50,000 1.87% 1762.89 Years to Win £25,000 1.86% 885.40 Years to Win £10,000 1.87% 353.21 Years to Win £5,000 1.87% 176.60 Years to Win £1,000 4.00% 16.48 Years to Win 500 6.00% 5.49 Years to Win £100 38.75% 5.88 Wins Per Year £50 19.38% 5.88 Wins Per Year £25 21.87% 13.28 Wins Per Year Rounded down to the nearest 2 decimal places.As you can't win a fraction of a prize you have to do some minor rounding to get an average luck figure. Luckily the chances of a lower value win when take as group is almost exactly 25 wins a year.1 Year you'd expect to get £1225, based on 6 £100, 6 £50 and 13 £25 wins. You can see your borrowing that 0.28 chance from the £25 to the £50 & £100 prizes.Realistically 1 of the 100 or 50 prizes could change to any of the other 2 prizes.So a range of £1150 - £1225, but £1225 is the most likely.That's not the end, we can ignore the top tier prizes (£5,000+). If you win your just very lucky.But the mid tier over a 4 year period now start to come into play as you would expect to win 1 of these prizes almost every 4 years when you look at these two prizes combined.With the £500 prize almost 3 times more likely than the £1,000 prize.

1 -

Wins per month? You mean wins per year?Sasahara said:Here are the odds of winning an prize in each bracket for a £50,000 holding.All based on perfect average luck. (So expect deviation)Prize % of fund £1,000,000 0.67% 98721.97 Years to Win £100,000 1.87% 3525.78 Years to Win £50,000 1.87% 1762.89 Years to Win £25,000 1.86% 885.40 Years to Win £10,000 1.87% 353.21 Years to Win £5,000 1.87% 176.60 Years to Win £1,000 4.00% 16.48 Years to Win 500 6.00% 5.49 Years to Win £100 38.75% 5.88 Wins Per Month £50 19.38% 5.88 Wins Per Month £25 21.87% 13.28 Wins Per Month Rounded down to the nearest 2 decimal places.As you can't win a fraction of a prize you have to do some minor rounding to get an average luck figure. Luckily the chances of a lower value win when take as group is almost exactly 25 wins a year.1 Year you'd expect to get £1225, based on 6 £100, 6 £50 and 13 £25 wins. You can see your borrowing that 0.28 chance from the £25 to the £50 & £100 prizes.Realistically 1 of the 100 or 50 prizes could change to any of the other 2 prizes.So a range of £1150 - £1225, but £1225 is the most likely.That's not the end, we can ignore the top tier prizes (£5,000+). If you win your just very lucky.But the mid tier over a 4 year period now start to come into play as you would expect to win 1 of these prizes almost every 4 years when you look at these to prizes combined.With the £500 prize almost 3 times more likely than the £1,000 prize.2 -

I think this is only likely if instant access / notice accounts go up. It seems that while there is some up and down relating to how much they need to take in (not too little as it's part of government funding, not too much as it's competing unfairly with private banks) NS&I mostly seem to be pitching their interest rate on the assumption that PBs are a halfway house between instant access and notice, and (on a small lag) setting the prize fund rate about halfway between the best buys of those two.newfoundglory said:

As base rate is now 3.5%, I wonder if rates will increase again after Jan, and if so what the distribution of prizes will be then? Were the odds not worse at 30,0000-to-one before the introduction of £25 prizes.

As base rate increases I assume they will not want to lose big holdings, if holders don't win enough they will sell their bonds, but you could easily find yourself over the £1000 or £500 personal savings allowance for tax with current savings rates.

0 -

As base rate is now 3.5%, I wonder if rates will increase again after Jan, and if so what the distribution of prizes will be then?

I presume the increase in prize rate to 3% , is the response to a base rate of 3.5 %, which was widely expected. So I would not expect any more increases, unless/until the base rate and other easy access accounts start to increase quite a bit more.

As said in the previous post, PB's have other advantages when competing with other easy access accounts and the large majority of PB savers are reluctant to cash them in, and/or take very little notice of savings rates generally. The posters/switchers on this forum are not typical of the general public.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards