We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Another "hint" from Pensions Minister that State Pension Age eligibility will change

Comments

-

1) NPA to SPA. For actuarial reduction, the NPA prevailing at the time of the contributions is used (since this has changed many times over the years, it is quite involved to actually work this out). However, assuming predictions of future increases in longevity are correct (and they have been revised sharply downwards over the last decade or so), on average, younger members will receive the income for a similar period (little comfort).Universidad said:tooldle said:I'm also in USS. My understanding is 'cuts' are to future benefits and not existing.There are two ways in which the value of already accrued USS benefits has been reduced by cuts, that I am aware of.1) When the scheme switched from its own NPA, to the SPA, with the SPA being higher.Your accrued benefits are not directly cut, but the cut introduced does absolutely devalue them. Because now either you retire earlier than the new SPA, and your benefits after the cut are actuarially reduced, or you retire at SPA (later than the orignal NPA), and your benefits from before the cut are reduced... because they're not uprated by late retirement factors, so you just get less of them than you've paid for.2) When the final salary scheme closed, settling your final salary as the salary at the time of the closure, rather than your final salary with the employer.Again, not a direct cut to the benefit accrued. You could have quit on the spot and it would have made no difference.But let's not be obtuse, the scheme was sold to us as a final salary scheme. This change alone devalued my original package significantly. I got my big promotion the year after the scheme closed.Now you can tell me that sort of unfairness was why Final Salary was not a good way to run a scheme. But what you can't tell me is that the change didn't cost me, based on the career I had, and the benefits I'd already accrued.Notice how both of the above cuts affected younger people more and older people less - a theme in all of these cuts, and where I came in - on the theme of intergenerational equality in pensions.

I completely agree with your general comments, for a new starter or members with little or no service prior to 2011, the DB component of USS is a much, much poorer prospect than it was. For example, modelling the 2.5% cap with historical UK inflation has a significant impact on income throughout retirement.

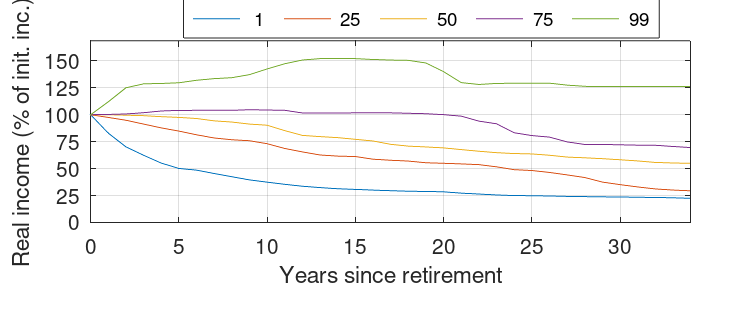

Figure shows real income (i.e. adjusted for inflation) at the 1st (worst), 25th, 50th (median), 75th, and 99th (best) percentiles as a function of time since retirement for a 2.5% inflation cap. Historical UK CPI was used (drawn from the database at https://www.macrohistory.net).*

The median case shows a decrease in real income of nearly 50% after 35 years (i.e. aged 100 assuming a retirement at 65). Even after only a decade, the real income ranges from a dreadful 35% of the initial income at the 1st percentile (the 1970s) to 90% in the median case. Note, the cases showing increases in real income are due to historic periods of deflation (largely confined to before 1930) since USS does have a deflationary floor (i.e., the nominal amount will not be decreased) - my cynical self suspects that the floor will be removed at the first sight of future deflation!

* ps anyone contemplating buying a nominal annuity (even one with an escalation) might do well to look at this graph!

1 -

OldScientist said:

1) NPA to SPA. For actuarial reduction, the NPA prevailing at the time of the contributions is used (since this has changed many times over the years, it is quite involved to actually work this out). However, assuming predictions of future increases in longevity are correct (and they have been revised sharply downwards over the last decade or so), on average, younger members will receive the income for a similar period (little comfort).Universidad said:tooldle said:I'm also in USS. My understanding is 'cuts' are to future benefits and not existing.There are two ways in which the value of already accrued USS benefits has been reduced by cuts, that I am aware of.1) When the scheme switched from its own NPA, to the SPA, with the SPA being higher.Your accrued benefits are not directly cut, but the cut introduced does absolutely devalue them. Because now either you retire earlier than the new SPA, and your benefits after the cut are actuarially reduced, or you retire at SPA (later than the orignal NPA), and your benefits from before the cut are reduced... because they're not uprated by late retirement factors, so you just get less of them than you've paid for.2) When the final salary scheme closed, settling your final salary as the salary at the time of the closure, rather than your final salary with the employer.Again, not a direct cut to the benefit accrued. You could have quit on the spot and it would have made no difference.But let's not be obtuse, the scheme was sold to us as a final salary scheme. This change alone devalued my original package significantly. I got my big promotion the year after the scheme closed.Now you can tell me that sort of unfairness was why Final Salary was not a good way to run a scheme. But what you can't tell me is that the change didn't cost me, based on the career I had, and the benefits I'd already accrued.Notice how both of the above cuts affected younger people more and older people less - a theme in all of these cuts, and where I came in - on the theme of intergenerational equality in pensions.

I completely agree with your general comments, for a new starter or members with little or no service prior to 2011, the DB component of USS is a much, much poorer prospect than it was. For example, modelling the 2.5% cap with historical UK inflation has a significant impact on income throughout retirement.

Figure shows real income (i.e. adjusted for inflation) at the 1st (worst), 25th, 50th (median), 75th, and 99th (best) percentiles as a function of time since retirement for a 2.5% inflation cap. Historical UK CPI was used (drawn from the database at https://www.macrohistory.net).*

The median case shows a decrease in real income of nearly 50% after 35 years (i.e. aged 100 assuming a retirement at 65). Even after only a decade, the real income ranges from a dreadful 35% of the initial income at the 1st percentile (the 1970s) to 90% in the median case. Note, the cases showing increases in real income are due to historic periods of deflation (largely confined to before 1930) since USS does have a deflationary floor (i.e., the nominal amount will not be decreased) - my cynical self suspects that the floor will be removed at the first sight of future deflation!

* ps anyone contemplating buying a nominal annuity (even one with an escalation) might do well to look at this graph!It could be even worse as AIUI the 2.5% inflation cap applies (or rather will apply from 2024) to previous years while still working, so it could be 70 years capped at 2.5% (for say a 25 year old who retires at 65 and lives to 95).The USS looks like an extreme example of a scheme that was incredibly generous, unlimited inflation protection was unusual outside the pubic sector, and is now (in terms of DB schemes anyway) pretty rubbish. They might as well have gone fully DC like most of the private sector have.Maybe the USS is now paying the price for past "abuses" such as the alleged practice of employers offering late career pay rises to boost pensions without the cost to the pension fund being passed onto the employer, as discussed here:A similar thing has happened with other pensions though not as extreme, most private sector schemes capped inflation rises to the stautory 5% cap, at least until it was reduced to 2.5% in 2005 by the last Labour govt in a desperate attempt to stop the demise the remaining DB pension schemes. Having just 8 years earlier imposed extra taxes on them because they were doing so well...

0 -

Interested to see the stats on life expectancy and effects on state pension payments.

Life expectancy can rise but the number of people claiming state pensions remain the same, particularly if they are increasing the age one can claim at.0 -

A bundle of joy on here again today I see, no wonder people feel like pegging out. I'm sat here with a chemo drip in my arm at 60Get a grip and enjoy what you have of your life9

-

Deleted_User said:

I planned for retirement at age 60 but mine has been moved to 67. Honestly, I don't think I'm going to get a pension - I don't believe it will be available when the time comes. I'm now planning for no state pension or healthcare/social care. The numbers just don't add up - it's not affordable.thriftytracey said:The state pension age is currently 66 and two further increases are already set out in legislation, including a gradual rise to 67 for those born on or after April 1960; and a gradual rise to 68 between 2044 and 2046 for those born on or after April 1977.

The briefings to the press suggest that the timescales will be changed in May 2023 when the review is published so that people will have to wait longer for their state pension.

Yet longevity is now falling? Not helped by the state of the NHS. Apparently excess mortality in October was 900 deaths due to ambulance wait times.

My own state pension eligibility falls in February 2026 so I narrowly missed having to wait until age 67. Could this change?

This notion that life expectancy has increased isn't really true. My grandparents all lived to late seventies with two living to 80's. None of their (10 in total) children matched those ages. The oldest lived to 78 and three died before 60. There were no young deaths in my grandparents generation (other than deaths of babies / during childbirth).

In reality, what happened is they dealt with some of the high numbers of early deaths - so pre-5 deaths used to be high and a lot of working class men did jobs that killed them off early. The eliminated those EARLY deaths an that raised average life expectancy. But healthy people aren't living longer - and in pretty much every family I know they're dying younger now.Sorry but this is rubbish, life expectancy has been increasing over the longer term even when you ignore those who died young. A sample of a handful of people in your immediate family doesn't mean the stats are a "slight of hand".Between 2001 and 2019 life expectancy at 65, ie the number of years someone who has already survived till 65 can expect to live, has gone up from 16.1 to 19.1 years for men and 19.2 to 21.5 for women.So about a 19% increase for men and 12% increase for women, over less than a couple of decades.

5 -

Here is the cohort life expectancy for those aged 65 (values from ONS data downloadable from https://www.ons.gov.uk/peoplepopulationandcommunity/birthsdeathsandmarriages/lifeexpectancies/datasets/lifetablesprincipalprojectionunitedkingdom). I've rounded values to the nearest integer year.Deleted_User said:

I planned for retirement at age 60 but mine has been moved to 67. Honestly, I don't think I'm going to get a pension - I don't believe it will be available when the time comes. I'm now planning for no state pension or healthcare/social care. The numbers just don't add up - it's not affordable.thriftytracey said:The state pension age is currently 66 and two further increases are already set out in legislation, including a gradual rise to 67 for those born on or after April 1960; and a gradual rise to 68 between 2044 and 2046 for those born on or after April 1977.

The briefings to the press suggest that the timescales will be changed in May 2023 when the review is published so that people will have to wait longer for their state pension.

Yet longevity is now falling? Not helped by the state of the NHS. Apparently excess mortality in October was 900 deaths due to ambulance wait times.

My own state pension eligibility falls in February 2026 so I narrowly missed having to wait until age 67. Could this change?

This notion that life expectancy has increased isn't really true. My grandparents all lived to late seventies with two living to 80's. None of their (10 in total) children matched those ages. The oldest lived to 78 and three died before 60. There were no young deaths in my grandparents generation (other than deaths of babies / during childbirth).

In reality, what happened is they dealt with some of the high numbers of early deaths - so pre-5 deaths used to be high and a lot of working class men did jobs that killed them off early. The eliminated those EARLY deaths an that raised average life expectancy. But healthy people aren't living longer - and in pretty much every family I know they're dying younger now.

Males Females

1980 (birth year 1915) 13 years 18 years

1990 (birth year 1925) 15 years 20 years

2000 (birth year 1935) 18 years 22 years

2010 (birth year 1945) 20 years 22 years

2020 (birth year 1955) 20 years 23 years

Of course, the later values rely on projections more than the earlier ones. But for the whole UK population, the life expectancy at 65 has increased over the last 40 years or so. I have no idea whether it will continue to do so, since the last decade has seen a slowing down in the increase. Also interesting to note that the gap in life expectancy between males and females has closed from 5 to 3 years over that 40 year period.

2 -

Do they publish stats like this based on the age the person retired - someone once claimed to me that people who retire at 65 tend to die much younger than people who retire at 60 or 55 - I am not sure where he got this info from or even whether there is any truth in it.OldScientist said:

Here is the cohort life expectancy for those aged 65 (values from ONS data downloadable from https://www.ons.gov.uk/peoplepopulationandcommunity/birthsdeathsandmarriages/lifeexpectancies/datasets/lifetablesprincipalprojectionunitedkingdom). I've rounded values to the nearest integer year.Deleted_User said:

I planned for retirement at age 60 but mine has been moved to 67. Honestly, I don't think I'm going to get a pension - I don't believe it will be available when the time comes. I'm now planning for no state pension or healthcare/social care. The numbers just don't add up - it's not affordable.thriftytracey said:The state pension age is currently 66 and two further increases are already set out in legislation, including a gradual rise to 67 for those born on or after April 1960; and a gradual rise to 68 between 2044 and 2046 for those born on or after April 1977.

The briefings to the press suggest that the timescales will be changed in May 2023 when the review is published so that people will have to wait longer for their state pension.

Yet longevity is now falling? Not helped by the state of the NHS. Apparently excess mortality in October was 900 deaths due to ambulance wait times.

My own state pension eligibility falls in February 2026 so I narrowly missed having to wait until age 67. Could this change?

This notion that life expectancy has increased isn't really true. My grandparents all lived to late seventies with two living to 80's. None of their (10 in total) children matched those ages. The oldest lived to 78 and three died before 60. There were no young deaths in my grandparents generation (other than deaths of babies / during childbirth).

In reality, what happened is they dealt with some of the high numbers of early deaths - so pre-5 deaths used to be high and a lot of working class men did jobs that killed them off early. The eliminated those EARLY deaths an that raised average life expectancy. But healthy people aren't living longer - and in pretty much every family I know they're dying younger now.

Males Females

1980 (birth year 1915) 13 years 18 years

1990 (birth year 1925) 15 years 20 years

2000 (birth year 1935) 18 years 22 years

2010 (birth year 1945) 20 years 22 years

2020 (birth year 1955) 20 years 23 years

Of course, the later values rely on projections more than the earlier ones. But for the whole UK population, the life expectancy at 65 has increased over the last 40 years or so. I have no idea whether it will continue to do so, since the last decade has seen a slowing down in the increase. Also interesting to note that the gap in life expectancy between males and females has closed from 5 to 3 years over that 40 year period.0 -

Interesting question - there's a 10 year old BBC article (https://www.bbc.co.uk/news/magazine-18952037) that suggests the news is mixed and some more recent US research summarised at https://hbr.org/2016/10/youre-likely-to-live-longer-if-you-retire-after-65 with a quote "The literature on the relationship between retirement age and longevity is still developing. The findings are mixed." from the latter source.Pat38493 said:

Do they publish stats like this based on the age the person retired - someone once claimed to me that people who retire at 65 tend to die much younger than people who retire at 60 or 55 - I am not sure where he got this info from or even whether there is any truth in it.OldScientist said:

Here is the cohort life expectancy for those aged 65 (values from ONS data downloadable from https://www.ons.gov.uk/peoplepopulationandcommunity/birthsdeathsandmarriages/lifeexpectancies/datasets/lifetablesprincipalprojectionunitedkingdom). I've rounded values to the nearest integer year.Deleted_User said:

I planned for retirement at age 60 but mine has been moved to 67. Honestly, I don't think I'm going to get a pension - I don't believe it will be available when the time comes. I'm now planning for no state pension or healthcare/social care. The numbers just don't add up - it's not affordable.thriftytracey said:The state pension age is currently 66 and two further increases are already set out in legislation, including a gradual rise to 67 for those born on or after April 1960; and a gradual rise to 68 between 2044 and 2046 for those born on or after April 1977.

The briefings to the press suggest that the timescales will be changed in May 2023 when the review is published so that people will have to wait longer for their state pension.

Yet longevity is now falling? Not helped by the state of the NHS. Apparently excess mortality in October was 900 deaths due to ambulance wait times.

My own state pension eligibility falls in February 2026 so I narrowly missed having to wait until age 67. Could this change?

This notion that life expectancy has increased isn't really true. My grandparents all lived to late seventies with two living to 80's. None of their (10 in total) children matched those ages. The oldest lived to 78 and three died before 60. There were no young deaths in my grandparents generation (other than deaths of babies / during childbirth).

In reality, what happened is they dealt with some of the high numbers of early deaths - so pre-5 deaths used to be high and a lot of working class men did jobs that killed them off early. The eliminated those EARLY deaths an that raised average life expectancy. But healthy people aren't living longer - and in pretty much every family I know they're dying younger now.

Males Females

1980 (birth year 1915) 13 years 18 years

1990 (birth year 1925) 15 years 20 years

2000 (birth year 1935) 18 years 22 years

2010 (birth year 1945) 20 years 22 years

2020 (birth year 1955) 20 years 23 years

Of course, the later values rely on projections more than the earlier ones. But for the whole UK population, the life expectancy at 65 has increased over the last 40 years or so. I have no idea whether it will continue to do so, since the last decade has seen a slowing down in the increase. Also interesting to note that the gap in life expectancy between males and females has closed from 5 to 3 years over that 40 year period.

1 -

I've no idea whether there are stats on this, but I would have thought that generally the younger a person was able to retire, the higher their salary and economic situation (which will generally have been throughout their life) which is going to have a big impact on average length of life - obviously there will be people that buck this trend, but it seems a valid hypothesis (though of course a lot of other seemingly valid hypotheses have been proved to be false after actual research).Pat38493 said:

Do they publish stats like this based on the age the person retired - someone once claimed to me that people who retire at 65 tend to die much younger than people who retire at 60 or 55 - I am not sure where he got this info from or even whether there is any truth in it.OldScientist said:

Here is the cohort life expectancy for those aged 65 (values from ONS data downloadable from https://www.ons.gov.uk/peoplepopulationandcommunity/birthsdeathsandmarriages/lifeexpectancies/datasets/lifetablesprincipalprojectionunitedkingdom). I've rounded values to the nearest integer year.Deleted_User said:

I planned for retirement at age 60 but mine has been moved to 67. Honestly, I don't think I'm going to get a pension - I don't believe it will be available when the time comes. I'm now planning for no state pension or healthcare/social care. The numbers just don't add up - it's not affordable.thriftytracey said:The state pension age is currently 66 and two further increases are already set out in legislation, including a gradual rise to 67 for those born on or after April 1960; and a gradual rise to 68 between 2044 and 2046 for those born on or after April 1977.

The briefings to the press suggest that the timescales will be changed in May 2023 when the review is published so that people will have to wait longer for their state pension.

Yet longevity is now falling? Not helped by the state of the NHS. Apparently excess mortality in October was 900 deaths due to ambulance wait times.

My own state pension eligibility falls in February 2026 so I narrowly missed having to wait until age 67. Could this change?

This notion that life expectancy has increased isn't really true. My grandparents all lived to late seventies with two living to 80's. None of their (10 in total) children matched those ages. The oldest lived to 78 and three died before 60. There were no young deaths in my grandparents generation (other than deaths of babies / during childbirth).

In reality, what happened is they dealt with some of the high numbers of early deaths - so pre-5 deaths used to be high and a lot of working class men did jobs that killed them off early. The eliminated those EARLY deaths an that raised average life expectancy. But healthy people aren't living longer - and in pretty much every family I know they're dying younger now.

Males Females

1980 (birth year 1915) 13 years 18 years

1990 (birth year 1925) 15 years 20 years

2000 (birth year 1935) 18 years 22 years

2010 (birth year 1945) 20 years 22 years

2020 (birth year 1955) 20 years 23 years

Of course, the later values rely on projections more than the earlier ones. But for the whole UK population, the life expectancy at 65 has increased over the last 40 years or so. I have no idea whether it will continue to do so, since the last decade has seen a slowing down in the increase. Also interesting to note that the gap in life expectancy between males and females has closed from 5 to 3 years over that 40 year period.3 -

Others have commented on your suggestion that your own personal experience overrides all the analysis that has been done by statistical experts and I am afraid to say that I agree with them. But this particular statement is in my opinion absolutely spot on. We are in the position that both my mum and my father in law have no quality of life and no dignity and neither would wish to be "living" like they are. Not a phrase that I particularly care for but "you wouldn't treat a dog like that".Deleted_User said:There's a difference between living and being 'kept alive'.

To be honest though I have no idea what the solution is.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.3K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 248K Work, Benefits & Business

- 605.2K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards