We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

High dividend yield income funds vs capital accumulation funds in retirement drawdown?

Comments

-

but avoids continual decisions on what, when and how much to sell or whether to change your expenditure.Whether to change your expenditure. That either means you know you have more than you’ll need during your lifetime, a nice situation many who discuss this matter don’t enjoy - hence their agonising over the best/better strategy; or you have your head in the sand with respect to running out of money. Using a ‘rational approach’ with ‘this’ for income and ‘that’ for growth doesn’t solve ‘not enough money’, unless I’ve missed something.

By automatically paying dividend and interest income into your current account you can avoid any effort whatsoever beyond an annual review.0 -

Unexpectedly not having enough money after retirement could arise from two possibilities…JohnWinder said:but avoids continual decisions on what, when and how much to sell or whether to change your expenditure.Whether to change your expenditure. That either means you know you have more than you’ll need during your lifetime, a nice situation many who discuss this matter don’t enjoy - hence their agonising over the best/better strategy; or you have your head in the sand with respect to running out of money. Using a ‘rational approach’ with ‘this’ for income and ‘that’ for growth doesn’t solve ‘not enough money’, unless I’ve missed something.

By automatically paying dividend and interest income into your current account you can avoid any effort whatsoever beyond an annual review.

- your planning was poor

- you were unlucky as assumptions you reasonably made based on history proved to be catastrophically wrong.

In both cases I see no solution other than a replan on new assumptions including opting for lower expenditure. Going for greater growth may improve the situation but it increases the risk that it doesn’t.

Fortunately I believe most people most of the time won’t be in that position as they will have planned on historically very pessimistic assumptions and after a few years of “normal” economic events they could have more money in their pot than when they started.

So that leaves us with the problem of coping with expected and planned for events. You can take a high growth approach and modify your spending up and down or only aim for sufficient growth to keep expenditure as planned in the long term.

High growth may make sense if enriching your beneficiaries is an important factor. Otherwise you may be happier focussing on a future with minimum financial worries. In those circumstances a large amount of cash or cautious investments are a valuable tool as they give you the option of waiting for the market to recover or to allow minor changes in your lifestyle to produce significant effects.0 -

‘Some level of growth is essential to keep up with long term inflation. Beyond that level your wealth could more usefully be spent in providing a steady income. ’

No doubt, dividends steadily or lumpily trickling or pouring in to a cash account that pays the bills is a convenience not to be understated for some people. And taxation might prioritise dividends to growth for some investors. Create your own list here.

But there’s an element of mental accounting by some people, dividends and growth viewed as less linked to each other and to some extent separate sources of income, whereas they are both part of the overall returns of the investment. We see this ‘accounting’ in notions like: ‘I’m happy the dividends held up through covid, although the value fell’; ‘CTY has never failed to raise its dividend’ (correct me if the trust is not CTY), the implication being it’s a good investment. This pushes investors in the direction of higher yielding stocks/funds, something examined in this paper: The Dividend Disconnect. Samuel M. Hartzmark University of Chicago Booth School of Business. David H. Solomon Boston College Carroll School of Management. July 30, 2018. From which:

When interest rates and bond yields are low, giving poor ‘income’, investors who like the idea of ‘automatic income’ rather than selling stocks move more into higher dividend paying stocks thus pushing their price up and returns down. ‘We estimate that investors buying dividend-paying stocks during times of high demand earn roughly 2-4% less per year in expectation. Thus, an investor whose preferences for dividends cause him to shift into and out of dividend-paying stocks at the same time as other investors would lose a significant portion of the equity premium by doing so.’

German research finds that personal spending is related temporally to when dividends are received. That might partly be because some people are dependent on the latest dividend to pay their bills, but even so there may be a cost in returns to them. Consuming Dividends. SAFE Working Paper No. 280. 6 Nov 2021. Konstantin Bräuer, Andreas Hackethal, Tobin Hanspal

And The Journal of Finance article at https://onlinelibrary.wiley.com/doi/abs/10.1111/jofi.12968, reports the same timing in spending regardless of wealth. Beware the effects of the ‘dividend fallacy’.

0 -

‘High growth may make sense if enriching your beneficiaries is an important factor. Otherwise you may be happier focussing on a future with minimum financial worries. In those circumstances a large amount of cash or cautious investments are a valuable tool ’

Of course I don’t know what ‘high growth’ means, but we’ve been talking about taking dividends or capital growth in this thread, so I’ll guess it means stocks which are not deliberately chosen as dividend paying stocks which we contrast with high dividend paying stocks which might not be meant for our heirs. This chart shows both beasts are nearly identical. On the other hand, if ‘ cautious investments’ and cash means government bonds and cash, then we’ve moved ‘off-thread’.

0

0 -

There's lots of ways to solve this problem. My approach would to use an annuity for income and index funds for some growth and some dividends. I find this trivial to manage because I basically don't do anything. In the US the dividend situation is a bit simpler than in the UK as we don't have INC or ACC versions of the same fund - whether dividends are reinvested or paid out as cash is decided just by telling the platform whether or not to reinvest dividends. The downside is that in the US dividends and capital gains are taxed annually whatever you do.Linton said:

The extent to which you need growth or income depends on your circumstances. Some level of growth is essential to keep up with long term inflation. Beyond that level your wealth could more usefully be spent in providing a steady income.bostonerimus said:Moderation in all things! So I like broad, cap. weighted index funds because you'll get a couple of percent in dividends and, hopefully, long term growth. I would not emphasize either growth or income/dividends.

The chances of your needs being optimally satisfied by the average allocations of every other investor in the world seem pretty low.

Basing your allocations on your objectives seems a more rational approach. It requires more effort in designing and maintaining your portfolio but avoids continual decisions on what, when and how much to sell or whether to change your expenditure.

By automatically paying dividend and interest income into your current account you can avoid any effort whatsoever beyond an annual review.“So we beat on, boats against the current, borne back ceaselessly into the past.”0 -

An annuity may be useful for some people but its inflexibility and cost, despite recent improvements, are downsides.bostonerimus said:

There's lots of ways to solve this problem. My approach would to use an annuity for income and index funds for some growth and some dividends. I find this trivial to manage because I basically don't do anything. In the US the dividend situation is a bit simpler than in the UK as we don't have INC or ACC versions of the same fund - whether dividends are reinvested or paid out as cash is decided just by telling the platform whether or not to reinvest dividends. The downside is that in the US dividends and capital gains are taxed annually whatever you do.Linton said:

The extent to which you need growth or income depends on your circumstances. Some level of growth is essential to keep up with long term inflation. Beyond that level your wealth could more usefully be spent in providing a steady income.bostonerimus said:Moderation in all things! So I like broad, cap. weighted index funds because you'll get a couple of percent in dividends and, hopefully, long term growth. I would not emphasize either growth or income/dividends.

The chances of your needs being optimally satisfied by the average allocations of every other investor in the world seem pretty low.

Basing your allocations on your objectives seems a more rational approach. It requires more effort in designing and maintaining your portfolio but avoids continual decisions on what, when and how much to sell or whether to change your expenditure.

By automatically paying dividend and interest income into your current account you can avoid any effort whatsoever beyond an annual review.0 -

I agree that over the long term of, in this example, 35 years growth and value (generally associated with high dividend stocks) will perform the same. I have said elsewhere that I believe any sufficiently broadly based portfolio will perform the same given sufficient time.JohnWinder said:‘High growth may make sense if enriching your beneficiaries is an important factor. Otherwise you may be happier focussing on a future with minimum financial worries. In those circumstances a large amount of cash or cautious investments are a valuable tool ’Of course I don’t know what ‘high growth’ means, but we’ve been talking about taking dividends or capital growth in this thread, so I’ll guess it means stocks which are not deliberately chosen as dividend paying stocks which we contrast with high dividend paying stocks which might not be meant for our heirs. This chart shows both beasts are nearly identical. On the other hand, if ‘ cautious investments’ and cash means government bonds and cash, then we’ve moved ‘off-thread’.

However us retirees don’t have the luxury of 35 years for things to even out. We need a strategy that works in the medium term when different allocations can behave in very different ways.

As to bonds or other approaches retirement investing being off-topic, I cannot see how you can sensibly discuss individual questions such as dividends or growth in isolation. They must be seen in the context of an overall strategy.

0 -

Yes but I believe you would have to wait until your mid/late 70s before a joint life inflation linked annuity reaches 5%-6%and that only gives 50% to the survivor.Deleted_User said:I do think annuities are underappreciated. They are in many ways the perfect product for somebody whose main aim for a lump of capital is to use it to give them a good standard of living while they're alive, with how much is left over being a secondary concern.They are not so useful for people who have so much capital that there is bound to be lots left over. If you can invest without straining for a high income, perhaps getting 2-3% income on your capital, and that is plenty for you when combined with any guaranteed pensions in payment you may also have, then you don't really need annuities.But if you want more like 5-6% income on your capital, and are old enough that an annuity can give you that, then an annuity will reliably pay you what it's supposed to, unlike investing targetting 5-6% income. Not only is all investing uncertain, but pushing for such a high income can increase the risks by reducing your portfolio's diversification.Partial annuitization, to give you a secure base income, and then investing the remaining capital aiming for a modest (2-3%) income, is another option.1 -

I did the "partial annuitization" thing to give me a guaranteed base income. Of course an annuity isn't an investment it's an insurance product and I feel that it diversifies your retirement income generation. So you get income from an annuity, dividends, capital gains and state pension. If you have a long term plan you might also add rental income, so you are not limited to funds with high dividends or capital growth when looking for income.Deleted_User said:I do think annuities are underappreciated. They are in many ways the perfect product for somebody whose main aim for a lump of capital is to use it to give them a good standard of living while they're alive, with how much is left over being a secondary concern.They are not so useful for people who have so much capital that there is bound to be lots left over. If you can invest without straining for a high income, perhaps getting 2-3% income on your capital, and that is plenty for you when combined with any guaranteed pensions in payment you may also have, then you don't really need annuities.But if you want more like 5-6% income on your capital, and are old enough that an annuity can give you that, then an annuity will reliably pay you what it's supposed to, unlike investing targetting 5-6% income. Not only is all investing uncertain, but pushing for such a high income can increase the risks by reducing your portfolio's diversification.Partial annuitization, to give you a secure base income, and then investing the remaining capital aiming for a modest (2-3%) income, is another option.“So we beat on, boats against the current, borne back ceaselessly into the past.”0 -

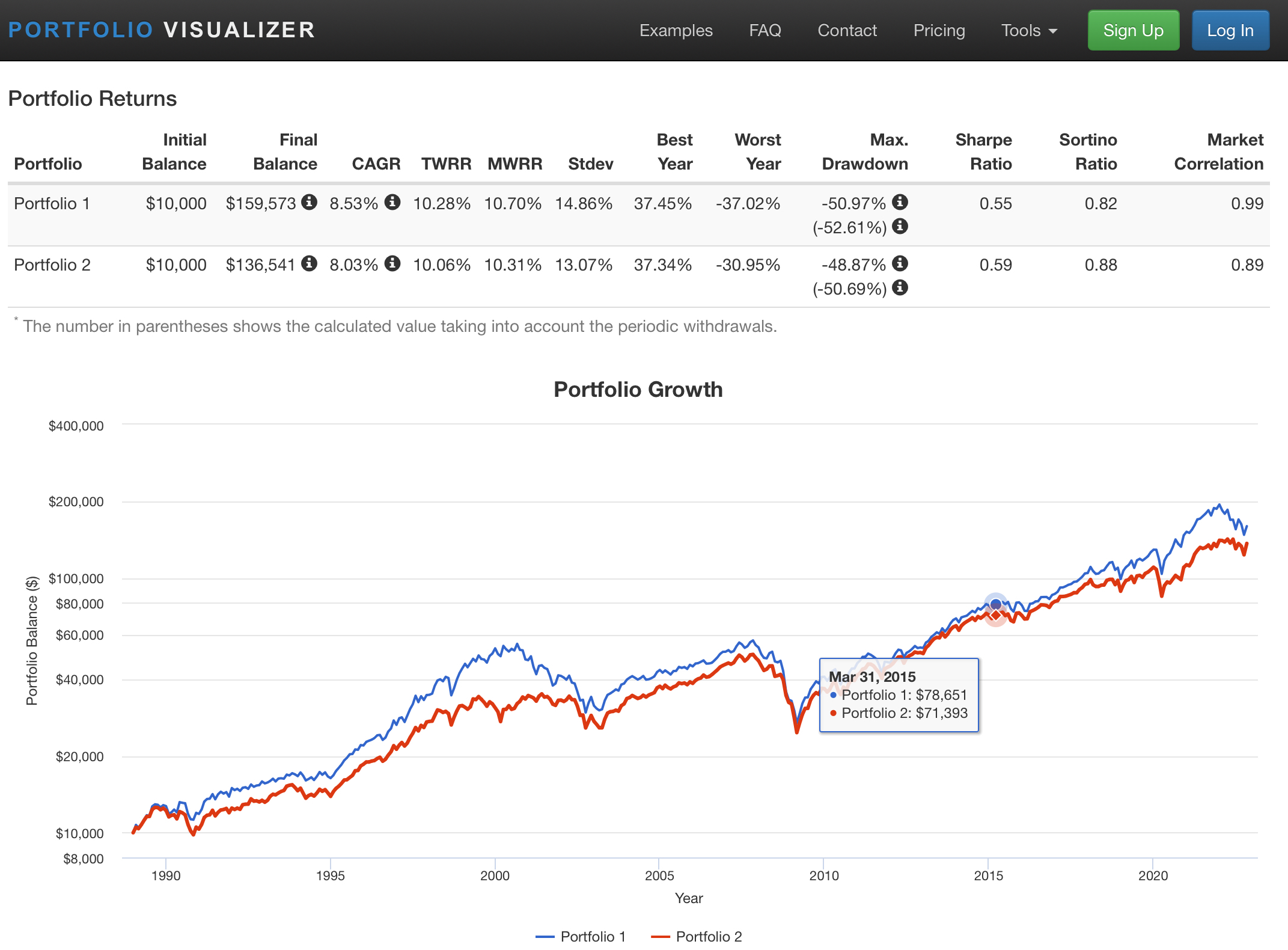

However us retirees don’t have the luxury of 35 years for things to even out. We need a strategy that works in the medium term when different allocations can behave in very different ways.Looking at that chart with such similar performances for an all-stock fund vs a dividend focused stock fund, I don’t see why they wouldn’t serve one equally well if it was one’s intention to take the same amount out each year as either dividends, capital gains or a bit of both. But we can test that, and here’s one example of the same funds from which is taken $400 (4% at start) each year. The red one is the ‘dividend’ fund, the blue the broader fund. Of course, this ignores the work required to take capital gains, compared with ‘no effort’ dividend receiving.

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards