We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

BOE & Pensions Collapse?

Jaguar_Skills

Posts: 557 Forumite

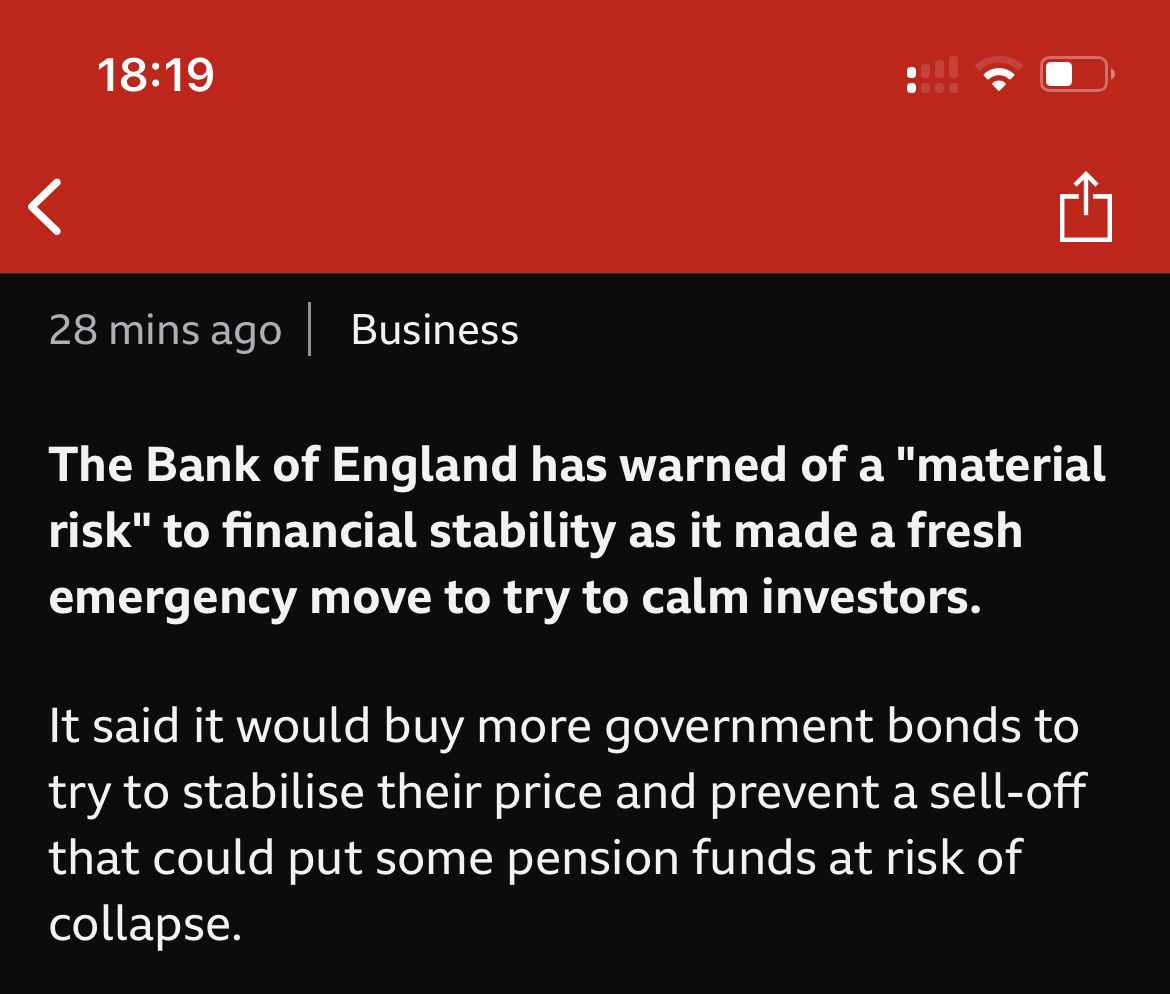

So normally I’m not one for the news scaremongering tactics but reading something on bbc news this evening caught my eye.

What would a collapse look like?

I’ve worked hard as a HRT payer to try and save as much as I can into my pension (36 and currently have a pot of circa £300k).

Obviously it would be devastating if that were all to disappear so I’m curious as to what this might look like or whether it’s just the news outlets creating headlines for clicks.

0

Comments

-

Jaguar_Skills said:Obviously it would be devastating if that were all to disappear so I’m curious as to what this might look like or whether it’s just the news outlets creating headlines for clicks.

If you can catch a recording of this evening's BBC six o'clock news and the piece at 6.06pm should hopefully reassure you. If there isn't a recording I'm sure it will be covered again at 10 o'clock.

To summarise they said, 'this only affects a very small proportion of pension funds and the Bank of England's intervention is to provide them with the breathing space they need to get their [that small proportion of pension funds] finances in order'.

Of course, always good to keep an eye on stories like this and to get your news from various different sources too.1 -

Assuming your pot is a standard DC pension, it is affected by share and bond movements, but no possibility it will suddenly collapse to nothing.Jaguar_Skills said:So normally I’m not one for the news scaremongering tactics but reading something on bbc news this evening caught my eye.What would a collapse look like?I’ve worked hard as a HRT payer to try and save as much as I can into my pension (36 and currently have a pot of circa £300k).Obviously it would be devastating if that were all to disappear so I’m curious as to what this might look like or whether it’s just the news outlets creating headlines for clicks.

It is a complicated technical issue relating only to some private sector DB( final salary ) schemes.5 -

I’ve worked hard as a HRT payer to try and save as much as I can into my pension (36 and currently have a pot of circa £300k).If you have a pot then you can ignore the BBC article as it is not referring to your type of pension.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.2 -

No idea about specifics but UK bond prices collapsed which is hurting DB pension schemes and puts their solvency into question. I would expect this to force companies with such schemes to be forced to provide additional funds to assure solvency.Don’t know why BoE feels it needs to help bond holders. When it buys bonds, it throws more cash on the economy and fuels inflation. Which hurts bonds. A vicious circle.2

-

It’s just a fidelity private pension with £240k in and my work Royal London with £60k indunstonh said:I’ve worked hard as a HRT payer to try and save as much as I can into my pension (36 and currently have a pot of circa £300k).If you have a pot then you can ignore the BBC article as it is not referring to your type of pension.0 -

The pension funds were not just holding bonds. They were holding derivatives to protect against large movements in the price of bonds. They guessed wrong, bond prices moved rapidly the wrong way, and these derivatives were left massively underwater. The holders of the derivatives demanded a payment of cash as collateral to guarantee they would get paid (a Margin Call). The pension funds were not holding sufficient cash or liquid assets. They were faced with having to sell long-term holdings at giveaway prices to realise the necessary funding. The losses would have made them potentially unable to cover their liabilities. So the BofE stepped in to manipulate bond prices to make the margin call go away.Deleted_User said:No idea about specifics but UK bond prices collapsed which is hurting DB pension schemes and puts their solvency into question. I would expect this to force companies with such schemes to be forced to provide additional funds to assure solvency.Don’t know why BoE feels it needs to help bond holders. When it buys bonds, it throws more cash on the economy and fuels inflation. Which hurts bonds. A vicious circle.

The BofE has a mandate to maintain the stability of financial markets, which is why they acted. The US Fed does not have such a mandate.6 -

Looking at the replies, it's just more ridiculous scaremongering then. But the majority of people viewing the BBC website will take this as gospel with a headline that says " BOE in emergency move to calm markets". The media in this country are an increasing, irresponsible disgrace.2

-

As an aside, I would suggest you have a very healthy pot for your age…check google for thoughts.

One suggests:

”At age 35 you should have roughly 10% of the final pension amount you plan to take at age 65. If you're aiming for a pension pot of £500,000 then £50,000 is a great aim.”

Maybe you are consciously aiming for £3M…or perhaps retiring early?

If the latter, I’d suggest ensuring your ISA allowances are also filled up - they can easily give you money you can get well before retirement age.You could even use a LISA specifically to aim for money to take from 60….25% free top up from the government 🤷♂️

If this is all obvious to you already, my apologies!Plan for tomorrow, enjoy today!2 -

Thanks for this. A really good post.cfw1994 said:As an aside, I would suggest you have a very healthy pot for your age…check google for thoughts.

One suggests:

”At age 35 you should have roughly 10% of the final pension amount you plan to take at age 65. If you're aiming for a pension pot of £500,000 then £50,000 is a great aim.”

Maybe you are consciously aiming for £3M…or perhaps retiring early?

If the latter, I’d suggest ensuring your ISA allowances are also filled up - they can easily give you money you can get well before retirement age.You could even use a LISA specifically to aim for money to take from 60….25% free top up from the government 🤷♂️

If this is all obvious to you already, my apologies!

I always deliberate over what I should do. Basically I put £750 a month into a Vanguard ISA - I appreciate that’s not a huge amount and nowhere near max it’s just by putting in my max allowance into pension it does help to reduce my tax liability.

Re the pension, I don’t know what really happens once I go over the £1.043m?

I’ve also focused on paying off my mortgage which I have now more or less done but the next house purchase will probably require a massive mortgage - circa another £600k so there will be less going in pension contributions etc.

we also have a bit of a dilemma that my OH doesn’t work and therefore all the pension is mine really.

I think I’ll add this to another post in the next few days and get some thoughts from the forum. We’ve just brought our second child home from the hospital so all a bit chaotic here.0 -

This report accurately reflects a statement released by the Bank of England announcing what action it is taking.jim8888 said:Looking at the replies, it's just more ridiculous scaremongering then. But the majority of people viewing the BBC website will take this as gospel with a headline that says " BOE in emergency move to calm markets". The media in this country are an increasing, irresponsible disgrace.

What would you prefer? That the media suppresses the truth? That is not a society that I want to live in.2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.8K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards