We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

fixed rate bonds VS stocks?

Comments

-

Why S&P500? What's wrong with the rest of the world? I think the average 10 year returns for equities was probably based on an acquisition price quite a bit higher than today, so its likely to be somewhat better based on current valuations. Savings rates undoubtedly have a bit further to rise, but I'd be surprised if we see 6% - where would that leave mortgage rates!The problem with fixing now for 2 years, then investing the proceeds, is that you run the risk of missing out on this period of cheaper stock prices. It would be a shame if markets had already recovered by the time your fix matured. Making regular monthly contributions into the market is worth considering as an alternative.2

-

I don’t know about stocks and shares.

But a fixed rate bond now that’s easy.

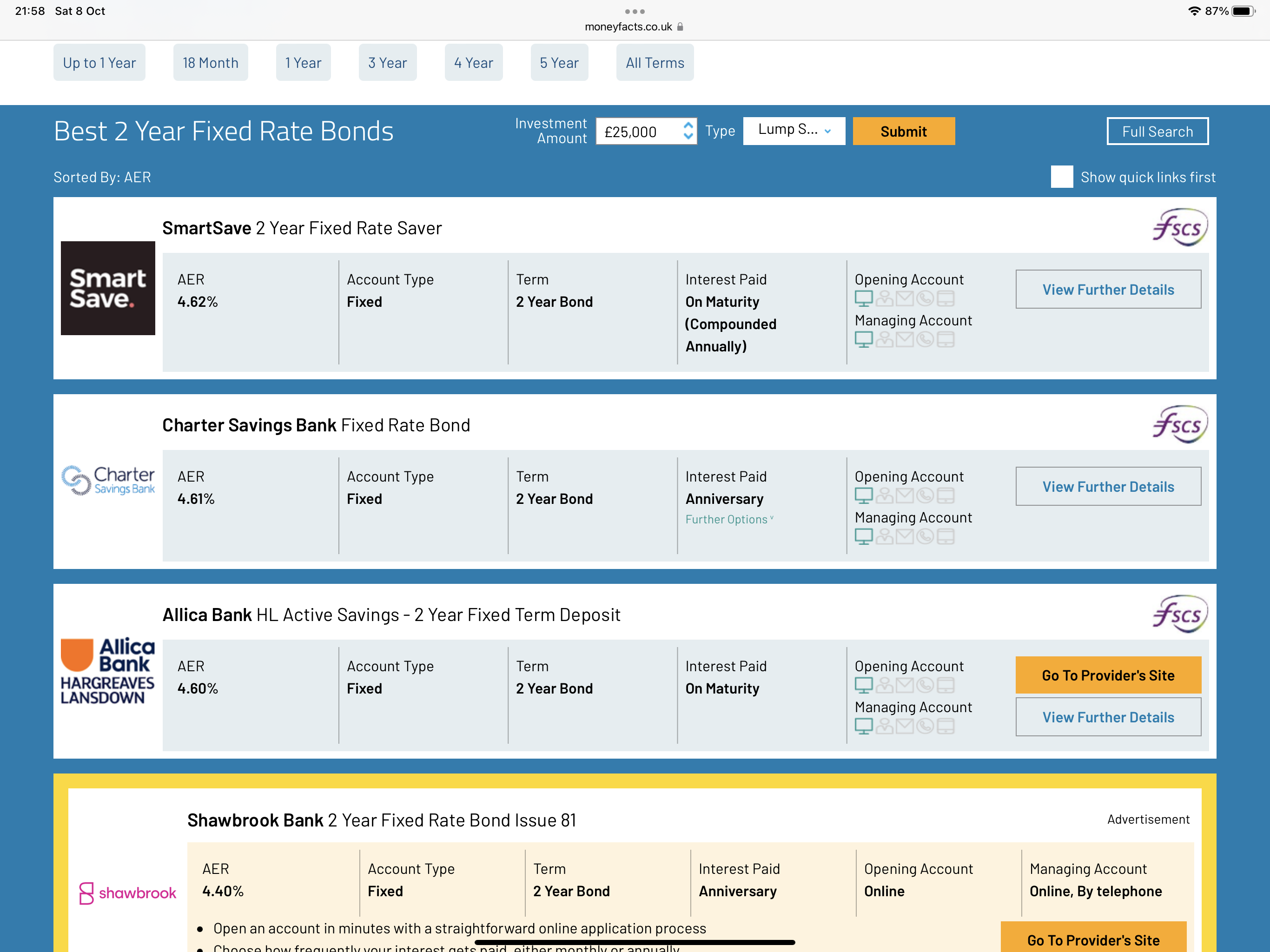

Smart save have 4.62% for 2 years.

But I would wait until November if not late December after the next 2 boe base rate rises.

Stick the cash in Al Ryan easy access at 2.35%, withdrawals limited to 20k a day.

1 -

I was thinking of locking my money away right now in a 2 year fixed rate bond at 4.2% interest and then investing in the stock market with a vanguard S&P 500 fund for the next 8-10 years. What do you think?You have chosen your US equity allocation but what about all the other regions/countries of the world?

With the dollar riding high and Sterling low, you could find that you miss out on the recovery in US markets due to currency fluctuations. So, hedged versions of the fund should be considered for some of the US allocation.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

It's plausible the US market will make gains while the dollar weakens. I'm interested to know whether you are making hedging adjustments to your clients' portfolios?dunstonh said:I was thinking of locking my money away right now in a 2 year fixed rate bond at 4.2% interest and then investing in the stock market with a vanguard S&P 500 fund for the next 8-10 years. What do you think?You have chosen your US equity allocation but what about all the other regions/countries of the world?

With the dollar riding high and Sterling low, you could find that you miss out on the recovery in US markets due to currency fluctuations. So, hedged versions of the fund should be considered for some of the US allocation.1 -

I was thinking of locking my money away right now in a 2 year fixed rate bond at 4.2% interest and then investing in the stock market with a vanguard S&P 500 fund for the next 8-10 years. What do you think?

There are other possible choices, such as paying a lump sum into a pension, or overpaying a mortgage as two examples.

However if we just look at the two choices you have mentioned, it would probably be more sensible to maybe invest some now, and put the rest in a fixed rate savings account. Rather than save it all for two years and then invest it all.

1 -

masonic said:Why S&P500? What's wrong with the rest of the world? I think the average 10 year returns for equities was probably based on an acquisition price quite a bit higher than today, so its likely to be somewhat better based on current valuations. Savings rates undoubtedly have a bit further to rise, but I'd be surprised if we see 6% - where would that leave mortgage rates!The problem with fixing now for 2 years, then investing the proceeds, is that you run the risk of missing out on this period of cheaper stock prices. It would be a shame if markets had already recovered by the time your fix matured. Making regular monthly contributions into the market is worth considering as an alternative.You're absolutly right. I think the VUSA from Vanguard came to mind as I would put at least 50% of my savings in the S&P index tracker and the rest in a world fund, im still looking for one which looks promising. Difficult as they all seem to be going down at the moment!

Thanks, I have put my rainy day fund in an easy access saver but its a bit lower than the Al Ryan 2.35%. Ive been so preoccupied with fixed rate bonds I havent really looked to see if I can get better easy access rates.Bigwheels1111 said:I don’t know about stocks and shares.

But a fixed rate bond now that’s easy.

Smart save have 4.62% for 2 years.

But I would wait until November if not late December after the next 2 boe base rate rises.

Stick the cash in Al Ryan easy access at 2.35%, withdrawals limited to 20k a day.dunstonh said:I was thinking of locking my money away right now in a 2 year fixed rate bond at 4.2% interest and then investing in the stock market with a vanguard S&P 500 fund for the next 8-10 years. What do you think?You have chosen your US equity allocation but what about all the other regions/countries of the world?

With the dollar riding high and Sterling low, you could find that you miss out on the recovery in US markets due to currency fluctuations. So, hedged versions of the fund should be considered for some of the US allocation.

Im sorry, i dont know what you mean/how to hedge a version of the fund?Albermarle said:I was thinking of locking my money away right now in a 2 year fixed rate bond at 4.2% interest and then investing in the stock market with a vanguard S&P 500 fund for the next 8-10 years. What do you think?There are other possible choices, such as paying a lump sum into a pension, or overpaying a mortgage as two examples.

However if we just look at the two choices you have mentioned, it would probably be more sensible to maybe invest some now, and put the rest in a fixed rate savings account. Rather than save it all for two years and then invest it all.

The stocks i would pay into would be first to max out my ISA allowance and then into a SIPP. I dont have a mortgage as I dont own a home and am unlikely to do so in the future, which is why im really only left with investing into stocks and banks savings accounts.If I were to do both bonds and stocks, in your opinion, what would be a sensible ratio of savings invested into bonds Vs stocks? especially as i would be drip feeding into stocks from a reserved pot. Perhaps 60% lump sum in a 1-2 year bond and 40% drip feed into stocks over a year?

0 -

For me, the "crossover" point, when I will prioritize fixed savers / bonds over the stockmarket, comes in the 5-7% range. (Assuming inflation doesn't hit 20%).

At 5%, I may push small cash into fixed bonds. At 6%, I'll consider medium sums. At 7% or more, I'm piling in.1 -

Millyonare said:For me, the "crossover" point, when I will prioritize fixed savers / bonds over the stockmarket, comes in the 5-7% range. (Assuming inflation doesn't hit 20%).

At 5%, I may push small cash into fixed bonds. At 6%, I'll consider medium sums. At 7% or more, I'm piling in.

Thanks! could you give me an idea of how much you would consider to be a small/medium amount? i'm a bit intimidated by your nametag 0

0 -

If your savings are in an account paying 0.25% I'd get that sorted asap and then decide your longer term plan. There's no point rushing into buying share based funds without doing some proper thinking about what you want and your risk profile so you might as well get the savings working while you do that.Remember the saying: if it looks too good to be true it almost certainly is.1

-

jimjames said:If your savings are in an account paying 0.25% I'd get that sorted asap and then decide your longer term plan. There's no point rushing into buying share based funds without doing some proper thinking about what you want and your risk profile so you might as well get the savings working while you do that.

I completely agree!. The problem is, I just don't know where to put those savings! I have a rainy day fund for 8 months (in addition to my monthly paycheck) and a large pot of savings (due to not bieng a homeowner) which i can invest in comfortably for at least 10 years. My attitude to risk is very high in the sense that I can stay the investment course for the long term and not rush to sell when things look bleak. Of course no one knows what the future holds but I would like to maximise my investments as much as i sensibly can and I know there are people with a wealth of knowledge which i would like to learn from....and share with others") 0

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards