We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

When does interest earned in a fixed rate savings account count as income for tax purposes?

Comments

-

There have been a number of threads in the recent past. The search function isn't particularly effective at finding them. My position is to avoid contradicting what the savings institution reports to HMRC, and as such I would just go with their approach (and if it might be material to my tax position, ask what it is in advance). I recall one poster who had discussed filing their own return declaring their interest in a more favourable manner for them than the savings institution declared (spread over tax years rather than all at maturity), though I cannot locate this thread now.

0 -

I think you might be correct, in that it depends on when the provider reports the interest to HMRC.coyrls said:In practice, I think it depends on when the provider reports the interest to HMRC. As Notepad_Phil suggests, where an annual interest summary is provided for tax purposes, then you should report that figure, even if the interest has been credited to the account and not paid to an external account.

The example of the Zopa 5-year fixed rate account unequivocally states that tax will only be considered on the interest at the completion of the 5-year term.

However, I've looked back at some multi-term fixed rate savings accounts I've had with Shawbrook in the recent past and for each a document is provided annually entitled "Tax Statement" containing a heading "CERTIFICATE OF DEDUCTION OF TAX - Statement for the purpose of section 975 of the Income Tax Act 2007" and detailing just the interest accrued in the preceding tax year along with the tax deducted (obviously £0.00). This suggests that Shawbrook report interest on an annual basis, based on when it's credited to the account, rather than at maturity.

So maybe the answer to the original question is that it actually depends on the provider. If so hopefully they're consistent across all their products so that it's at least possible to build a list of which institution does what.0 -

-

xylophone said:I did, thanks for posting it, and at first sight it does seem a slam dunk, but the 'HMRC spokesman' does not fully qualify their statement "In general, interest counts towards a saver's PSA when it 'arises' - that is when it is received, or made available to the recipient."i.e. they do say "Interest has been made available if it is credited to an account on which the account holder is free to draw." but not what "received" means.This is exactly as per the SAIM2440 tax page, and I wouldn't be surprised if the spokesman was just reading from that page, word for word.Most of the rest of the article then seems to be from the author rather than any spokesman and I'm not sure how much I trust the average financial journalist to get things 100% right.It would appear that either multiple banks and building societies are doing this wrong and sending annual interest information to the hmrc and their account holders when they shouldn't, or it's not as simple as the article would indicate e.g. perhaps in SAIM2400 where it says "interest arising in the tax year" "was held to include the ‘swelling of a person’s assets’ even where the person had no immediate right to the income."I doubt that the hmrc pages will ever be made any clearer, so the safest way if anyone is likely to be hit by multiple years of interest being made liable in the maturing year, is to ensure that they opt to get the interest paid out monthly or annually to a different account.2

-

Yes, I read the article too - thank you for taking the time and trouble to post the link. Thank you to Notepad_Phil for his summary and assessment of the article too - I agree with their conclusion and the accompanying suggestion.xylophone said:Did you have a look at this article?2 -

I have 2 and 3 years fixed rate accounts, the interest for which is not available to withdraw, and I have to pay tax on them every year.0

-

I’m hoping for 5% plus for 5 year fixed and maybe a 7 year from Shawbrook if their rates are good enough.

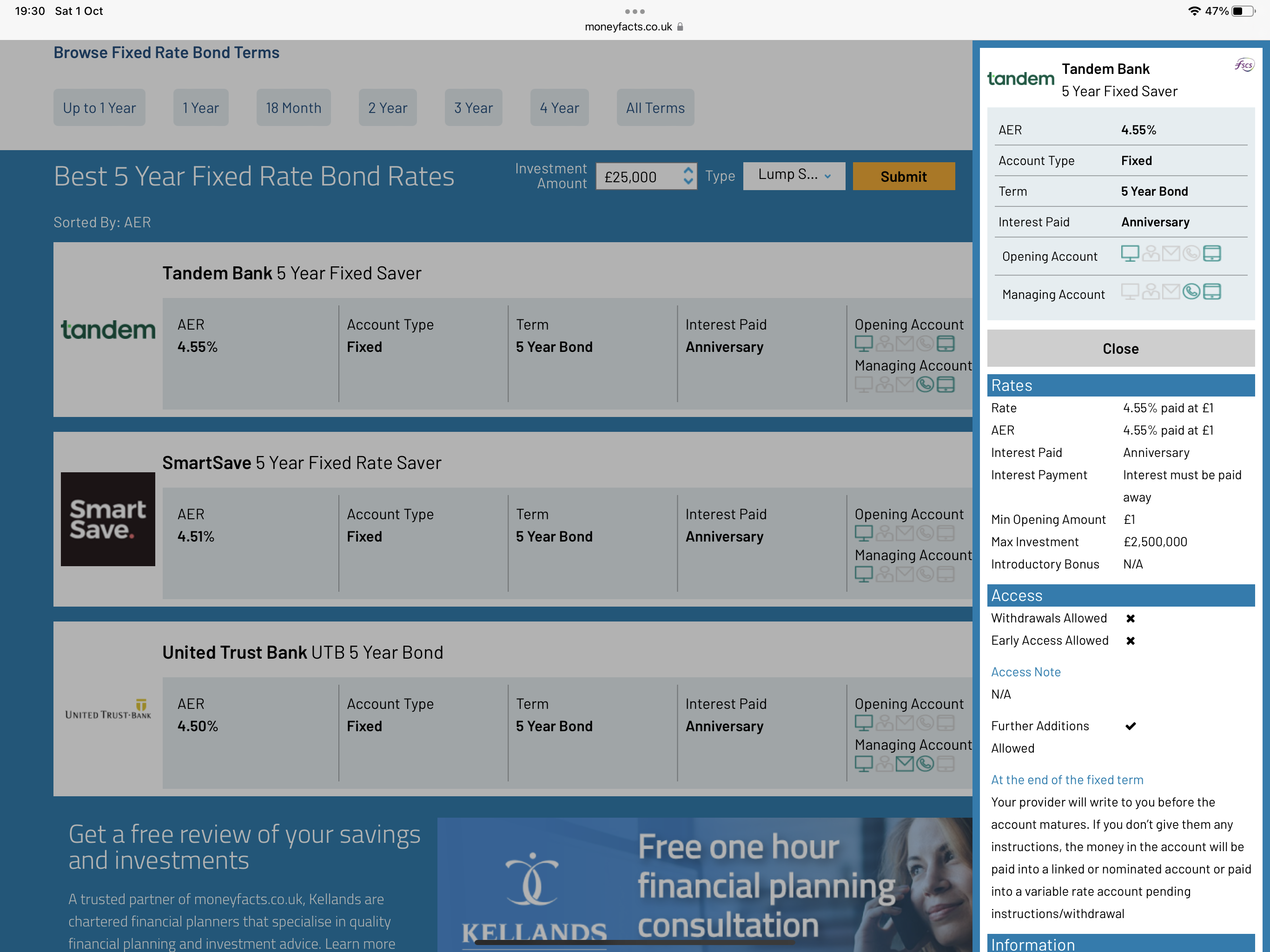

I need interest paid yearly and away so I can get an income and pay no tax or a minimum amount.

On money facts you can see the options.

Interest payment, interest must be paid away.

0 -

If you're bringing this up in the context of this thread about all interest potentially being declared at maturity, any account where interest is paid away will be spread over the tax years rather than being taxable at maturity.Bigwheels1111 said:I’m hoping for 5% plus for 5 year fixed and maybe a 7 year from Shawbrook if their rates are good enough.

I need interest paid yearly and away so I can get an income and pay no tax or a minimum amount.

On money facts you can see the options.

Interest payment, interest must be paid away.

0 -

Sorry should have made it clear, paid away each year is taxed that year, at maturity is taxed for all the years in one go.masonic said:

If you're bringing this up in the context of this thread about all interest potentially being declared at maturity, any account where interest is paid away will be spread over the tax years rather than being taxable at maturity.Bigwheels1111 said:I’m hoping for 5% plus for 5 year fixed and maybe a 7 year from Shawbrook if their rates are good enough.

I need interest paid yearly and away so I can get an income and pay no tax or a minimum amount.

On money facts you can see the options.

Interest payment, interest must be paid away.

0 -

Of the recent top of table providers, Zopa is the only one I'm aware of that makes interest all taxable at maturity. Most providers treat interest as arising monthly/quarterly/annually even if compounded in the account, but there could be others who take Zopa's approach.Bigwheels1111 said:

Sorry should have made it clear, paid away each year is taxed that year, at maturity is taxed for all the years in one go.masonic said:

If you're bringing this up in the context of this thread about all interest potentially being declared at maturity, any account where interest is paid away will be spread over the tax years rather than being taxable at maturity.Bigwheels1111 said:I’m hoping for 5% plus for 5 year fixed and maybe a 7 year from Shawbrook if their rates are good enough.

I need interest paid yearly and away so I can get an income and pay no tax or a minimum amount.

On money facts you can see the options.

Interest payment, interest must be paid away.

2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards