Current debt-free wannabe stats:

We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

PLEASE READ BEFORE POSTING: Hello Forumites! In order to help keep the Forum a useful, safe and friendly place for our users, discussions around non-MoneySaving matters are not permitted per the Forum rules. While we understand that mentioning house prices may sometimes be relevant to a user's specific MoneySaving situation, we ask that you please avoid veering into broad, general debates about the market, the economy and politics, as these can unfortunately lead to abusive or hateful behaviour. Threads that are found to have derailed into wider discussions may be removed. Users who repeatedly disregard this may have their Forum account banned. Please also avoid posting personally identifiable information, including links to your own online property listing which may reveal your address. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Shared ownership experts - advice on staircasing to 100%?

annetheman

Posts: 1,043 Forumite

I recently spoke with my mortgage advisor who helped me secure my shared ownership flat, and he believes I can afford to go to 75% right now (what I initially wanted) or maybe buy outright in 2024, but I am torn for a few reasons listed below. The big push is the RPI-linked rent increase!

What would you advise, given that flat prices haven't really budged much*? Here is some info about my situation:

Any advice will be great, is it worth doing it sooner e.g. as soon as I pay off my debts, given the crazy inflation-linked rent rise we're anticipating?

I can give some more clarifications if needed - thanks!

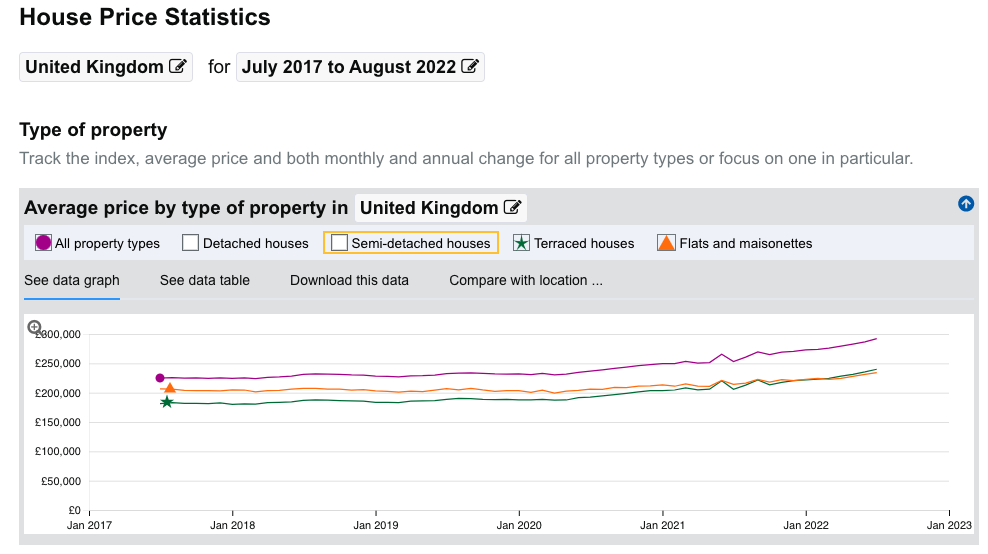

*Just to add that people aren't talking about the tanking of flat prices nearly as much as I thought. They have essentially flatlined and for the first time ever, this year terraced houses overtook flats in average price increase in the UK.

This has especially affected London, but it is a country-wide trend. Firm blame can be placed on the building safety crisis (NOT just cladding), the toxicity of feudal leasehold system that has been exposed by the cladding crisis and yes of course, a bit of the desire for more outdoor space since the pandemic.

Edit to add some links on this!

Land registry data:

What would you advise, given that flat prices haven't really budged much*? Here is some info about my situation:

- 30% share of flat purchased at 90% LTV in Feb 2021 (full purchase price £355,000).

- Mortgage is a 5 year fix, ending Feb 2026.

- At the time, gross earnings of £39,200.

- Earnings now gross £65,000 with approx 15% bonus (job started August 2022).

- Based on advisor's calculations, with predicted increase in rent next year, I will be paying around £300 less monthly if I buy outright (rent increase in insane).

- I am using £1,000 disposable each month to pay off debts of £17,000 by December 2023 using the snowball method.

- Expect an increase in salary with next promotion to around £85,000-90,000 base in the next 2 years; in a very secure pharma job, this is normal.

- After paying off debts, I can save at least £30,000 by Feb 2026 (end of fix) - currently snowball will be used to save (not factoring increase in pay).

- Flat sales have flatlined, I don't think I will have any real equity in the flat now.

- I want to see what happens to existing ground rents, as I am hoping, like new ground rents, legislation will be passed to remove (so I can do this within the new lease at the same time as repurchasing).

- I don't want to pay the early exit fee, even though it's not that bad, comparable to the savings I will make in rent on the 70% portion over the next 3.5 years.

- There are still products on the market at similar rates to what I have that might not be available later.

- He believes (but is not sure) I have enough equity for outright purchase.

- Increase in value could mean I can't afford it even later.

- As my rent is tied to RPI, he believes it will rocket on the 70% portion, so it is worth decreasing to 25% or getting rid altogether if I am in a position to.

Any advice will be great, is it worth doing it sooner e.g. as soon as I pay off my debts, given the crazy inflation-linked rent rise we're anticipating?

I can give some more clarifications if needed - thanks!

*Just to add that people aren't talking about the tanking of flat prices nearly as much as I thought. They have essentially flatlined and for the first time ever, this year terraced houses overtook flats in average price increase in the UK.

This has especially affected London, but it is a country-wide trend. Firm blame can be placed on the building safety crisis (NOT just cladding), the toxicity of feudal leasehold system that has been exposed by the cladding crisis and yes of course, a bit of the desire for more outdoor space since the pandemic.

Edit to add some links on this!

Land registry data:

Credit card: £8,524.31 | Loan: £3,224.80 | Student Loan (Plan 1): £5,768.55 | Total: £17,517.66

Debt-free target: 21-Mar-2027

Debt-free diary

Debt-free diary

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards