We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

We're aware that some users are currently experiencing errors on the Forum. Our tech team is working to resolve the issue. Thanks for your patience.

For a one year fixed, are there any more competitive comparison sites than MSE?

chris112

Posts: 127 Forumite

Based on the MSc website the best one you fix I could get is 3.32%,

but before I commit, I wanted to see if there are any other comparison websites that you use for even more competitive one year fixed rates?

but before I commit, I wanted to see if there are any other comparison websites that you use for even more competitive one year fixed rates?

I have read about raisin, but it seems a bit confusing and a bit too good to be true for me

0

Comments

-

I always check Moneyfacts: https://moneyfacts.co.uk/savings-accounts/1-year-fixed-rate-bonds/?quick-links-first=false

It looks like the two are in agreement. Sometimes brand new rates will appear on one before the other. Raisin is fine, but only occasionally has something better than what's available direct. Worth it for the cashback offer, however.

2 -

I would not fix for a year just now but would wait another couple of weeks1

-

As Daliah says, I'd probably hold fire before fixing for a year.

The Bank of England have their next review exactly 1 week from now, in which they'll review interest rates and (in my opinion) probably increase them by 0.5% - 0.75%.

This would almost certainly push up the interest many savings accounts are paying shortly after. The 3.32% fix could well be 4% by the end of the month.Know what you don't1 -

They went up 0.5% last month but savings rates didn't really have any big jumps (but I hope you're right!)Exodi said:As Daliah says, I'd probably hold fire before fixing for a year.

The Bank of England have their next review exactly 1 week from now, in which they'll review interest rates and (in my opinion) probably increase them by 0.5% - 0.75%.

This would almost certainly push up the interest many savings accounts are paying shortly after. The 3.32% fix could well be 4% by the end of the month.1 -

Didn't they? I thought they did, I think the best easy access account was previously Chase at 1.5% (but this offer was quite a bit above everyone else at the time and I think was partly done as a big marketing project), now the best easy access account is 1.85%.grahamgoo said:

They went up 0.5% last month but savings rates didn't really have any big jumps (but I hope you're right!)Exodi said:As Daliah says, I'd probably hold fire before fixing for a year.

The Bank of England have their next review exactly 1 week from now, in which they'll review interest rates and (in my opinion) probably increase them by 0.5% - 0.75%.

This would almost certainly push up the interest many savings accounts are paying shortly after. The 3.32% fix could well be 4% by the end of the month.

Know what you don't1 -

If you go to the easy access savings page of Moneyfacts, it shows the best rate as 1.81% with Shawbrook.

However this is only showing savings providers where you can go to the providers site through the Moneyfacts link provided ( and presumably they get a small commission)

If you untick the box ' show quick links first', then you get the full list, showing Al Rayan bank at the top with 2.1%3 -

Exodi said:

Didn't they? I thought they did, I think the best easy access account was previously Chase at 1.5% (but this offer was quite a bit above everyone else at the time and I think was partly done as a big marketing project), now the best easy access account is 1.85%.grahamgoo said:

They went up 0.5% last month but savings rates didn't really have any big jumps (but I hope you're right!)Exodi said:As Daliah says, I'd probably hold fire before fixing for a year.

The Bank of England have their next review exactly 1 week from now, in which they'll review interest rates and (in my opinion) probably increase them by 0.5% - 0.75%.

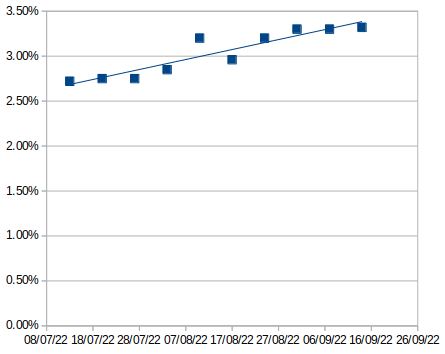

This would almost certainly push up the interest many savings accounts are paying shortly after. The 3.32% fix could well be 4% by the end of the month.The best easy access account pays 2.1%, Chase got pipped quite a while ago by Virgin Money, and subsequently Al Rayan stole lead position and has been raising its rate to stay at the top.You can use the MSE tip article archive to get a feel for this in the context of the best 1 year fix:- 13th July: Cynergy Bank 2.72%, min £10,000

- 20th July: Tandem 2.75%, min £1

- 27th July: Tandem 2.75%, min £1

- 3rd August: OakNorth Bank 2.85%, min £1

- Rate meeting 4th August

- 10th August: Union Bank of India 3.2%, min £5,000 (quickly pulled)

- 17th August: Cynergy Bank 2.96%, min £10,000

- 24th August: Monument Bank 3.2%, min £25,000

- 31st August: Tandem 3.3%, min £1

- 7th September: Tandem 3.3%, min £1

- 14th September: Virgin Money 3.32%, min £1

Rates are mostly driven by competition in the marketplace, and have been creeping up steadily. Union Bank of India was a bit of an outlier at the time. The danger I've seen the suggestion that it is a bad time to fix a few weeks before a rate meeting, around the time of a rate meeting, and a few weeks before the next meeting. I've yet to see anyone suggest a good time. Perhaps the view is that there hasn't been a good time to fix so far this year. Personally, I don't try to time the market, so I've been renewing my ladder of fixes as each one has matured.5 - 13th July: Cynergy Bank 2.72%, min £10,000

-

Oh brilliant, thanks for linking that. I think that answers grahamgoo suggestion that rates didn't change with the BoE increase. It looks like on average they increased completely in line with the increase.masonic said:Exodi said:

Didn't they? I thought they did, I think the best easy access account was previously Chase at 1.5% (but this offer was quite a bit above everyone else at the time and I think was partly done as a big marketing project), now the best easy access account is 1.85%.grahamgoo said:

They went up 0.5% last month but savings rates didn't really have any big jumps (but I hope you're right!)Exodi said:As Daliah says, I'd probably hold fire before fixing for a year.

The Bank of England have their next review exactly 1 week from now, in which they'll review interest rates and (in my opinion) probably increase them by 0.5% - 0.75%.

This would almost certainly push up the interest many savings accounts are paying shortly after. The 3.32% fix could well be 4% by the end of the month.The best easy access account pays 2.1%, Chase got pipped quite a while ago by Virgin Money, and subsequently Al Rayan stole lead position and has been raising its rate to stay at the top.You can use the MSE tip article archive to get a feel for this in the context of the best 1 year fix:- 13th July: Cynergy Bank 2.72%, min £10,000

- 20th July: Tandem 2.75%, min £1

- 27th July: Tandem 2.75%, min £1

- 3rd August: OakNorth Bank 2.85%, min £1

- Rate meeting 4th August

- 10th August: Union Bank of India 3.2%, min £5,000 (quickly pulled)

- 17th August: Cynergy Bank 2.96%, min £10,000

- 24th August: Monument Bank 3.2%, min £25,000

- 31st August: Tandem 3.3%, min £1

- 7th September: Tandem 3.3%, min £1

- 14th September: Virgin Money 3.32%, min £1

Rates are mostly driven by competition in the marketplace, and have been creeping up steadily. Union Bank of India was a bit of an outlier at the time. The danger I've seen the suggestion that it is a bad time to fix a few weeks before a rate meeting, around the time of a rate meeting, and a few weeks before the next meeting. I've yet to see anyone suggest a good time. Perhaps the view is that there hasn't been a good time to fix so far this year. Personally, I don't try to time the market, so I've been renewing my ladder of fixes as each one has matured.

I'm not sure I agree with your view that people are constantly suggesting to hold off to the next BoE increase, or that there is no good time to fix when the above almost proves the opposite? Fixing shortly after (a few weeks to give banks time to decide on their offerings) a BoE increase seems to be optimal.

Surely you can agree that fixing just before a rate meeting (I'll caveat this with - where it is widely held rates will increase) probably isn't the best idea.Know what you don't1 - 13th July: Cynergy Bank 2.72%, min £10,000

-

My searches tend to include this...

https://www.thisismoney.co.uk/money/article-1621507/Best-savings-rates-Fixed-rate-accounts.html

1 -

Exodi said:

Oh brilliant, thanks for linking that. I think that answers grahamgoo suggestion that rates didn't change with the BoE increase. It looks like on average they increased completely in line with the increase.masonic said:Exodi said:

Didn't they? I thought they did, I think the best easy access account was previously Chase at 1.5% (but this offer was quite a bit above everyone else at the time and I think was partly done as a big marketing project), now the best easy access account is 1.85%.grahamgoo said:

They went up 0.5% last month but savings rates didn't really have any big jumps (but I hope you're right!)Exodi said:As Daliah says, I'd probably hold fire before fixing for a year.

The Bank of England have their next review exactly 1 week from now, in which they'll review interest rates and (in my opinion) probably increase them by 0.5% - 0.75%.

This would almost certainly push up the interest many savings accounts are paying shortly after. The 3.32% fix could well be 4% by the end of the month.The best easy access account pays 2.1%, Chase got pipped quite a while ago by Virgin Money, and subsequently Al Rayan stole lead position and has been raising its rate to stay at the top.You can use the MSE tip article archive to get a feel for this in the context of the best 1 year fix:- 13th July: Cynergy Bank 2.72%, min £10,000

- 20th July: Tandem 2.75%, min £1

- 27th July: Tandem 2.75%, min £1

- 3rd August: OakNorth Bank 2.85%, min £1

- Rate meeting 4th August

- 10th August: Union Bank of India 3.2%, min £5,000 (quickly pulled)

- 17th August: Cynergy Bank 2.96%, min £10,000

- 24th August: Monument Bank 3.2%, min £25,000

- 31st August: Tandem 3.3%, min £1

- 7th September: Tandem 3.3%, min £1

- 14th September: Virgin Money 3.32%, min £1

Rates are mostly driven by competition in the marketplace, and have been creeping up steadily. Union Bank of India was a bit of an outlier at the time. The danger I've seen the suggestion that it is a bad time to fix a few weeks before a rate meeting, around the time of a rate meeting, and a few weeks before the next meeting. I've yet to see anyone suggest a good time. Perhaps the view is that there hasn't been a good time to fix so far this year. Personally, I don't try to time the market, so I've been renewing my ladder of fixes as each one has matured.

I'm not sure I agree with your view that people are constantly suggesting to hold off to the next BoE increase, or that there is no good time to fix when the above almost proves the opposite? Fixing shortly after (a few weeks to give banks time to decide on their offerings) a BoE increase seems to be optimal.

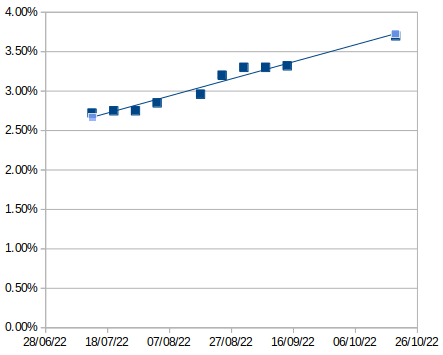

Surely you can agree that fixing just before a rate meeting (I'll caveat this with - where it is widely held rates will increase) probably isn't the best idea.Perhaps plotting the above data will help? I don't think you can rely on that outlier point from 10th August being repeated after next week's announcement. These will come along completely at random when a new bank wants to attract funds very quickly.The BoE meetings are on a 6 week cycle (normally). Over the above 9 week period, rates have increased by an average of 0.06% per week. By staying in easy access for this period, one has had an opportunity cost of 0.02% per week (easy access has been an average of ~1.1% below the top 1 year fix). Fixing using the 24th August 3.2% offering, for example, a few weeks after the rate decision, will turn out to be a bad time to fix if another 0.5%+ rise happens next week and rates are ~3.7% in 4 weeks time (~19th October). At that point, if there's another rise in the 3rd November meeting, an argument could be made to hold off until a few weeks after that. And so the cycle repeats until we think the MPC will hold rates steady.Or above rationale in a chart (outlier removed, trend extrapolated, late August fix sensible?):

I don't think you can rely on that outlier point from 10th August being repeated after next week's announcement. These will come along completely at random when a new bank wants to attract funds very quickly.The BoE meetings are on a 6 week cycle (normally). Over the above 9 week period, rates have increased by an average of 0.06% per week. By staying in easy access for this period, one has had an opportunity cost of 0.02% per week (easy access has been an average of ~1.1% below the top 1 year fix). Fixing using the 24th August 3.2% offering, for example, a few weeks after the rate decision, will turn out to be a bad time to fix if another 0.5%+ rise happens next week and rates are ~3.7% in 4 weeks time (~19th October). At that point, if there's another rise in the 3rd November meeting, an argument could be made to hold off until a few weeks after that. And so the cycle repeats until we think the MPC will hold rates steady.Or above rationale in a chart (outlier removed, trend extrapolated, late August fix sensible?): 1

1 - 13th July: Cynergy Bank 2.72%, min £10,000

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards