We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Should I be worried

Comments

-

Pleased you got it sorted with the revenue.

I hope that the state pension remains as the foundation of most ordinary peoples retirement planning. It seems to be a better fit for the many. Maybe it should even be brought up to European standards in the future. The drip feed narrative that everybody will have to go private in the future should be viewed cautiously IMHO.Watching a “safe” private pension drop (another 1.5% today) at nearly five times the rate of a riskier pension has done nothing for my belief in the pension industry or its forecasts. I know the world is a bit all over the place at the moment and drops will happen and recoveries will come but that just strengthens my views.

Imagine being ready to retire now with your pot in a “safe” fund and then realising you may just have to carry on working because your fund is plummeting.

but what do I know. I’m still very grateful for the advice I’ve received here.0 -

Imagine being ready to retire now with your pot in a “safe” fund and then realising you may just have to carry on working because your fund is plummeting

It is true that very unusually 'safe' funds have dropped pretty much the same as riskier funds this year. It is also true you can be a bit unlucky about the exact timing when you retire. (I know I retired 14 months ago)

However two important points ;

If you retire with a pot, that is so badly affected that you need to start work again, then you retired with too small a pot in the first place. Or not enough cash to help you through a bad year.

The current situation is not great, but funds have not 'plummeted'. Mine are the same as they were 18 months ago and still a lot higher than they were 5 years ago. Gyrations in the markets have been relatively modest, compared to some proper crashes in the past. The high inflation is actually more of an issue though.

0 -

Many people are in exactly that position. I see no shame in that as not everyone has enjoyed the comfort blanket of a DB scheme in their working life. I see no parity in my funds, with the safe fund nosediving at almost five times the rate of the riskier policy as I’ve previously stated. If someone has a big enough pot not to be bothered by what’s happening at the moment, or enough in the bank to tide them over (presuming the normal guesstimations for any recovery apply) then I would wonder why they are seeking advice here? It has been kindly explained that these are exceptional circumstances. Hopefully we will bob up and out of exceptional circumstances before they turn into something far worse. I doubt any crash or depression came from unexceptional circumstances. Maybe nobody will have a big enough pot then?However two important points ;If you retire with a pot, that is so badly affected that you need to start work again, then you retired with too small a pot in the first place. Or not enough cash to help you through a bad year.

Not that you are wrong of course.

I’ll keep updating the graphs for now. See how we are in a wee while.0 -

And over the cliff we go. 50/50 safe my backside. If these sort of pension funds are the norm in workplace schemes then why are the news channels ignoring the danger. Maybe because core voters of a certain age would go scary Mary.

Who benefits from the catastrophe of the last few weeks. Crispin Odey, hedge fund manager? When the man who used to employ the current incumbent at No11 bets against government bonds (tipped off) and calls that treachery,”the gift that keeps on giving” then something is broken. The last plummet was caused by a virus. There’s more than one kind of virus.

Yes I know that holding out is sensible but I just cannot accept that this financial model for most working peoples retirement is a reliable mechanism. Where’s there’s a vault stuffed with money there’s always gonna be bank robbers and the new sheriff is (insert your own answer here. I can’t write what I think he is).1 -

Honey I shrunk the Quids indeed

0 -

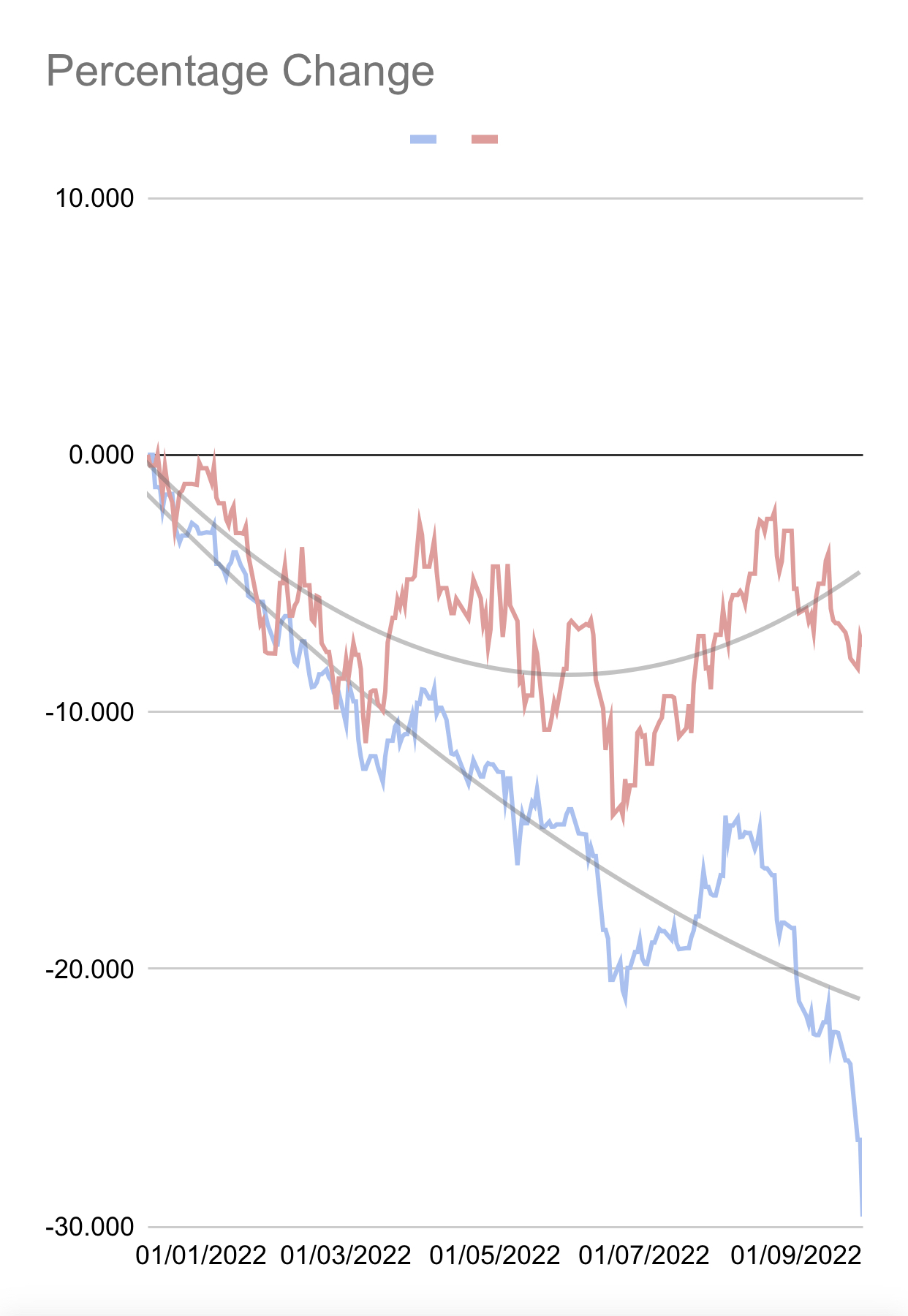

pretty graph but it could do with some labelsI’m a Senior Forum Ambassador and I support the Forum Team on the Pensions, Annuities & Retirement Planning, Loans

& Credit Cards boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com.

All views are my own and not the official line of MoneySavingExpert.1 -

Two funds

Plots show % change since Xmas 2021

Red = Reassure - Pensions Global Equity Pension Accumulator Series 01

Blue = Aegon - 50/50 Cautious Managed Selection (Arc) Pn

Doesn't look pretty to me. The original post asked Should I Be Worried. I think it needs editing to Should Everyone Be Worried. Finally the BBC has started reporting on pension funds diving and it’s taken a kamikaze chancellor to make them look. Even lockdown didn’t crash funds so spectacularly. Almost as if it’s deliberate.0 -

Doesn't look pretty to me. The original post asked Should I Be Worried. I think it needs editing to Should Everyone Be Worried.

Why should everyone be worried?

Finally the BBC has started reporting on pension funds diving and it’s taken a kamikaze chancellor to make them look.You have misunderstood what they are reporting.

Even lockdown didn’t crash funds so spectacularly. Almost as if it’s deliberate.Yes, they did. Just not as much at the lowest risk end. Anyone who was low/medium or higher would have lost more during 2020.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0 -

People on this forum were warning about bonds/gilts were likely to go into decline two years ago, after years of above average growth. Many investors and advisors reduced their bondholdings. They approx flatlined for quite a while, but then started declining steeply from Dec last year, due to inflation and interest rate rises and the future prospect of more of the same. Some bond funds were already 30% down before the mini budget, although it has exacerbated the decline further.anfirmor said:Two funds

Plots show % change since Xmas 2021

Red = Reassure - Pensions Global Equity Pension Accumulator Series 01

Blue = Aegon - 50/50 Cautious Managed Selection (Arc) Pn

Doesn't look pretty to me. The original post asked Should I Be Worried. I think it needs editing to Should Everyone Be Worried. Finally the BBC has started reporting on pension funds diving and it’s taken a kamikaze chancellor to make them look. Even lockdown didn’t crash funds so spectacularly. Almost as if it’s deliberate.0 -

Thank you for your advice. I wish I had been scouring the forum two years when you predicted bond failure but I’m learning more each day. Like just realising many providers no longer automatically de risk workplace pensions in the 10 year lead up to retirement.

I suppose there’s a prediction that the Bank of England would need to launch the lifeboat to save pension funds. Again didn’t spot it.

Any predictions for the next two years? Many of us who aren’t as informed could use some insight. I’m sure it would be very well received.

And you’re quite right. In lockdown my workplace pension dropped rapidly by roughly 2/3 but it also recovered smartly. Would you be so kind as to share your opinions for any recovery in typical 50/50 schemes in the current financial/political climate and timescale for that?0

And over the cliff we go. 50/50 safe my backside. If these sort of pension funds are the norm in workplace schemes then why are the news channels ignoring the danger. Maybe because core voters of a certain age would go scary Mary.

And over the cliff we go. 50/50 safe my backside. If these sort of pension funds are the norm in workplace schemes then why are the news channels ignoring the danger. Maybe because core voters of a certain age would go scary Mary.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.8K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards