We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

deferred DB pension Revaluation. Are the 5%, 2.5% limits compounded? Also partial years.

Comments

-

And if someone says they are retiring on 15/6/2022 in your example, would the pension company pick up the phone and point out to them - do you realise if you wait 6 days you will get a much higher pension for the rest of your life?zagfles said:Pat38493 said:

I must be missing something because they way I read your comments, if I retire in 2023 for example, I would get the exact same starting pension no matter whether I retired any day from 1st January to 31st December (which I think is what most people would assume at first)zagfles said:

What do you think has changed? Reread them, there's no contradiction.Pat38493 said:

Did the rules change in the meantime then? I found the thread I was referring to and it's actually older than this one not newer. See the OP in this thread and follow up replies:zagfles said:Pat38493 said:

On another thread, I remember reading that the exact date of deferral of the pension is relevant for this also but I didn't see that mentioned on this resurrected thread?Pensions_matter_2 said:Looks like latest revaluation Order is just out, for those who are interested.

https://www.legislation.gov.uk/uksi/2022/1229/article/2/made

My understanding was for example if your pension was deferred on 1st June 2005, if you took your DB benefit on 1st Jan 2023, they would actually use the 62.8% number but if you took the benefit on 1st August 2023, they would use the 67.8% number or something like that? Is that correct or did I misunderstood that at the time - the message seemed to be that you are almost always better to take your DB pension after the anniversary date of deferral?

In this thread is seems ot say that it just rolls over by year but this was contrary to the other thread I was using.In my first reply: "Partial years usually are lost. You only get whole years, "

Rules on using Occupational Pensions Revaluation Orders — MoneySavingExpert Forum

However in the other thread it implies you will almost always get a higher pension if you retire after the anniversary date of your pension deferral.

I guess maybe the issue is that by “whole years” you mean years from date of deferral?Yes, so if you went deferred on 20/6/2015 and took the pension on 15/6/2022 you'd only get 6 years (1/1/2016-31/12/2021 inflation), because it's only 6 whole years despite being nearly 7.But if you waited till 21/6/2022 you get 7 years (1/1/2015 - 31/12/2021).If you waited a bit longer till 10/1/2023, it's still 7 whole years but different years (1/1/2016-31/12/2022).Particularly relevant now - if you're thinking about taking a DB pension now it could be worth delaying till the the new year!

Also, the yearly table row labels are completely mislabelled - they should say something like “x whole years cumulated inflation from deferral date” or suchlike. Is this maybe because these tables are used for some other purposes beyond what we are discussing here?

Not to mention as pointed out by the OP I think, it would be child’s play using modern calculations to pro rate the pension based on months or even days.0 -

In general no a company wouldnt do that, the odd person might especially perhaps if you were having general discussions on the phone, but for most it steers too cose to giving financial advise which is a massive no no.Pat38493 said:

And if someone says they are retiring on 15/6/2022 in your example, would the pension company pick up the phone and point out to them - do you realise if you wait 6 days you will get a much higher pension for the rest of your life?zagfles said:Pat38493 said:

I must be missing something because they way I read your comments, if I retire in 2023 for example, I would get the exact same starting pension no matter whether I retired any day from 1st January to 31st December (which I think is what most people would assume at first)zagfles said:

What do you think has changed? Reread them, there's no contradiction.Pat38493 said:

Did the rules change in the meantime then? I found the thread I was referring to and it's actually older than this one not newer. See the OP in this thread and follow up replies:zagfles said:Pat38493 said:

On another thread, I remember reading that the exact date of deferral of the pension is relevant for this also but I didn't see that mentioned on this resurrected thread?Pensions_matter_2 said:Looks like latest revaluation Order is just out, for those who are interested.

https://www.legislation.gov.uk/uksi/2022/1229/article/2/made

My understanding was for example if your pension was deferred on 1st June 2005, if you took your DB benefit on 1st Jan 2023, they would actually use the 62.8% number but if you took the benefit on 1st August 2023, they would use the 67.8% number or something like that? Is that correct or did I misunderstood that at the time - the message seemed to be that you are almost always better to take your DB pension after the anniversary date of deferral?

In this thread is seems ot say that it just rolls over by year but this was contrary to the other thread I was using.In my first reply: "Partial years usually are lost. You only get whole years, "

Rules on using Occupational Pensions Revaluation Orders — MoneySavingExpert Forum

However in the other thread it implies you will almost always get a higher pension if you retire after the anniversary date of your pension deferral.

I guess maybe the issue is that by “whole years” you mean years from date of deferral?Yes, so if you went deferred on 20/6/2015 and took the pension on 15/6/2022 you'd only get 6 years (1/1/2016-31/12/2021 inflation), because it's only 6 whole years despite being nearly 7.But if you waited till 21/6/2022 you get 7 years (1/1/2015 - 31/12/2021).If you waited a bit longer till 10/1/2023, it's still 7 whole years but different years (1/1/2016-31/12/2022).Particularly relevant now - if you're thinking about taking a DB pension now it could be worth delaying till the the new year!

Also, the yearly table row labels are completely mislabelled - they should say something like “x whole years cumulated inflation from deferral date” or suchlike. Is this maybe because these tables are used for some other purposes beyond what we are discussing here?

Not to mention as pointed out by the OP I think, it would be child’s play using modern calculations to pro rate the pension based on months or even days.

Because ultimately its your responsibility to understand your pension, recreating the calculations people are referencing in this thread might be too much, but everyone should be able to understand the concept You would have had your whole working life to read booklets, ask questions, google information, speak to advisers etc.

As for the last point, doesnt matter how easy it is, the pension schemes rules were written that it isnt done like that. DB Schemes are gold dust these days, people with them should be happy they have them in the first place, wishing it had additional complexity could backfire given it would do nothing but add to the financial strain of the schemes it what is already a massive financial burden for the employers covering them, and make it more likely the Scheme closes, stops any future discrtionary increases, struggles and goes into the PPF etc0 -

Just found this thread.

When I asked Mercer to explain the sawtooth pattern for retiring on different months over the coming year they replied like they didn't understand the question, saying that they didn't produce the graph and didn't know what the figures relate to.

I was trying to find out if the apparent loss was real or maybe it was counteracted (almost immediately.) by a revaluation of the in-payment amount. eg if you retire on 15/6 you will get £9000 but on 21/6 this will be uplifted to £9400.

I still don't know what the details of the in-payment revaluations are. Will be asking soon, when I get a proper quote for taking my pension July 2025 (Deferment date mid June).0 -

'Revaluation' as a term is used for increases before the pension comes into payment, so 'in-payment revaluation' may appear oxymoronic if you use the phrase with a pension administrator. How schemes deal with the first pension increase in payment just varies, some will give a full year's increase, others will pro-rate somehow, others still might not give any increase at all. Also the treatment of any GMP and excess will very likely be different (post-88 GMP after GMP Age gets the full year's increase, but this is correlative to the fact there's no GMP revaluation for the final, part tax year before GMP Age).optoutDB said:Just found this thread.

When I asked Mercer to explain the sawtooth pattern for retiring on different months over the coming year they replied like they didn't understand the question, saying that they didn't produce the graph and didn't know what the figures relate to.

I was trying to find out if the apparent loss was real or maybe it was counteracted (almost immediately.) by a revaluation of the in-payment amount. eg if you retire on 15/6 you will get £9000 but on 21/6 this will be uplifted to £9400.

I still don't know what the details of the in-payment revaluations are. Will be asking soon, when I get a proper quote for taking my pension July 2025 (Deferment date mid June).1 -

hyubh said:'Revaluation' as a term is used for increases before the pension comes into payment, so 'in-payment revaluation' may appear oxymoronic if you use the phrase with a pension administrator.Noted. In payment uplift ?

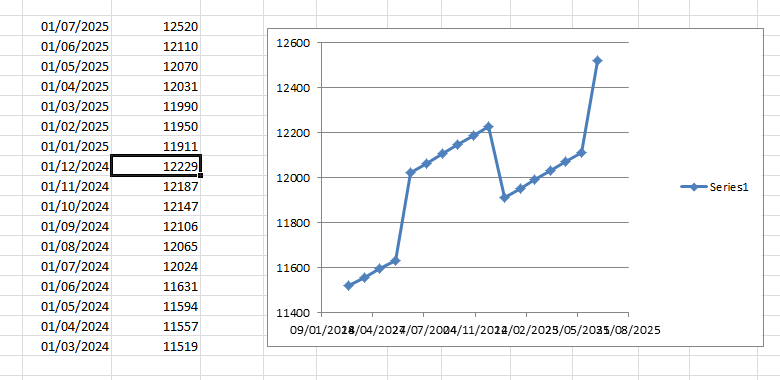

Is this the regular sawtooth pattern ? This was the output from the Retirement Illustrator that I asked Mercer to explain. ( My deferment date was something like 10 June). Note: the input to the illustrator is a date, and the primary output is a the yearly pension under option 1, so I didn't feel the need to add column headings. 0

0 -

This is a pretty old thread, and some other threads since then have put a further wrinkle on this. With some schemes, including some that are administrated by Mercer, the revlauation is done in a different way - it's done by revaluating the pension to your NRA first, using a forecasted rate for unknown periods. After that they apply a (higher) early retirement factor if you are retiring early.optoutDB said:Just found this thread.

When I asked Mercer to explain the sawtooth pattern for retiring on different months over the coming year they replied like they didn't understand the question, saying that they didn't produce the graph and didn't know what the figures relate to.

I was trying to find out if the apparent loss was real or maybe it was counteracted (almost immediately.) by a revaluation of the in-payment amount. eg if you retire on 15/6 you will get £9000 but on 21/6 this will be uplifted to £9400.

I still don't know what the details of the in-payment revaluations are. Will be asking soon, when I get a proper quote for taking my pension July 2025 (Deferment date mid June).

For schemes which use this method, you cannot game the system in the way described in this thread because it's only the ERF date and amount that would change - the revaluation is fixed by the NRA date of your pension and the original deferral date.

If the scheme revalues the pension to the date you want to retire, and then applies the ERF from there, that's when the points discussed in this thread seem to apply.0 -

I've got 2 quotes coming (for 1st June and 1st July). If the in-payment increments are not detailed I will get that information. And then I will take whichever is best [ unless I decide to not take it yet

") ] 0

] 0 -

All I know is that my deferred pension goes up each month. Straight forward as they’ll be paying it for less.

As for catching up with inflation (I.e. where inflation exceeds the cap) there is nothing of note in the scheme documentation, so I’ve got no idea.0 -

Yup that's exactly what you get with statutory revaluation. Monthly the pension is going up around £40 because there's a month's less ERF. Then in July there's around a £400 jump because you get an extra year's inflation. Then in Jan there's a drop because you lose inflation in the year you left and it gets replaced by last's year's inflation. So inflation in the year you left must have been higher than current inflation. All explained in this thread and the previous one.optoutDB said:hyubh said:'Revaluation' as a term is used for increases before the pension comes into payment, so 'in-payment revaluation' may appear oxymoronic if you use the phrase with a pension administrator.Noted. In payment uplift ?

Is this the regular sawtooth pattern ? This was the output from the Retirement Illustrator that I asked Mercer to explain. ( My deferment date was something like 10 June). Note: the input to the illustrator is a date, and the primary output is a the yearly pension under option 1, so I didn't feel the need to add column headings.

In-payment indexation usually uses completely different rules not linked at all to revaluation in deferment.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards