We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Drawing a Regular Income which way is best?

datadezign

Posts: 44 Forumite

I need to replace my annual income from funds invested. I have calculated that looking at say a 10-15 year average returns in a medium type risk should achieve this.

My question is:-

What is the best approach, to enable income drawdown from the invested funds?

ALSO with the current economic volatility should I defer my first time investment into the markets, or drip feed in tranches?

What is the best approach, to enable income drawdown from the invested funds?

ALSO with the current economic volatility should I defer my first time investment into the markets, or drip feed in tranches?

0

Comments

-

Depends on your circumstances & how much you need.

I'd take the money, buy investment property. Rents provide regular income & house price inflation provides capital gain.

If you are smart you can get a yield way above what you can get elsewhere.

You can leverage by using what you have as a deposit and borrowing the rest to increase income & potential capital gain.0 -

Income isn't regular if they tenant doesn't pay. It could be a significant tax hit and not very tax efficient to do that and potentially much lower yield than income from a fund as well as much more hassle.subjecttocontract said:Depends on your circumstances & how much you need.

I'd take the money, buy investment property. Rents provide regular income & house price inflation provides capital gain.

If you are smart you can get a yield way above what you can get elsewhere.

You can leverage by using what you have as a deposit and borrowing the rest to increase income & potential capital gain.Remember the saying: if it looks too good to be true it almost certainly is.2 -

I've been doing it for 25 years.....

* missed payments very rare.

* no significant tax hit.

* Yields up to 15%.

Nothing is certain in life (except death & taxes)......and there is certainly no guarantees from funds.

It's a free choice.

0 -

* Yields up to 15%.Buying a property today expecting a 15% yield is unheard of unless you have building/refurbishment skills.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.3 -

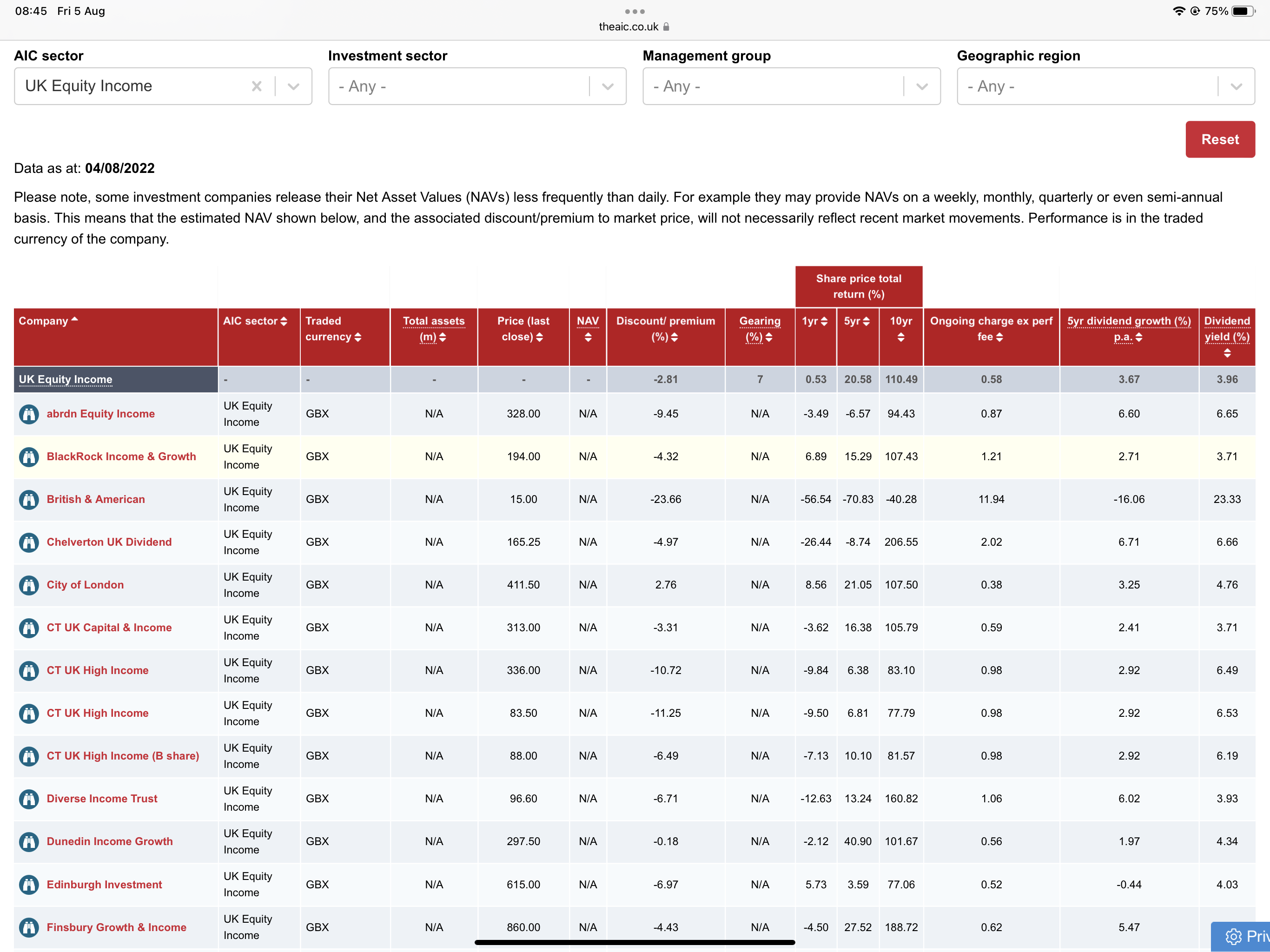

I thought you were looking for an IFA to help you with this? Anyway, one way is to invest in a range of income paying investment trusts (IT), OEICs and/or ETFs. For instance, a well known IT is City of London (LSE:CTY) with a current dividend yield of 4.76% and invests mostly in UK 'blue chip' dividend payers.datadezign said:I need to replace my annual income from funds invested. I have calculated that looking at say a 10-15 year average returns in a medium type risk should achieve this.My question is:-

What is the best approach, to enable income drawdown from the invested funds?

ALSO with the current economic volatility should I defer my first time investment into the markets, or drip feed in tranches?

https://www.theaic.co.uk/aic/find-compare-investment-companies?sec=UGI&sortid=Name&desc=false

1 -

It's certainly not unheard of, some auction purchases can provide this level of return.dunstonh said:* Yields up to 15%.Buying a property today expecting a 15% yield is unheard of unless you have building/refurbishment skills.

We dont know what skills the OP has or is prepared to employ.

Property has the advantage of regular rental income and capital appreciation.

0 -

Property is illiquid & expensive to trade.subjecttocontract said:

It's certainly not unheard of, some auction purchases can provide this level of return.dunstonh said:* Yields up to 15%.Buying a property today expecting a 15% yield is unheard of unless you have building/refurbishment skills.

We dont know what skills the OP has or is prepared to employ.

Property has the advantage of regular rental income and capital appreciation.If you get Capital Appreciation you’ll create huge Capital Gains Tax liability income tax is due on rent.Funds in an wrapper (and even outside a wrapper to some extent). Suffer none of these.The advantage of property is you can easily get leverage compared with funds. If only a building society had lent me 250k so I could buy £300k of SMT in 2008.3 -

Discussion so far has been about using ‘at risk’ investments, investments with risks of failure: your rental property burns down; the share market collapses for 10 years; your bonds default; inflation trashes your assets’ values. Those risks can be managed but not eliminated easily, although having a big margin of safety with assets which are worth a lot more than one would usually need protects against catastrophes.

But the other approach is to use at least some of your wealth to buy guaranteed regular income; a liability matching portfolio, or liability driven investing, basically focussing on recognising how much income you need for life and investing appropriately to ensure you get it.

You’ll easily find information on this approach which would involve a lifetime inflation linked annuity for many people, amongst other strategies, and you can read an accessible approach here https://doczz.net/doc/8871437/applying-life-cycle-economics

1 -

Answer depends on how much net (liquid) cash you have to play with.1

-

ALSO with the current economic volatility should I defer my first time investment into the markets, or drip feed in tranches?

This question is probably the one most frequently asked on this forum. 'Should I go all in or drip feed' and usually followed by ' in the current turmoil' which could be today or 6 months ago or 18 months ago or 5 years ago etc as there is never a time when the financial markets are stable. The problem is nobody knows the future direction of the markets.

The answer is statistically it is better to go all in, as markets rise more often then they fall. The mantra being 'time in the market not timing the market' However the natural loss aversion of human beings means that many find this difficult to do, and feel more comfortable with drip feeding.

You can go in the middle and say put 40% in now, 30% in 3 months and 30 % in 6 months, but in the end it is your decision.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.3K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards