We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Aiming to be mortgage free before I am 62!

Comments

-

He is the king of the splurge so he isn't always great at paying half towards his driving lessons so I am having to be bad cop with him at the moment.Sarahwithlove said:That's such a good idea getting your son to pay some of his salary towards board. It helps him learn to budget and understand that you don't get to keep it all for fun. Is he a natural saver or does he spend it? I did a mixture of both and was able to pay for my own driving lessons, car and insurance as a result. Hopefully he will save some as well.

His part time job isn't many hours or well paid but it is nice seeing a tiny savings start to appear. I like that he doesn't know the board is going into an account so anything is a bonus!

I am gutted not to have won on the premium bonds again. Only 2 more draws until I cash them in

Total Debt May 21 £20,490.44 DEBT FREE DATE 29/7/22

Mortgage balance May 21 £177,096.19. Now £143,070.41

Mortgage free date. At start of sole mortgage = July 2042

2024 SAVINGS FOCUS - get rid of the car finance. £12,706.25 PAID OFF

2025 Savings Focus - 33.3/33.3/33.3 split; savings for house renovations (bathrooms/garden/kitchen; whichever collapses first), save for a family holiday (probably our last one!) and paydown/offset the mortgage. Total pot = £4238.560 -

I had an underperforming 2024 on PBs as well . So annoying

glad you slowly training DS upDON'T BUY STUFF (from Frugalwoods)

No seriously, just don’t buy things. 99% of our success with our savings rate is attributed to the fact that we don’t buy things... You can and should take advantage of discounts.... But at the end of the day, the only way to truly save money is to not buy stuff. Money doesn’t walk out of your wallet on its own accord.

https://forums.moneysavingexpert.com/discussion/6289577/future-proofing-my-life-deposit-saving-then-mfw-journey-in-under-13-years#latest0 -

I am having an end if year review session with my budget planner, which I thought would be a little depressing as my mortgage overpayments just haven't been happening. However, I have quite a bit to be proud of alongside giving myself a bit of a slap to not get too sidetracked again!

I have joined the 2025 mortgage challenge and am aiming for £3000 overpayment. I am hoping to be a bit more focused on making those overpayments but also acknowledging my regular overpayments. I had always said I would keep paying the £1100 a month I had to pay initially but this felt like a bigger deal/impact when my mortgage was on a lower % to start with but I should still be really pleased I overpay £83.22 as part of my direct debit.

Annoyingly, I can't make overpayments online so I have to call up. I might have to build little extra payments to pay in a chunk rather than ringing to pay every 19p separately!

I am well on track to pay off my car in early 2025 but I do have a niggle in the back of my head that my car needs an MOT and service. Knowing my luck that could be scary!

I had said a while ago that my 2025 strategy was 50/50 holiday savings and mortgage overpayments but I have adapted to 33.3/33.3/33.3 to build a pot for house savings. My garden is decked with rotting decking and a fence that might not withstand another storm. We have 4 bathrooms, all of which are falling apart. The kitchen cupboard doors are falling off with carcasses that aren't much better and the space doesn't really work for us anymore. If I changed the kitchen then i would need to have the tiling pulled up for the full downstairs. The hall and stairs carpet is patchwork.

I don't really have a priority with the house as I think I will have to be governed by which bit presents itself as a priority first!

2024 goal review

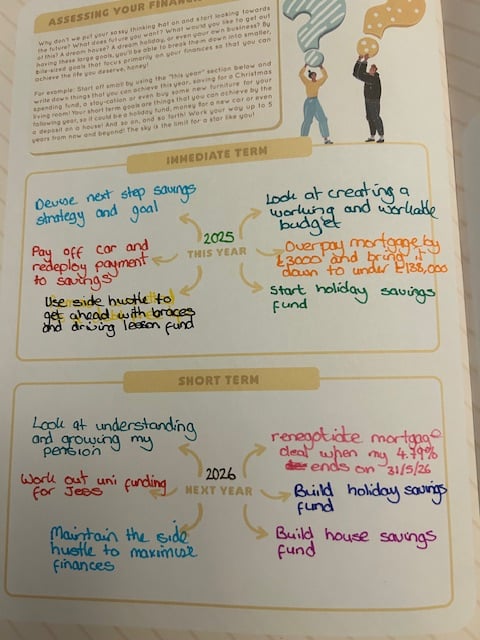

Immediate term/this year

Look at next step savings strategy / I ticked that off at the start of 2024

Build savings for car balloon payment £8156.25 due 31/3/26 / I have the balloon payment and more saved

Remain committed to a debt free life ? I had a little blip of using creation finance from currys but I paid it off way before any interest was charged and I think i needed to be able to cope with the idea of tiny temporary debt!

Look at creating a working a workable budget x Budgeting remains my nemesis!

Pay down mortgage: January 2025 aim £145,000 x The mortgage came down but not quite far enough and I won't hit that in January either

Short term/next year

Save for twins' driving lessons ? This one is ongoing as twin 2 has started but he works part time so he pays half and I am paying the other half as I go from the side hustle. We are still waiting to hear from DVLA about twin 1 so that could get expensive and need savings.

Plan and save for our next holiday x not yet but this goal was for 2025 and the car being paid will free up some savings focus

Maintain the side hustle to maximise the finances / This is ticking away for this academic year but is a PITA. It will need a little more direct focus for the academic year 2025/26

Renegotiate mortgage deal when my 2.19% deal ends on 28/2/24 / This one should have been in the previous section but now on 4.79% until 31/5/26. Hoping the rates may be lower then!

Build a car fund to either own my car or buy a newer car / Well on my way")

I feel quite proud of my work on my 2024 goals. I have rocked some but others make it obvious where I need to focus myself for 2025.

The twins prom set me back by around £1000. I was able to save and give the twins cash for their GCSE results.

I feel great that neither of those things caused me any issues but they did have an impact on possible mortgage overpayments!

I am dropping a child at a party soon so I think i will sign off for tonight and come back tomorrow ready to think about my 2025 goals and another monster post.

Total Debt May 21 £20,490.44 DEBT FREE DATE 29/7/22

Mortgage balance May 21 £177,096.19. Now £143,070.41

Mortgage free date. At start of sole mortgage = July 2042

2024 SAVINGS FOCUS - get rid of the car finance. £12,706.25 PAID OFF

2025 Savings Focus - 33.3/33.3/33.3 split; savings for house renovations (bathrooms/garden/kitchen; whichever collapses first), save for a family holiday (probably our last one!) and paydown/offset the mortgage. Total pot = £4238.564 -

I have set my new goals for 2025

Frustratingly enough, I now have enough to pay off my car but that would mean forgoing the interest on my account which matures on 9th February so I am going to make one last car payment then cash in my premium bonds after the February draw and get that loan gone.

I think that sort of means my 2025 goals only get to start in mid-February but it is what it is!

Total Debt May 21 £20,490.44 DEBT FREE DATE 29/7/22

Mortgage balance May 21 £177,096.19. Now £143,070.41

Mortgage free date. At start of sole mortgage = July 2042

2024 SAVINGS FOCUS - get rid of the car finance. £12,706.25 PAID OFF

2025 Savings Focus - 33.3/33.3/33.3 split; savings for house renovations (bathrooms/garden/kitchen; whichever collapses first), save for a family holiday (probably our last one!) and paydown/offset the mortgage. Total pot = £4238.564 -

A month between updates but what a month!

'Accidentally' used a big chunk of savings on a very lovely black lab puppy. She is exhausting, adorable and rather expensive but we are utterly in love.

Another no win on the premium bonds made it easier to cash them in this month. I have pooled all my savings accounts (and had to pinch a little from my side hustle due to the accidental puppy purchase) and have tonight sent a bank transfer to pay off my car.

That feels massive and amazing to have been able to do but now very nervous that I have done something wrong and sent a massive amount of money to the wrong place so eagerly awaiting confirmation that my account is settled.

My car had its service and MOT on Saturday so I now need to save to buy new brake disks and pads in the next 2000-3000 miles!

Total Debt May 21 £20,490.44 DEBT FREE DATE 29/7/22

Mortgage balance May 21 £177,096.19. Now £143,070.41

Mortgage free date. At start of sole mortgage = July 2042

2024 SAVINGS FOCUS - get rid of the car finance. £12,706.25 PAID OFF

2025 Savings Focus - 33.3/33.3/33.3 split; savings for house renovations (bathrooms/garden/kitchen; whichever collapses first), save for a family holiday (probably our last one!) and paydown/offset the mortgage. Total pot = £4238.563 -

Congrats on the puppy (and settling the car finance, obvs - but mostly the puppy!) 😀😀😀Mortgage start: £65,495 (March 2016)

Cleared 🧚♀️🧚♀️🧚♀️!!! In 5 years, 1 month and 29 days

Total amount repaid: £72,307.03. £1.10 repaid for every £1.00 borrowed

Finally earning interest instead of paying it!!!0 -

I love the thought of accidentally buying a puppy 🤣 Have fun and enjoy! Congrats on getting the car paid off 🙂I've been mortgage free once, so let's do it again!

Starting balance March 26 £191,274.531 -

I really want to accidentally buy a puppy

") DON'T BUY STUFF (from Frugalwoods)

DON'T BUY STUFF (from Frugalwoods)

No seriously, just don’t buy things. 99% of our success with our savings rate is attributed to the fact that we don’t buy things... You can and should take advantage of discounts.... But at the end of the day, the only way to truly save money is to not buy stuff. Money doesn’t walk out of your wallet on its own accord.

https://forums.moneysavingexpert.com/discussion/6289577/future-proofing-my-life-deposit-saving-then-mfw-journey-in-under-13-years#latest1 -

Congratulations on the Accidental puppy! I have to say labs are the absolute best, we've had 2, they are wonderfulTiredbutdetermined said:A month between updates but what a month!

'Accidentally' used a big chunk of savings on a very lovely black lab puppy. She is exhausting, adorable and rather expensive but we are utterly in love. Mortgage (Nov 20- NOV 39) originally £130,999 (Interest only) NOW £101,089(approx 78% equity)

Mortgage (Nov 20- NOV 39) originally £130,999 (Interest only) NOW £101,089(approx 78% equity)

Over payments 2020 £750/£750 (Mortgage payments only start Dec 2020)

Over payments 2021 £9,000 /£9,000 Over payments 2022 £7,629/£9,000 (£1,371 short of target)

Over payments 2023 £2,620/£9,000 (£6,380 short of target) Over payments 2024 £5,406/£11,000

Over payments 2025 £4,093/£5,600 (fix rate exp Dec 2025)

Loan £11298

Total Savings £5170

Premium Bonds - £1088

Xmas Regular Saver 2026 - £3000 -

Urgh, I have disappeared for a while again and have been plodding away but don't feel like I am getting anywhere positive fast!

I am saving into quite a lot of different pots at the moment so I don't think I get the same buzz of seeing my savings pot grow in the same way as I did when I was saving to pay off my car. I still put the £325 'car payment' into savings each month but it gets split 4 ways now.

The emergency fund has taken a battering and I used the last of it on a £500 car bill. My car also needs a new battery as we head into winter so the EF needs rebuilding just to be decimated again!

The twins are costing a fortune in driving lessons but I do make them contribute too. My son did have his test booked for the start of this month but he wasn't ready so that has been put off until September. I am pleased he hasn't had to fail (Yet!) but another 2+ months of driving lessons is a killer! Luckily his driving instructor was putting his prices up so we bought 2 x 10hr blocks before the prices went up. That might be enough to see him through to his test. My daughter is with a different company and I had to put her lessons on my credit card I am just plodding away at chipping that back down.

My side hustles are a bit slow at the moment. I am waiting for a nice big chunk from the GCSEs and the other hustle is slow over the summer but still ticking a little.

I need to update my signature as that might make me feel a little jollier!

Total Debt May 21 £20,490.44 DEBT FREE DATE 29/7/22

Mortgage balance May 21 £177,096.19. Now £143,070.41

Mortgage free date. At start of sole mortgage = July 2042

2024 SAVINGS FOCUS - get rid of the car finance. £12,706.25 PAID OFF

2025 Savings Focus - 33.3/33.3/33.3 split; savings for house renovations (bathrooms/garden/kitchen; whichever collapses first), save for a family holiday (probably our last one!) and paydown/offset the mortgage. Total pot = £4238.562

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards