We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

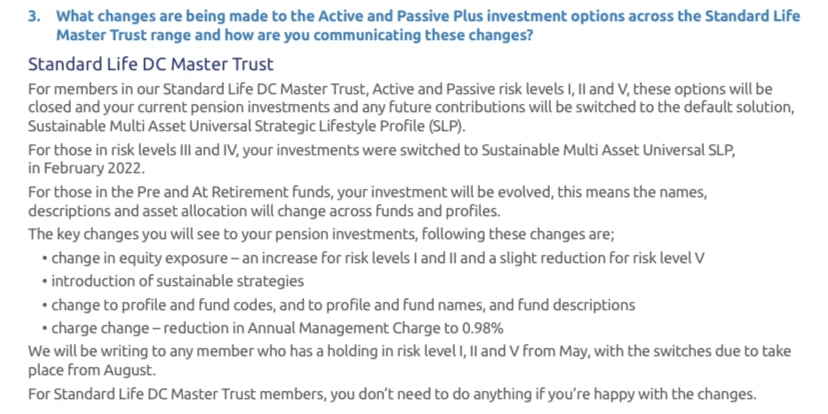

Standard Life Default Funds

Has anyone considered why Standard Life is moving towards greater exposure to equities when it appears recession risk is at its highest?

It feels options are being taken away.

https://lib.standardlife.com/library/uk/invp108.pdf

Comments

-

Has anyone considered why Standard Life is moving towards greater exposure to equities when it appears recession risk is at its highest?

The change seems to be one for the long term, so any current market issues are not really that relevant. In any case the stock markets look forward, so a possible recession/flat economy is already priced into the market. Often markets recover when a recession actually bites, as they are then looking forward to the recovery.

In reality no one knows what equities will do next week/month/year.

The changes may be because the Passive Plus funds have not been great performers ( too much UK% for one thing) and I did read somewhere that SL default funds were bottom of the league table of default funds

1 -

I’m not sure the default Standard Life pension fund options (which have their costs capped under statute for workplace pension schemes) once collated into one master default “sustainable” fund will continue to be appropriate for my risk appetite.It is worth noting that there are many different versions of SL workplace pensions. Largely depending on when taken out and employer decisions on what should be offered. The defaults on one plan may be different to the defaults on another.Has anyone considered why Standard Life is moving towards greater exposure to equities when it appears recession risk is at its highest?1 - Lower volatility gilts and bonds are going to be off the boil for a good number of years.

2 - equity performance does not align with economy status. i.e. markets have still gone up during periods of recession.

3 - Markets look ahead. They have already priced in what they think may happen.

4 - When paying in monthly, periods of loss are good news. Not bad.It feels options are being taken away.Why?

Have they said they are reducing their funds list?

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

All valid points, thank you both @Albermarle @dunstonh.It feels options are being taken away.Why?

Have they said they are reducing their funds list?

Yes, default funds “Active” funds I to V and “Passive” funds I to V (with various asset allocations i.e. equity only, high equity-low fixed income through to cash equivalents) are being consolidated into a single “Sustainable Master” fund allocating ~70% equity 15% fixed income 15% “other”.

Not the end of the world but, as far as I understand, the frustrating bit is that the cap on costs of 0.75% on workplace pension scheme default funds will then only apply to this Master fund if the asset allocation doesn’t reflect my long term strategy.

Maybe I’m mistaken? I’m having a hard time deciphering via their comms and website!0 -

Not the end of the world but, as far as I understand, the frustrating bit is that the cap on costs of 0.75% on workplace pension scheme default funds will then only apply to this Master fund if the asset allocation doesn’t reflect my long term strategy.Most SL workplace pensions I come across have the charge between 0.3% and 0.5% and all the internal funds are at the default lowest with only external fund houses coming in at higher cost. If your workplace pension is at 0.75% and has the smallest fund range then that suggests they have done little or no work with the provider or there are not enough employees to get a better version.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

I use SL - but just pick a small number of the lowest cost general global equity funds with some slightly dearer but still cheapish (after corporate discount) allocations to other assets - Gold, Property, China and (as I am well in my late 50s) a stabilising (but flat performing) chunk in a cash type fund. I know this is pretty much what the standard funds do but its working for me and I prefer the option to tinker, although I try not toI think I saw you in an ice cream parlour

Drinking milk shakes, cold and long

Smiling and waving and looking so fine1 -

Couldn’t agree moreMost SL workplace pensions I come across have the charge between 0.3% and 0.5% and all the internal funds are at the default lowest with only external fund houses coming in at higher cost. If your workplace pension is at 0.75% and has the smallest fund range then that suggests they have done little or no work with the provider or there are not enough employees to get a better version.")

It’s worth noting that most pension providers seem not to offer a lower rate on their default funds but give workplace pension scheme members a discount to reduce the overall rate (same effect).

What that discount is seems to be up for grabs but must always be 0.75% or below (unless the Government get their way and blow it out the water to support private equity as part of a national strategy).

0 -

This is pretty much identical to my primary work pension (SL too).mark55man said:I use SL - but just pick a small number of the lowest cost general global equity funds with some slightly dearer but still cheapish (after corporate discount) allocations to other assets - Gold, Property, China and (as I am well in my late 50s) a stabilising (but flat performing) chunk in a cash type fund. I know this is pretty much what the standard funds do but its working for me and I prefer the option to tinker, although I try not to

I have tinkered with it a fair bit but think I've now reached a happy medium using 3 Vanguard passive funds each with a reasonable charge of 0.18% and a SL property fund that's around 0.22% (after scheme discount). There are active global equity funds offered by BG and BNY Mellon which I've used in the past and with the employer discount more palatable but right now I cant justify 0.65% or higher for the active funds when the Vanguard passives have outperformed the actives during the last few years and most timeframes upto 5+ years.

I used a SL works pension many years back at a previous employer, the fund selection wasn't great and scheme discount was not that generous so it's pot luck what your employer has negotiated with SL!1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.5K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards