We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Working while drawing DB pension

Pat38493

Posts: 3,533 Forumite

Hi,

Am I right in thinking that if someone is in receipt of a DB pension income, they can take another job on up to 40K a year, and contribute up to 100% of their salary to a DC pension?

The lower limit wouldn't apply because they aren't drawing any flexible benefits?

They could then get 25% back out tax free, even in the same year if they wanted?

So for example if they had a DB pension £35K.

New job £40K salary 100% paid into DC scheme.

Draw out 10K tax free.

Now you earned 45K in the year but for tax purposes you only earned £35K, plus you have £30K left in your DC pot (crytalised), but you could carry on doing that in following years because you have not drawn any non tax free money out?

What am I missing or is this allowed?

Am I right in thinking that if someone is in receipt of a DB pension income, they can take another job on up to 40K a year, and contribute up to 100% of their salary to a DC pension?

The lower limit wouldn't apply because they aren't drawing any flexible benefits?

They could then get 25% back out tax free, even in the same year if they wanted?

So for example if they had a DB pension £35K.

New job £40K salary 100% paid into DC scheme.

Draw out 10K tax free.

Now you earned 45K in the year but for tax purposes you only earned £35K, plus you have £30K left in your DC pot (crytalised), but you could carry on doing that in following years because you have not drawn any non tax free money out?

What am I missing or is this allowed?

0

Comments

-

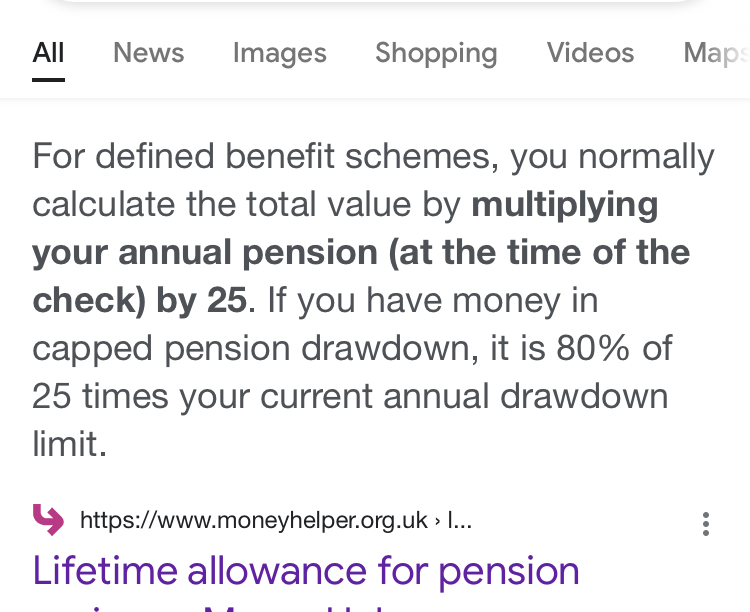

They will have used £875000 of the £1073100 Lifetime Allowance (£35k x 25). So not huge amounts left especially if that have any other DC pension.0

-

I think for LTA purposes a DB pension is multiplied by 20, not 25

1 -

Isn't it 20x the DB pension (plus any PCLS)?0

-

Its 20 I just read the first extract on Google which on further investigation is for pre 2006 pension

0

0 -

Hi

This is similar to my circumstances which I've been doing for five years or so, so yes - you can do this. In practice I contribute enough to keep below the HR tax limit.

Though I have to say that if it wasn't for the 'generosity' of the LTA in relation to DB pensions I'd have been completely screwed.2 -

I guess, but it seems to me that you could save up to 2K in tax annually by doing this, but yes if you already close to the LTA it would be an issue. Plus further potential tax savings in future years when you stop working. Plus avoidance of NI if you can use Salary Sacrifice.jimi_man said:Hi

This is similar to my circumstances which I've been doing for five years or so, so yes - you can do this. In practice I contribute enough to keep below the HR tax limit.

Though I have to say that if it wasn't for the 'generosity' of the LTA in relation to DB pensions I'd have been completely screwed.

How did you find that from a practicality point of view - I don't know if most pension providers would typically allow you to draw out your tax free cash in small chunks like a salary without you ending up paying huge charges?0 -

I should add that I don't actually draw the pension out, at least I haven't yet. I'm just using it as a tax efficient savings vehicle that's all. It's to cover the bit from when we finish working until SPA. (57-67)

However if you just drew it out once a year then I wouldn't have thought the charges would be too onerous?

I did Salary Sacrifice for a while when I was contracting, and whilst it does save NI, you can't go below Minimum Living Wage (the DB pension income doesn't count in that figure) so you wouldn't be able to contribute the full amount into the pension.0 -

You need to look at the charges for your particular pension provider - they vary.Pat38493 said:

I guess, but it seems to me that you could save up to 2K in tax annually by doing this, but yes if you already close to the LTA it would be an issue. Plus further potential tax savings in future years when you stop working. Plus avoidance of NI if you can use Salary Sacrifice.jimi_man said:Hi

This is similar to my circumstances which I've been doing for five years or so, so yes - you can do this. In practice I contribute enough to keep below the HR tax limit.

Though I have to say that if it wasn't for the 'generosity' of the LTA in relation to DB pensions I'd have been completely screwed.

How did you find that from a practicality point of view - I don't know if most pension providers would typically allow you to draw out your tax free cash in small chunks like a salary without you ending up paying huge charges?

Do you need to draw out multiple chunks in the year? If you do that, AFAIA, each one is a crystallisation event which has to recalc the remaining LTA % so more admin for them. Crystallising one bigger chunk per year and taking the 25% tax free portion would probably be simpler (and maybe incur less fees?).I’m a Senior Forum Ambassador and I support the Forum Team on the Pensions, Annuities & Retirement Planning, Loans

& Credit Cards boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com.

All views are my own and not the official line of MoneySavingExpert.0 -

I think the higher price SIPP providers, like HL & Fidelity plus the traditional providers like Aviva, Standard Life etc normally do not have any extra charges for taking the TFLS in stages.

The lower cost providers usually have some kind of charge for each withdrawal. ( so may end up higher cost in the end)

OP - The £40K annual allowance includes employer contributions and tax relief .

Also do not forget that the DB pension will be taxed.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards