We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

SIPP contributions when drawing from a DB pension

Comments

-

For each year of NI contributions, you currently get an extra £5.29 per week. That of course will go up with inflation each, so it should get a good boost next year.happybagger said:

Is there a formula for this sort of thing? ie how much each of the latter years adds?Dazed_and_C0nfused said:True.

Remember the 3rd year only adds £0.98/week.

Probably still worth it but not as good value as the first two!

I'm showing as 82.3% of the maximum, with 27 of 35 years complete (although last year not yet accounted for).

The 35 years is only relevant for those who started contributing since 2016. If your current estimate is £152.38 (82.3% of the maximum) it looks like you might get to the maximum with another 7 years of NI contributions.2 -

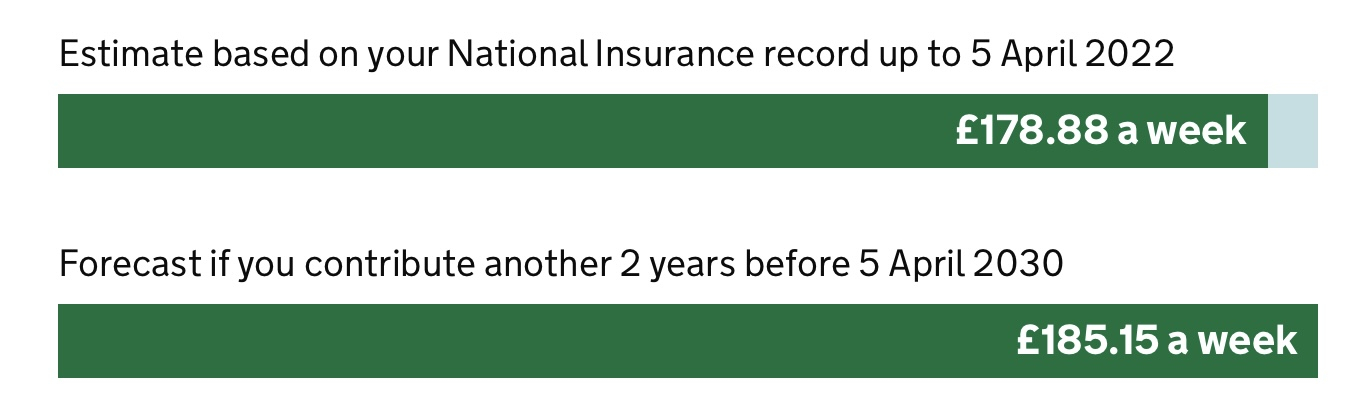

Though when adding a year you cannot go over the state pension amount of £185.15. So currently the value of the last contribution to bring it up to the maximum could be worth between £0.01 and £5.29.Audaxer said:

For each year of NI contributions, you currently get an extra £5.29 per week. That of course will go up with inflation each, so it should get a good boost next year.happybagger said:

Is there a formula for this sort of thing? ie how much each of the latter years adds?Dazed_and_C0nfused said:True.

Remember the 3rd year only adds £0.98/week.

Probably still worth it but not as good value as the first two!

I'm showing as 82.3% of the maximum, with 27 of 35 years complete (although last year not yet accounted for).

The 35 years is only relevant for those who started contributing since 2016. If your current estimate is £152.38 (82.3% of the maximum) it looks like you might get to the maximum with another 7 years of NI contributions.2 -

Yes, I would say your last year is also well worth paying.IanManc said:

Thank you for this @Audaxer and @Notepad_Phil ! My forecast says I need two more years, and I'm paying voluntary Class 3 contributions. I now know that this year's contributions will add £5.29 to my pension - so I'll get the contributions back by the time I'm 70 at current values; while the next financial year's contributions will add £2.68 to my pension - so I'll get my contributions back just before I'm 73. On balance I reckon that the last year is still worth paying in, buy I'm open to other opinions!Audaxer said:

For each year of NI contributions, you currently get an extra £5.29 per week. That of course will go up with inflation each, so it should get a good boost next year.happybagger said:

Is there a formula for this sort of thing? ie how much each of the latter years adds?Dazed_and_C0nfused said:True.

Remember the 3rd year only adds £0.98/week.

Probably still worth it but not as good value as the first two!

I'm showing as 82.3% of the maximum, with 27 of 35 years complete (although last year not yet accounted for).

The 35 years is only relevant for those who started contributing since 2016. If your current estimate is £152.38 (82.3% of the maximum) it looks like you might get to the maximum with another 7 years of NI contributions.1 -

The ability to buy the £5.29 a week index linked for life for about £850 is such a fantastic deal, that even if you only get half of it for the last year, it is still a great deal.IanManc said:

Thank you for this @Audaxer and @Notepad_Phil ! My forecast says I need two more years, and I'm paying voluntary Class 3 contributions. I now know that this year's contributions will add £5.29 to my pension - so I'll get the contributions back by the time I'm 70 at current values; while the next financial year's contributions will add £2.68 to my pension - so I'll get my contributions back just before I'm 73. On balance I reckon that the last year is still worth paying in, buy I'm open to other opinions!Audaxer said:

For each year of NI contributions, you currently get an extra £5.29 per week. That of course will go up with inflation each, so it should get a good boost next year.happybagger said:

Is there a formula for this sort of thing? ie how much each of the latter years adds?Dazed_and_C0nfused said:True.

Remember the 3rd year only adds £0.98/week.

Probably still worth it but not as good value as the first two!

I'm showing as 82.3% of the maximum, with 27 of 35 years complete (although last year not yet accounted for).

The 35 years is only relevant for those who started contributing since 2016. If your current estimate is £152.38 (82.3% of the maximum) it looks like you might get to the maximum with another 7 years of NI contributions.1 -

Ok. Actually I started contributing in 1988. There are gaps in my record thoughAudaxer said:

For each year of NI contributions, you currently get an extra £5.29 per week. That of course will go up with inflation each, so it should get a good boost next year.happybagger said:

Is there a formula for this sort of thing? ie how much each of the latter years adds?Dazed_and_C0nfused said:True.

Remember the 3rd year only adds £0.98/week.

Probably still worth it but not as good value as the first two!

I'm showing as 82.3% of the maximum, with 27 of 35 years complete (although last year not yet accounted for).

The 35 years is only relevant for those who started contributing since 2016. If your current estimate is £152.38 (82.3% of the maximum) it looks like you might get to the maximum with another 7 years of NI contributions.You have:

- 27 years of full contributions

- 16 years to contribute before 5 April 2037

- 8 years when you did not contribute enough

0 -

My forecast is more than £185.15 a week.Notepad_Phil said:

Though when adding a year you cannot go over the state pension amount of £185.15. So currently the value of the last contribution to bring it up to the maximum could be worth between £0.01 and £5.29.Audaxer said:

For each year of NI contributions, you currently get an extra £5.29 per week. That of course will go up with inflation each, so it should get a good boost next year.happybagger said:

Is there a formula for this sort of thing? ie how much each of the latter years adds?Dazed_and_C0nfused said:True.

Remember the 3rd year only adds £0.98/week.

Probably still worth it but not as good value as the first two!

I'm showing as 82.3% of the maximum, with 27 of 35 years complete (although last year not yet accounted for).

The 35 years is only relevant for those who started contributing since 2016. If your current estimate is £152.38 (82.3% of the maximum) it looks like you might get to the maximum with another 7 years of NI contributions.

Your forecast is £209.17 a week,£909.52 a month, £10,914.19 a year

Your forecast

- is not a guarantee and is based on the current law

- is based on your National Insurance record up to 5 April 2021

- does not include any increase due to inflation

£209.17 is the most you can get

You cannot improve your forecast any more.

0 -

My forecast is more than £185.15 a week.

This is because at introduction of the NSP (6/4/16), your "starting (foundation) amount" was higher than £155.65 ( the full new state pension).

See

Under the Government proposals, if your foundation amount is higher than the full level of the single-tier pension you will get the extra amount as a separate protected payment. This will be paid on top of the full single-tier pension.

Thus any contributions or credits after 6/4/16 will not have increased your state pension.

However, your "foundation amount" will have been revaluing since then, the amount equalling the full NSP under the triple (double for the current year) lock and the balance (the protected payment) by CPI.

2 -

Not just a bargain, but an absolute steal. To buy a £270 pa pension , index linked/triple locked at 66, would cost about £7,000.happybagger said:

Ok. Actually I started contributing in 1988. There are gaps in my record thoughAudaxer said:

For each year of NI contributions, you currently get an extra £5.29 per week. That of course will go up with inflation each, so it should get a good boost next year.happybagger said:

Is there a formula for this sort of thing? ie how much each of the latter years adds?Dazed_and_C0nfused said:True.

Remember the 3rd year only adds £0.98/week.

Probably still worth it but not as good value as the first two!

I'm showing as 82.3% of the maximum, with 27 of 35 years complete (although last year not yet accounted for).

The 35 years is only relevant for those who started contributing since 2016. If your current estimate is £152.38 (82.3% of the maximum) it looks like you might get to the maximum with another 7 years of NI contributions.You have:

- 27 years of full contributions

- 16 years to contribute before 5 April 2037

- 8 years when you did not contribute enough

2 -

The State Pension forecast is quite “twitchy”. My estimate (£173.59 with 3 more years required which I shared above) has changed over the last few weeks and now shows

The shortfall is now only £6.27 a week (not £11.56) with only 2 more years (not 3) required. I only worked 6 weeks in last year!0

The shortfall is now only £6.27 a week (not £11.56) with only 2 more years (not 3) required. I only worked 6 weeks in last year!0 -

By twitchy you mean it's now been updated to reflect the latest complete year (to 5 April 2022).n3ophyte said:The State Pension forecast is quite “twitchy”. My estimate (£173.59 with 3 more years required which I shared above) has changed over the last few weeks and now showsThe shortfall is now only £6.27 a week (not £11.56) with only 2 more years (not 3) required. I only worked 6 weeks in last year!

What you worked doesn't come into it, it's what was reported by your employer (or any NI credits, voluntary payments) that counts.

It could be your 6 weeks work was reported as two or even three monthly payments which could be beneficial under the LEL rules.

https://www.litrg.org.uk/tax-guides/students/going-abroad/national-insurance

NB. Ignore the fact that that is aimed at people leaving the UK, the principle is correct.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards