We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Virgin Money Mortgage timelines are crazy

col81

Posts: 338 Forumite

Applied 4 weeks ago approved in principal for a second homeowner mortgage no issues. With underwriters still not heard anything chased 3 times just keep getting told it is in a queue? is this normal? i have £0 debt and 999 experian credit score. House worth £210k need £125k mortgage

0

Comments

-

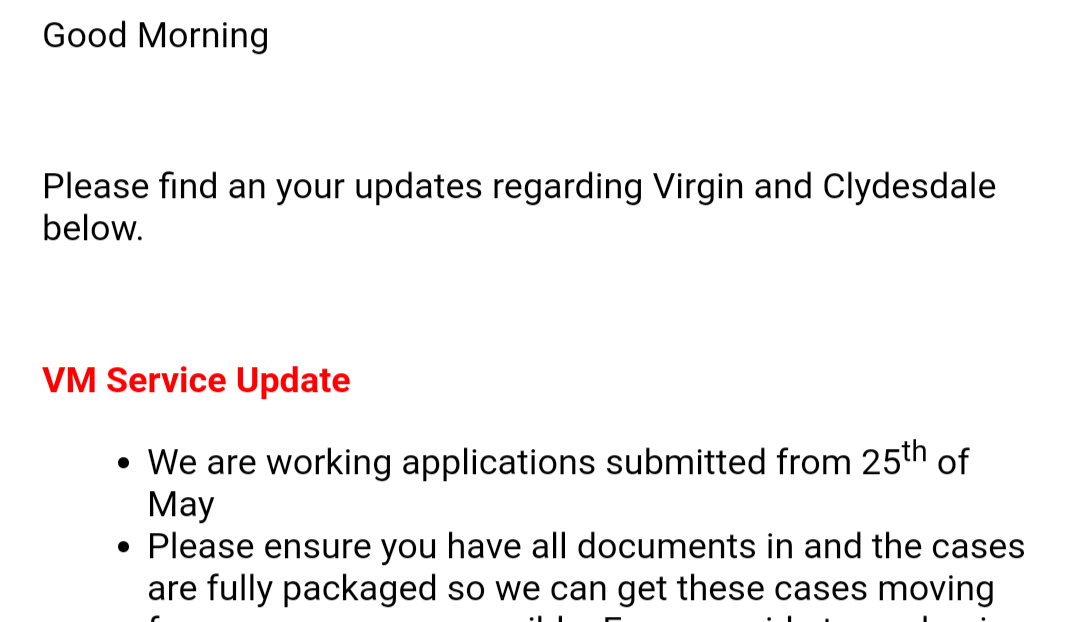

@col81 Virgin-Clydesdale are quite slow at present, the only mainstream lender that is slower right now is Nationwide.

With respect to intermediary applications, this is from my Virgin BDM this morning -

If your app went in well before then, might be worth chasing your broker for an update.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

We're at 8 weeks with Kensington via Trussle, still no yay or ney. Just lots of unreturned calls, same docs being requested multiple time, vague promises of deadlines that are never met. First-time buyers so we're not sure how far from the norm this is. But I feel your frustration, just a shame these companies don't have any empathy toward their customers, you feel you're like cattle to them.0

-

If you applied 4 weeks ago you should have heard back by now.

Although plenty of lenders are taking 10-15 working days to assess documents at the moment. Off the top of my head:

Natwest,

Nationwide,

TML,

Virgin.

I am a Mortgage AdviserYou should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.1 -

Thank you! The broker has said all information submitted is fine and virgin will contact me regarding a valuation. Does this mean I will get a offer? How do they value the property? I told them it's worth £190k but next door is going through a sales process and it went for £216k (it's going through)

0 -

col81 said:Thank you! The broker has said all information submitted is fine and virgin will contact me regarding a valuation. Does this mean I will get a offer? How do they value the property? I told them it's worth £190k but next door is going through a sales process and it went for £216k (it's going through)

The value for the lender will be the lower of what you told them (190k) and what the valuer thinks it is. So the maximum they will come back with is 190k.

0 -

What if they said it's worth £170k do I pay a higher rate because of ltv? Seems a grey area. Also I presume if valuation ok I'm sorted?0

-

If you are close to an LTV band and fall into the next one with a 20k down-valuation then yes you may have to pay a higher rate. But tbh the difference in rates between 60-85% LTV is minimal anyways. The only issue is whether the bank will allow you to pick a rate that was available when you applied or one that is available now (which will be higher).The valuation is separate to the underwriting.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.9K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.4K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards