We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

NSandi complaint

Merryb

Posts: 16 Forumite

Hi

I have had some money in a NSANDI saver that matured last December. I haven't been able to deal with it until now and I assumed that they would keep it in some sort of easy access low interest account. However they now tell me that they have transferred it to a 0.1% account and I cannot take it out for a year.

Surely this is very unethical?

Furthermore the person on the phone was very rude and when I asked to speak to someone about this he said someone could get back to me - he didn't know when, but said 'when they aren't busy'. Really not the attitude I would expect, especially from someone that is holding my money - of perhaps that is why?

Can anyone give me any advice on this? Obviously I want to move it to somewhere where it will at least have a hope against inflation...

0

Comments

-

Unfortunately I think it’s in the TandC’s that if you don’t make contact and give instructions- this is the action they will take

i think your stuck with this now

2 -

I assumed that they would keep it in some sort of easy access low interest account.

Some savings providers do that but many just put you back into the same product you had before, if they get no instructions from you . So that bit is not unusual . However if it is a fixed rate account and it only pays 0.1%, then that is pretty bad.

0 -

What did the maturity letter say they'd do if they didn't hear from you?Merryb said:I have had some money in a NSANDI saver that matured last December. I haven't been able to deal with it until now and I assumed that they would keep it in some sort of easy access low interest account.2 -

They just emailed me to say I could get the statement online, however when I go online it says it isn't a paperless account and there are no document there, so there seems to be a hiccup there.Looking at their site,they don't do that type of account anymore but I don't know since when - it does seem strange that they were even able to transfer to that type of account if it was no longer available. however for those accounts already running they do say 'once you have decided to renew you won't have access', but my point is that I didn't decide and they seem to have chosen the smallest return for me. It all seems very low behaviour to me.0

-

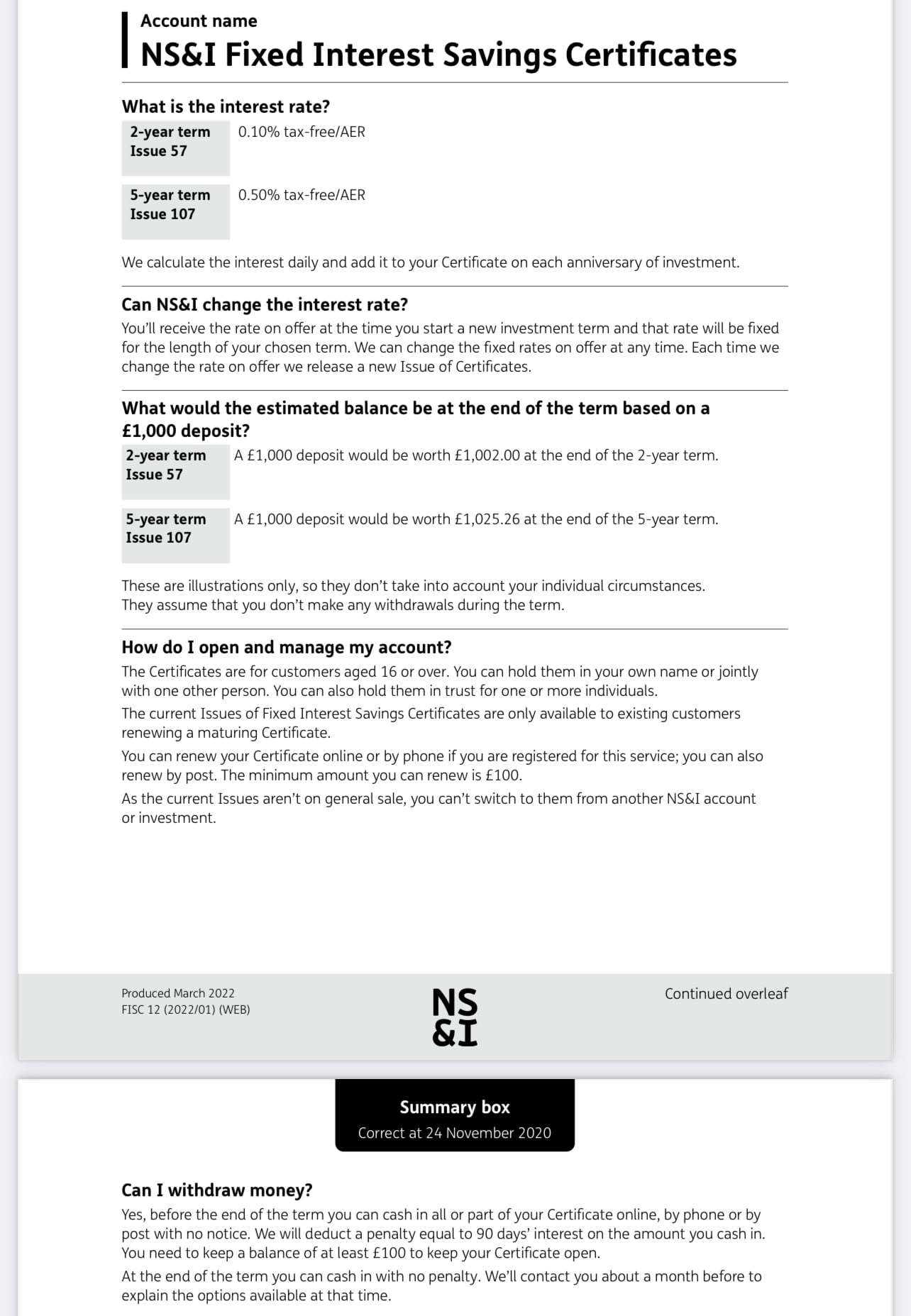

https://www.nsandi.com/files/asset/pdf/fixed-interest-savings-certificates-key-features.pdf explains the terms associated with Fixed Interest Savings Certificates, so if this is the product you have then the maturity options are clearly defined:What happens at maturity?However, the good news is this section:

We’ll contact you to let you know your options at least 30 days before your Certificate matures. Your options on maturity will normally be to:

• reinvest in a new Certificate of the same term (which will normally happen automatically if you don’t give us different instructions)

• reinvest in a new Certificate of a different term

• cash in your Certificate to get your money back, together with interest.Cashing in earlyObviously with a derisory and uncompetitive rate of 0.1%, that's no penalty at all really....

Certificates are designed to be held for the full term. You can cash in (including switching to another NS&I account) early but there is a cost.

If you cash in only part of the Certificate you must leave a balance of at least £100.

When you ask us to cash in (online, by phone, by post) we will treat this as you giving us your consent to make the payment. You can’t stop or change the payment once you have given your instructions (unless we agree to this).

The cost of cashing in early

We’ll deduct from the payment a penalty equal to 90 days’ interest on the amount you cash in.0 -

It is very unusual for NS&I not to notify you well in time before maturity of the options you have. There is also extensive general maturity information online.

What was your account called before it matured, and what is it called now? Can you cash it in early, with a loss of interest?0 -

You've assumed and not bother to read any communications sent. Hardly grounds for complaint.3

-

I am guessing this is the 1 year Guaranteed Growth Bond at 0.10%If so you can't have early access

- Previously, we gave you access to your investment before the end of its term but charged a penalty equal to 90 days’ interest on any money you took out early. Now, once you’ve decided to renew a Bond, you won’t have access to your money until the Bond reaches the end of its new term

See the Summary Box0 -

It could be, but it could also be ine of these

May be the OP comes back and tells us which it is0

May be the OP comes back and tells us which it is0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards