We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Leaseholder Buildings Insurance

henrygregory

Posts: 567 Forumite

Hi, I own a shared ownership property. When I purchased the property, I was told that I need contents only insurance, which I duly took out (with all the extras including accidental damage) and have renewed in the 3 years I have lived here. The property is a newbuild and is now 3 years old.

The HA who owns the remaining share charges me a service charge. A portion of this service charge covers the buildings insurance. At no point did the HA provide me with documentation for this insurance, so I had no clue what was actually covered. I wrote to them asking for full details of what was covered once I had settled in, in 2020 and I have this on file.

A month ago, I returned home to find that one of the pieces of glass in my front door was shattered. The door faces out into the street and I have a video doorbell. I checked it and could not see any evidence that someone had smashed the glass or damaged the door. It is a double glazed pane and it is shattered on the inside half of the glass not the outside facing half.

1.I contacted the house builder assuming the glass would be under warranty. No, only for the first two years

2.I contacted a local glazier to ascertain roughly how much it might cost to get the glass replaced.

3. In the interim, I contacted the insurance broker for the buildings insurance to see if there would be any excess payable to help me decide what the best way forwards would be. The documentation I requested in 2020 seemed to suggest that excesses were only payable for subsidence but I wanted to make sure.

4.The insurer got back to me and asked me to explain what had happened - they had several details completely incorrect from my initially enquiry, I put them right and re-explained exactly what the situation was. I had to repeatedly chase them for almost 3 weeks.

They have just got back to me stating:

I would be grateful of any thoughts on this as how can I identify an event? I feel like they are saying the damage is maybe wear and tear?

If I come home and my window is broken, what do they want me to do to identify this? Moving forwards, this worries me as if someone were to damage my property, how am I supposed to be able to identify that this is a one off, identifiable event? For all I know, someone may have tried to kick the door and the glass shattered. The doorbells are not 100% and have missed things in the past at night.

I have never ever made a claim before. My contents insurance won't cover this as the glass is part of the building. To protect myself against this in the future, surely I couldn't get building and contents insurance moving forward as I would have a dual policy on the buildings component which would be against the rules. How am I supposed to have myself fully covered moving forwards?

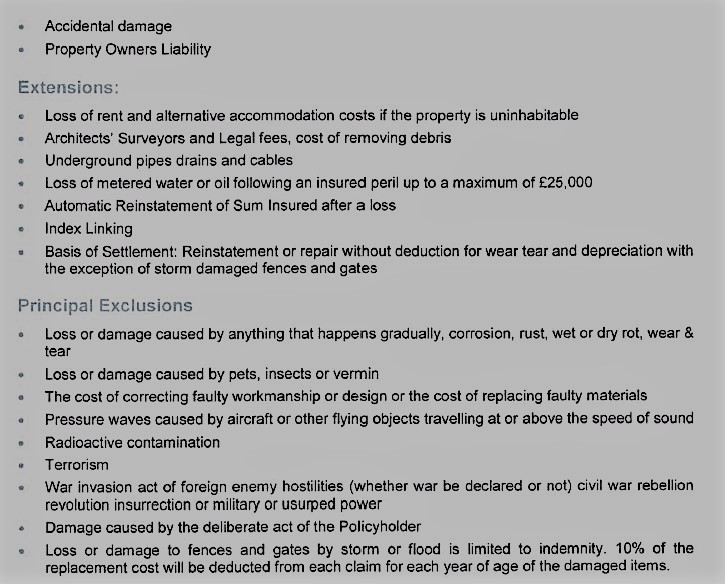

Here is a breakdown of what is apparently covered...

The HA who owns the remaining share charges me a service charge. A portion of this service charge covers the buildings insurance. At no point did the HA provide me with documentation for this insurance, so I had no clue what was actually covered. I wrote to them asking for full details of what was covered once I had settled in, in 2020 and I have this on file.

A month ago, I returned home to find that one of the pieces of glass in my front door was shattered. The door faces out into the street and I have a video doorbell. I checked it and could not see any evidence that someone had smashed the glass or damaged the door. It is a double glazed pane and it is shattered on the inside half of the glass not the outside facing half.

1.I contacted the house builder assuming the glass would be under warranty. No, only for the first two years

2.I contacted a local glazier to ascertain roughly how much it might cost to get the glass replaced.

3. In the interim, I contacted the insurance broker for the buildings insurance to see if there would be any excess payable to help me decide what the best way forwards would be. The documentation I requested in 2020 seemed to suggest that excesses were only payable for subsidence but I wanted to make sure.

4.The insurer got back to me and asked me to explain what had happened - they had several details completely incorrect from my initially enquiry, I put them right and re-explained exactly what the situation was. I had to repeatedly chase them for almost 3 weeks.

They have just got back to me stating:

There is zero excess.

We've had a look at your recent correspondence and from what you’ve said there doesn’t seem to be a one off event which has occurred to cause the window to break. Because of this the policy wouldn’t cover the glass that has shattered. There needs to be a one off, identifiable event which doesn’t seem to be the case.

Fine, would have been good if they could have told me that three weeks ago. Glazier has said it should be under £200 and they are coming next week to take a look and give me an accurate cost, all depends if the glass can be removed from a UPVC door.We've had a look at your recent correspondence and from what you’ve said there doesn’t seem to be a one off event which has occurred to cause the window to break. Because of this the policy wouldn’t cover the glass that has shattered. There needs to be a one off, identifiable event which doesn’t seem to be the case.

I would be grateful of any thoughts on this as how can I identify an event? I feel like they are saying the damage is maybe wear and tear?

If I come home and my window is broken, what do they want me to do to identify this? Moving forwards, this worries me as if someone were to damage my property, how am I supposed to be able to identify that this is a one off, identifiable event? For all I know, someone may have tried to kick the door and the glass shattered. The doorbells are not 100% and have missed things in the past at night.

I have never ever made a claim before. My contents insurance won't cover this as the glass is part of the building. To protect myself against this in the future, surely I couldn't get building and contents insurance moving forward as I would have a dual policy on the buildings component which would be against the rules. How am I supposed to have myself fully covered moving forwards?

Here is a breakdown of what is apparently covered...

0

Comments

-

You have an insured perils policy and as such its your duty to prove the damage was caused by one of the listed perils (fire, storm, malicious damage etc)

The fact that you attempted to make a warranty claim points to the fact you believe it may be a manufacturing fault which isn't one of the insured perils (and indeed is often an explicitly excluded risk)

The insurers will take your explanation of what's happened and the damage and decide if on the balance of probability it was caused by an insured peril, the fact the outside glass is intact and the inside glass is the one that broke whilst the property was vacant doesn't point at any external actors being involved for it to be malicious damage or attempted theft, you've not described there being anything inside that could have hit the glass whilst the property is unoccupied for it to be accidental damage and so by a process of elimination it seems most likely a manufacturing/design defect as you first thought and hence not covered.0 -

Thanks, didn't know what was the name of it.Sandtree said:You have an insured perils policy and as such its your duty to prove the damage was caused by one of the listed perils (fire, storm, malicious damage etc)

The fact that you attempted to make a warranty claim points to the fact you believe it may be a manufacturing fault which isn't one of the insured perils (and indeed is often an explicitly excluded risk)

The insurers will take your explanation of what's happened and the damage and decide if on the balance of probability it was caused by an insured peril, the fact the outside glass is intact and the inside glass is the one that broke whilst the property was vacant doesn't point at any external actors being involved for it to be malicious damage or attempted theft, you've not described there being anything inside that could have hit the glass whilst the property is unoccupied for it to be accidental damage and so by a process of elimination it seems most likely a manufacturing/design defect as you first thought and hence not covered.

As far as I can see, it is not something I have done to the glass.

If in the future, I return home and find a full pane to be broken, or the side of the double glazing facing out, what would I do then as you would assume in that instance it could be attempted theft or malicious. Would they cover that? Just want to make sure that I am as covered as I can be.0 -

They will make a determination by what you say and what evidence there is... if you say you've come home the windows smashed in and there is a brick sat on your carpet they'll assume its malicious damage... they may decide to inspect (probably not for this value) and obv if they see all the broken glass is outside the property and not inside then that will look like a staged claim.henrygregory said:

Thanks, didn't know what was the name of it.Sandtree said:You have an insured perils policy and as such its your duty to prove the damage was caused by one of the listed perils (fire, storm, malicious damage etc)

The fact that you attempted to make a warranty claim points to the fact you believe it may be a manufacturing fault which isn't one of the insured perils (and indeed is often an explicitly excluded risk)

The insurers will take your explanation of what's happened and the damage and decide if on the balance of probability it was caused by an insured peril, the fact the outside glass is intact and the inside glass is the one that broke whilst the property was vacant doesn't point at any external actors being involved for it to be malicious damage or attempted theft, you've not described there being anything inside that could have hit the glass whilst the property is unoccupied for it to be accidental damage and so by a process of elimination it seems most likely a manufacturing/design defect as you first thought and hence not covered.

As far as I can see, it is not something I have done to the glass.

If in the future, I return home and find a full pane to be broken, or the side of the double glazing facing out, what would I do then as you would assume in that instance it could be attempted theft or malicious. Would they cover that? Just want to make sure that I am as covered as I can be.

Its only when there is no explanation for the damage that you get into a more difficult situation and especially on an insured perils policy... and all risks policy is less problematic as it moves the burden from you to prove what did happen to the insurer proving it was one of the named exclusions. All risk policies are typically notably more expensive as a result.1 -

Thank you, that makes perfect sense.Sandtree said:

They will make a determination by what you say and what evidence there is... if you say you've come home the windows smashed in and there is a brick sat on your carpet they'll assume its malicious damage... they may decide to inspect (probably not for this value) and obv if they see all the broken glass is outside the property and not inside then that will look like a staged claim.henrygregory said:

Thanks, didn't know what was the name of it.Sandtree said:You have an insured perils policy and as such its your duty to prove the damage was caused by one of the listed perils (fire, storm, malicious damage etc)

The fact that you attempted to make a warranty claim points to the fact you believe it may be a manufacturing fault which isn't one of the insured perils (and indeed is often an explicitly excluded risk)

The insurers will take your explanation of what's happened and the damage and decide if on the balance of probability it was caused by an insured peril, the fact the outside glass is intact and the inside glass is the one that broke whilst the property was vacant doesn't point at any external actors being involved for it to be malicious damage or attempted theft, you've not described there being anything inside that could have hit the glass whilst the property is unoccupied for it to be accidental damage and so by a process of elimination it seems most likely a manufacturing/design defect as you first thought and hence not covered.

As far as I can see, it is not something I have done to the glass.

If in the future, I return home and find a full pane to be broken, or the side of the double glazing facing out, what would I do then as you would assume in that instance it could be attempted theft or malicious. Would they cover that? Just want to make sure that I am as covered as I can be.

Its only when there is no explanation for the damage that you get into a more difficult situation and especially on an insured perils policy... and all risks policy is less problematic as it moves the burden from you to prove what did happen to the insurer proving it was one of the named exclusions. All risk policies are typically notably more expensive as a result.

Money is not really the issue luckily for me so a more expensive policy is not an issue - I have a very good contents only policy - top of the rankings currently.

But I am assuming, as the property buildings insurance has to be done by my housing association, there is no way for me to upgrade or do my own as I have it in my mind that you can't be double insured for something, like on a car - you can only have one insurance policy running at one time. Is that correct? I would much rather pay more and know that in the event of something happening, you won't have any hassle. I was already not one bit impressed at a 3 week response time to be told there is no excess and no, doesn't seem you are covered - surely something that could have been explained a little faster.

0 -

There is nothing illegal or technically to stop you having multiple policies running, its common in relation to commercial insurance as no single insurer wants to cover the whole Shard for example. In practice however mass market consumer insurance isn't designed for this and having two insurers will add delays as they check each others terms and see if either have slipped up and forgotten to include a "no other insurance" clause etc.

Your main issue however would be proving you have an insurable interest in the property given your lease states its the HA's responsibility to buy the insurance. Without this your policy wouldn't respond in the event of a claim... in practice the insurer may not realise its leasehold or think to check but you could be paying for nothing.

Its likely there is a single policy covering the full development which moves it into commercial/business insurance space which is often much more nuanced (rather than standard terms for everyone) and works at a different pace... large companies are much more comfortable paying out to fix urgent issues knowing they'll be reimbursed in due time whereas consumers often want the insurer to provide the suppliers and pay them up front etc hence have more automated systems, quicker response times etc.1 -

Your lease may well say something about whether you're prohibited from duplicating insurance.henrygregory said:

But I am assuming, as the property buildings insurance has to be done by my housing association, there is no way for me to upgrade or do my own as I have it in my mind that you can't be double insured for something, like on a car - you can only have one insurance policy running at one time. Is that correct? I would much rather pay more and know that in the event of something happening, you won't have any hassle.Sandtree said:

They will make a determination by what you say and what evidence there is... if you say you've come home the windows smashed in and there is a brick sat on your carpet they'll assume its malicious damage... they may decide to inspect (probably not for this value) and obv if they see all the broken glass is outside the property and not inside then that will look like a staged claim.henrygregory said:

Thanks, didn't know what was the name of it.Sandtree said:You have an insured perils policy and as such its your duty to prove the damage was caused by one of the listed perils (fire, storm, malicious damage etc)

The fact that you attempted to make a warranty claim points to the fact you believe it may be a manufacturing fault which isn't one of the insured perils (and indeed is often an explicitly excluded risk)

The insurers will take your explanation of what's happened and the damage and decide if on the balance of probability it was caused by an insured peril, the fact the outside glass is intact and the inside glass is the one that broke whilst the property was vacant doesn't point at any external actors being involved for it to be malicious damage or attempted theft, you've not described there being anything inside that could have hit the glass whilst the property is unoccupied for it to be accidental damage and so by a process of elimination it seems most likely a manufacturing/design defect as you first thought and hence not covered.

As far as I can see, it is not something I have done to the glass.

If in the future, I return home and find a full pane to be broken, or the side of the double glazing facing out, what would I do then as you would assume in that instance it could be attempted theft or malicious. Would they cover that? Just want to make sure that I am as covered as I can be.

Its only when there is no explanation for the damage that you get into a more difficult situation and especially on an insured perils policy... and all risks policy is less problematic as it moves the burden from you to prove what did happen to the insurer proving it was one of the named exclusions. All risk policies are typically notably more expensive as a result.

I'm not sure how easy it would be to find insurance which would cover you against a window spontaneously breaking - you certainly aren't going to find a policy which will insure you against everything, which seems to be what you're hoping for?

If you wanted to know what risks were covered, couldn't you just have spent the 3 weeks reading the policy yourself if you already had a copy of it?0 -

Thanks again, that makes perfect sense to me and I think you are quite right re there being one single policy covering the entire development and the workings of that as you describe are exactly what I think goes on, and it all makes a lot of sense which is why I think it would be better to have my own buildings cover if I can and my insurer would be happy with that.Sandtree said:There is nothing illegal or technically to stop you having multiple policies running, its common in relation to commercial insurance as no single insurer wants to cover the whole Shard for example. In practice however mass market consumer insurance isn't designed for this and having two insurers will add delays as they check each others terms and see if either have slipped up and forgotten to include a "no other insurance" clause etc.

Your main issue however would be proving you have an insurable interest in the property given your lease states its the HA's responsibility to buy the insurance. Without this your policy wouldn't respond in the event of a claim... in practice the insurer may not realise its leasehold or think to check but you could be paying for nothing.

Its likely there is a single policy covering the full development which moves it into commercial/business insurance space which is often much more nuanced (rather than standard terms for everyone) and works at a different pace... large companies are much more comfortable paying out to fix urgent issues knowing they'll be reimbursed in due time whereas consumers often want the insurer to provide the suppliers and pay them up front etc hence have more automated systems, quicker response times etc.

Good point re paying for nothing if insurer doesn't respond.

I might contact HA and try to ascertain if there would be an issue with my just having my own Contents + Buildings insurance - my current one is due to lapse on 23rd of this month so it is an excellent time to address this.

I fully appreciate that you can't insure against everything, but I can certainly do my best to ensure I deal with competent insurance companies who don't take so long to get back to you. Like I say, this is my first ever incident/potential claim, so wanted to double check things before proceeding, didn't expect a 3 week wait.

Thanks again for your help") 0

0 -

You pretty much can, other than the outcome of your own criminal activity and certainly own deliberate acts... the reality however is that you quickly get into individual underwriting and that comes at a notable cost when compared to mass market standard wording/computerised pricing products.henrygregory said:I fully appreciate that you can't insure against everything

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards