We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Investing newbie

Comments

-

1. An S&S ISA is a type of account, you choose the platform, on the platform you choose the fund, the fund is not the ISA. Albemarle has covered above in more detail, the platform will have nothing to do with performance except to the extent that lower fees will help boost it.

2. What do you mean by managed fund? As a newbie you're unlikely to be knowledgeable/lucky enough to pick one that would do any better than a simple, risk appropriate multi-asset fund or fund-of-funds (https://monevator.com/passive-fund-of-funds-the-rivals/).

3. Part of the problem with picking such a fund now, is that bond yields seem to be rising and most expect that to continue for quite a few years. Higher rates means falling bond prices. Any low/medium risk fund will be bound to hold some bonds.

4. If it's in an ISA, you will never have to worry about tax on the gains anyway (unless Parliament change their mind which is unlikely partly because it's not economical for HMRC to go after the small amounts they could get by making ISAs less generous).

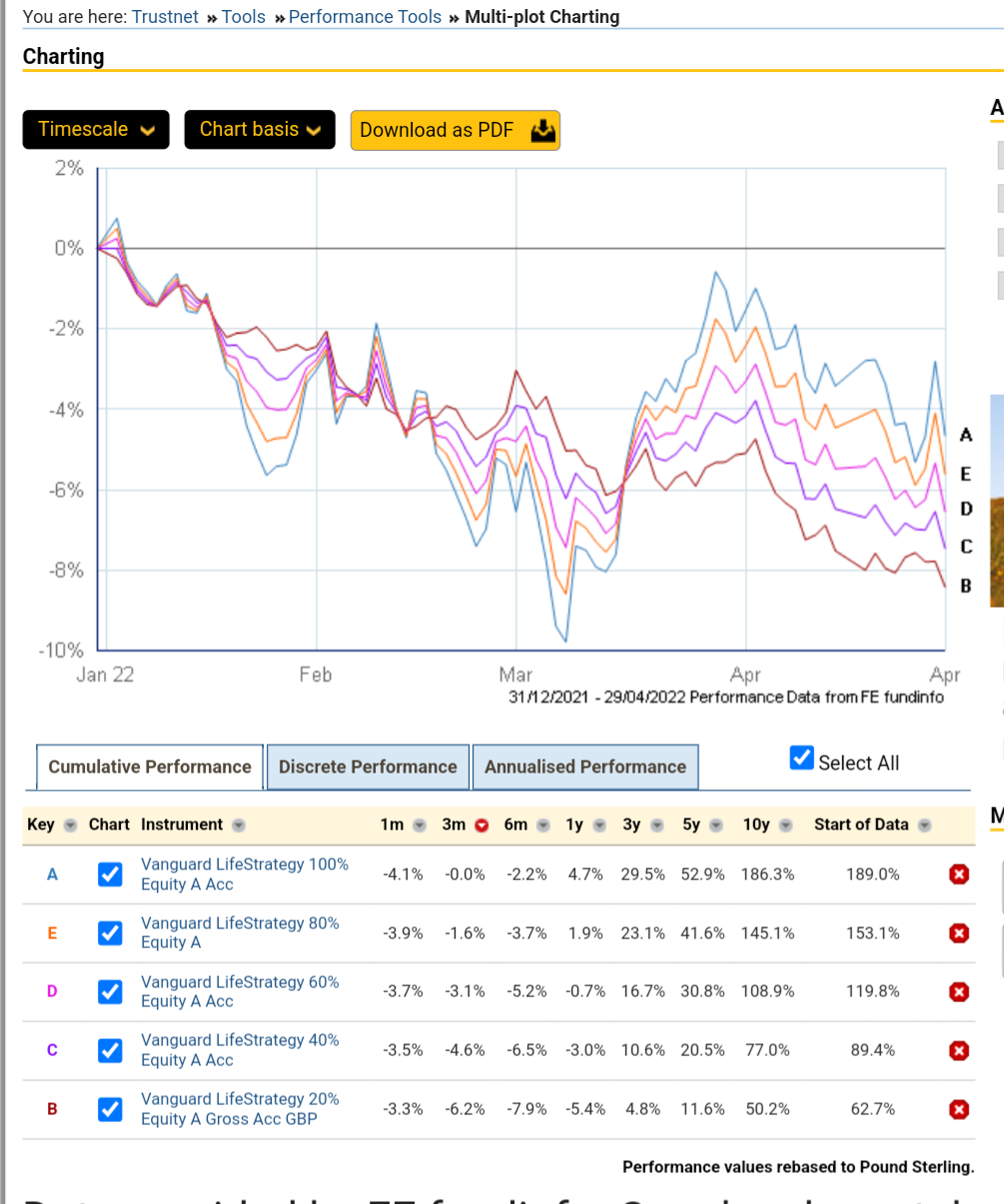

5. Having large savings has no tax consequences unless you are earning more interest than the savings allowance. You can also avoid such tax worries in future by using a cash ISA, though it is common sense to go for an S&S ISA if it's sensible in your circumstances, and I see no reasons why in your circumstances it wouldn't be.6. Define low to medium risk. For example, this year to date, conventionally lower risk funds such as Vanguard Lifestrategy 20 (80% bonds) have actually fallen more than VLS 100 (100% equity) as bond prices have reacted worse to inflation fears than equities. 0

0 -

Read this: https://monevator.com/category/investing/passive-investing-investing/Sandra97 said:

It's been mentioned a global unmanaged fund but could someone explain how this is less risky or similar risk to a managed spread? As a newbie a managed spread seems to make much more sense to me but again I'm totally open to feedback.

1 -

So far there's some amazing advice here thanks so much for everyone who has taken the time to write. I'm going to digest this through the day when I have a moment to properly go through the posts, I may have some further questions later on I hope that's alright with you all. I'm fairly excited at this now I have some very knowledgeable posters giving me feedback!0

-

Using the life raft of recent performance isn't always a sound basis upon which select to select individual investment funds. As is the case now. The sands are shifting. There's nothing like uncertainty to unsettle markets.mears1 said:

So, is the time for entry wrong now for Sandra97, for the funds suggested by other posters, whilst taking into her objectives?Thrugelmir said:Stock markets are a roller coaster ride. If you are prepared for the volatility and can be flexible as to timescale. Take a seat, buckle yourself in and see what the future holds. Past performance provides no guarantees. Time your entry wrong and potentially totally the reverse could occur.

A broad diversified investment should be at the core of your portfolio. Let the investment managers decide the asset allocation for you.1 -

The one month figures are more telling. As reality is finally sinking in and Corporate results disappoint. .tebbins said:1. An S&S ISA is a type of account, you choose the platform, on the platform you choose the fund, the fund is not the ISA. Albemarle has covered above in more detail, the platform will have nothing to do with performance except to the extent that lower fees will help boost it.

2. What do you mean by managed fund? As a newbie you're unlikely to be knowledgeable/lucky enough to pick one that would do any better than a simple, risk appropriate multi-asset fund or fund-of-funds (https://monevator.com/passive-fund-of-funds-the-rivals/).

3. Part of the problem with picking such a fund now, is that bond yields seem to be rising and most expect that to continue for quite a few years. Higher rates means falling bond prices. Any low/medium risk fund will be bound to hold some bonds.

4. If it's in an ISA, you will never have to worry about tax on the gains anyway (unless Parliament change their mind which is unlikely partly because it's not economical for HMRC to go after the small amounts they could get by making ISAs less generous).

5. Having large savings has no tax consequences unless you are earning more interest than the savings allowance. You can also avoid such tax worries in future by using a cash ISA, though it is common sense to go for an S&S ISA if it's sensible in your circumstances, and I see no reasons why in your circumstances it wouldn't be.6. Define low to medium risk. For example, this year to date, conventionally lower risk funds such as Vanguard Lifestrategy 20 (80% bonds) have actually fallen more than VLS 100 (100% equity) as bond prices have reacted worse to inflation fears than equities.0 -

To me a 10 year take is what I'd consider long term, I know I won't need access to the money in that time10 years is medium term for investing. Broadly speaking 8-15 years is medium term. 15+ is long termSo to avoid any doubt the 10 year period is my window to work in.The bulk of your contributions are not even going to be invested for the medium term but short term. year 1 has 10 years, year 2 has 9 years, year 3 has 7 years etc.

So, you need to look at risk relative to timescale.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

Just to pick up on this comment, the logic is flawed if you're considering investing because you'd be paying tax on savings interest.Sandra97 said:Have savings and these are now at risk of incurring tax so I need to do something.

On the other hand, investing is likely to be appropriate to protect money from inflation over the next ten years, so you're probably doing the right thing, but for a different reason!2 -

I get stocks and shares ISA is where you put money then within that wrapper you have a platform and from what I understand it's up to me whatever I want to do within that wrapper,

Nearly right

")

Typically you will have an investment platform that allows you to buy , sell and hold the investments they offer .

You can buy these investments outside an ISA, or inside a S&S ISA wrapper that the platform will operate/offer for you .

Outside an ISA there are no limits on how much you can invest but you may have to pay tax on gains and dividends. Inside an ISA there will be no tax to pay buy you are limited to £20K per tax year of new contributions .

Regarding what is long term . I think most people would consider 10 years long term but in some circumstances it is better to look further ahead ( pension planning etc ) However the more important point made is that you will be investing through most of the ten years, so some of the investments may only be 3 or 4 years old. This is an interesting graph that shows historically/on average , the chance of losing money over various time periods

Long-term investing: Increasing your chances of positive returns (nutmeg.com)

0 -

Sandra97 said:Good feedback thanks so far I'm just trying to digest it. @Albermarle thanks, you've mentioned being potentially pedantic - I'll be honest I'm not sure I really understand what you're trying to describe to me. I get stocks and shares ISA is where you put money then within that wrapper you have a platform and from what I understand it's up to me whatever I want to do within that wrapper, I really am new to this world and trying to understand it fully before venturing out.

It's been mentioned a global unmanaged fund but could someone explain how this is less risky or similar risk to a managed spread? As a newbie a managed spread seems to make much more sense to me but again I'm totally open to feedback.Also what do you mean by a managed spread? There is such a term as "spread betting" which is a gambling term but I can't find the term "managed spread" on Investopedia, if it's not there it's likely not a term people use.0 -

@tebbins I'm looking for an investment which will automatically invest in a range of things for diversification such as some stocks, bonds, cash etc. to reduce risk does that help? My terminology isn't perfect sorry as I mentioned right at the start this is new to me and I'm learning.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards