We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Has MSE helped you to save or reclaim money this year? Share your 2025 MoneySaving success stories!

COVID Travel Insurance - UK staycation

Sparky3900

Posts: 8 Forumite

Looking for some advice. My elderly parents booked a £400 UK hotel stay at the end of last year and took out travel insurance with a well-known provider to cover COVID.

Sadly they tested positive last week and were too unwell to travel and didn’t want to be contagious to others.

However, the insurer (taken out some months back) has argued that since GOV guidance has changed to advisory on isolation, they didn’t “have to” not go because of COVID. The company argue they could have gone and spread it instead and therefore they won’t pay out.

I’m really disappointed that my elderly parents did the right thing and are now being penalised. Is there anything they can do?

I’m looking at going away myself in June and considering COVID insurance but if the wording on T&Cs is being treated that ambiguously, I’m not sure insurance would be worth the paper it’s written on.

Any advice or tips appreciated

Any advice or tips appreciated

0

Comments

-

If they were too unwell to go, that is different from choosing not to go.

Forget about it trying to treat it as a Covid specific issue. What does the policy say about illness and the evidence required?0 -

This is one of the factors putting me off booking anything at all because the insurers are wriggling out of their responsibility. It isn't illegal to go out with Covid symptoms but it isn't advised. This is apart from not feeling well enough to travel which the insurer should still cover.Sparky3900 said:Looking for some advice. My elderly parents booked a £400 UK hotel stay at the end of last year and took out travel insurance with a well-known provider to cover COVID.Sadly they tested positive last week and were too unwell to travel and didn’t want to be contagious to others.However, the insurer (taken out some months back) has argued that since GOV guidance has changed to advisory on isolation, they didn’t “have to” not go because of COVID. The company argue they could have gone and spread it instead and therefore they won’t pay out.I’m really disappointed that my elderly parents did the right thing and are now being penalised. Is there anything they can do?I’m looking at going away myself in June and considering COVID insurance but if the wording on T&Cs is being treated that ambiguously, I’m not sure insurance would be worth the paper it’s written on.

Any advice or tips appreciated0 -

If someone has Covid symptoms, it isn't a case of 'choosing' not to go but of feeling that it is your duty/responsibility not to go. If the symptoms were mild (as I had with Covid), I would want to go but would feel that I shouldn't.Deleted_User said:If they were too unwell to go, that is different from choosing not to go.

Forget about it trying to treat it as a Covid specific issue. What does the policy say about illness and the evidence required?0 -

Ok but that’s nothing to do with whether your insurance would cover the costs.katejo said:

If someone has Covid symptoms, it isn't a case of 'choosing' not to go but of feeling that it is your duty/responsibility not to go. If the symptoms were mild (as I had with Covid), I would want to go but would feel that I shouldn't.Deleted_User said:If they were too unwell to go, that is different from choosing not to go.

Forget about it trying to treat it as a Covid specific issue. What does the policy say about illness and the evidence required?1 -

It’s a bit confusing.Sparky3900 said:Looking for some advice. My elderly parents booked a £400 UK hotel stay at the end of last year and took out travel insurance with a well-known provider to cover COVID.Sadly they tested positive last week and were too unwell to travel and didn’t want to be contagious to others.However, the insurer (taken out some months back) has argued that since GOV guidance has changed to advisory on isolation, they didn’t “have to” not go because of COVID. The company argue they could have gone and spread it instead and therefore they won’t pay out.I’m really disappointed that my elderly parents did the right thing and are now being penalised. Is there anything they can do?I’m looking at going away myself in June and considering COVID insurance but if the wording on T&Cs is being treated that ambiguously, I’m not sure insurance would be worth the paper it’s written on.

Any advice or tips appreciated

You said they were too unwell to travel, but the insurer said they could have gone.

were they too unwell or not?

what does their insurance say e.g. does it say “serious illness”? (It usually does).

if so we’re they seriously unwell or did they have mild symptoms?

it appears as though the insurer thinks they could have gone so you need to clarify the situation.

if it was the case that they had mild symptoms and weren’t actually too unwell to travel then they need to checks exactly what they are covered for.

wrt the wording, well it depends on what it says and whether you get a good policy.

my insurer will cover covid with evidence i.e. test

if you p aren’t sure on the wording e.g. “medical evidence” then I would suggest you ask before you go and keep the transcript.

so we’re they physically able to go or not?

and what does their policy say about covid?You have recourse to complaints and ombudsman if they aren’t playing fair, but it does need to be clarified as being too unwell to travel is different to not wanting to spread it.0 -

Their decision to not go was based on both in theory, but mainly because they presumed they would be covered to cancel and/or be able to rebook. They took the insurance out (well before GOV rules changed) purely for the COVID cover. After being told they wouldn't be able to claim under the terms of the policy, it then became a personal/moral decision.Deleted_User said:If they were too unwell to go, that is different from choosing not to go.

Forget about it trying to treat it as a Covid specific issue. What does the policy say about illness and the evidence required?

Nothing much in the policy about general illness at all. They're so down about it, they don't even want to go back and even look at the policy.

Just seems wrong that an inusrance company won't cover them because Gov guidelines changed from mandoatory isolation to advised isolation. Essentially the company (well-known) encouraged my parents to go with COVID on holiday because they wouldn't cover them. The hotel won't offer a refund or rebook either. They even had the cheek to ask for booking reference so they could re-sell the room!0 -

I'm guessing that this was specific "covid-insurance" rather than generic travel insurance?

if so then it probably only covers:

Can't travel because of lock-down at destination/home

Can't travel because of mandatory self-isolation

0 -

If the Government/Scientists are still advising people to stay at home (I'm not allowed to go to work with Covid), the insurer should still have to pay out if the person has proof of a positive test.lisyloo said:

Ok but that’s nothing to do with whether your insurance would cover the costs.katejo said:

If someone has Covid symptoms, it isn't a case of 'choosing' not to go but of feeling that it is your duty/responsibility not to go. If the symptoms were mild (as I had with Covid), I would want to go but would feel that I shouldn't.Deleted_User said:If they were too unwell to go, that is different from choosing not to go.

Forget about it trying to treat it as a Covid specific issue. What does the policy say about illness and the evidence required?0 -

lisyloo said:

It’s a bit confusing.Sparky3900 said:Looking for some advice. My elderly parents booked a £400 UK hotel stay at the end of last year and took out travel insurance with a well-known provider to cover COVID.Sadly they tested positive last week and were too unwell to travel and didn’t want to be contagious to others.However, the insurer (taken out some months back) has argued that since GOV guidance has changed to advisory on isolation, they didn’t “have to” not go because of COVID. The company argue they could have gone and spread it instead and therefore they won’t pay out.I’m really disappointed that my elderly parents did the right thing and are now being penalised. Is there anything they can do?I’m looking at going away myself in June and considering COVID insurance but if the wording on T&Cs is being treated that ambiguously, I’m not sure insurance would be worth the paper it’s written on.

Any advice or tips appreciated

You said they were too unwell to travel, but the insurer said they could have gone.

were they too unwell or not?

what does their insurance say e.g. does it say “serious illness”? (It usually does).

if so we’re they seriously unwell or did they have mild symptoms?

it appears as though the insurer thinks they could have gone so you need to clarify the situation.

if it was the case that they had mild symptoms and weren’t actually too unwell to travel then they need to checks exactly what they are covered for.

wrt the wording, well it depends on what it says and whether you get a good policy.

my insurer will cover covid with evidence i.e. test

if you p aren’t sure on the wording e.g. “medical evidence” then I would suggest you ask before you go and keep the transcript.

so we’re they physically able to go or not?

and what does their policy say about covid?You have recourse to complaints and ombudsman if they aren’t playing fair, but it does need to be clarified as being too unwell to travel is different to not wanting to spread it.

Wording is above. Medical evidence is the same as would be required for almost all policies and they would have been able to provide that no problem at all with positive lateral flows and PCR.

But the fact is that the company is arguing over the wording on the first bullet of "has to be cancelled". They are suggesting the holiday didn't "have to be cancelled" as the Gov rules have changed to "advised" isolation. In short, they are suggesting they could and should have gone to a hotel with COVID.

In terms of severity of illness, they were too unwell to go on holiday in my honest opinion. Being physically well enough is a subjective thing. I could contract Malaria and still physically go on holiday, but it wouldn't be very good for me. They took out the policy to cover this exact situation in good faith.0 -

It seems that isn't the case with this well known insurer. As the Government guidance is only "advised" isolation now then they won't be covering the cost.If the Government/Scientists are still advising people to stay at home (I'm not allowed to go to work with Covid), the insurer should still have to pay out if the person has proof of a positive test.

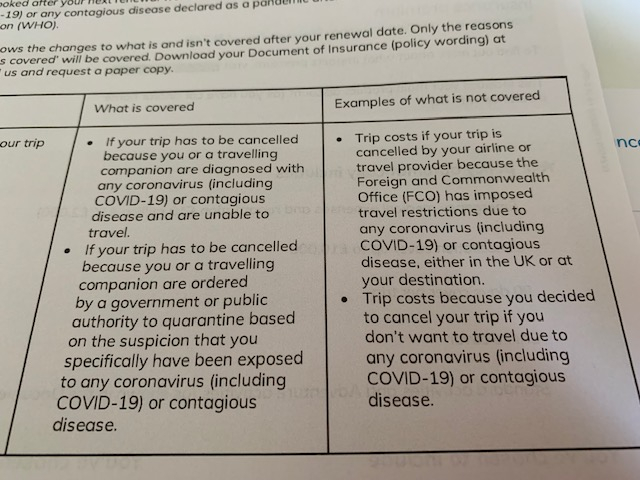

Every policy i have looked to cover my own staycation coming up in June has very similar ambiguous wording. Another example of a specific COVID clause below:

HAVE TO CANCEL and UNABLE TO TRAVEL are deliberately misleading and vague in light of the new "advice" from Gov.

I would assume i am covered for cancellation for my own holiday, but i bet i would be refused a claim on the same grounds i have explained previously.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353K Banking & Borrowing

- 253.9K Reduce Debt & Boost Income

- 454.8K Spending & Discounts

- 246.1K Work, Benefits & Business

- 602.2K Mortgages, Homes & Bills

- 177.8K Life & Family

- 260K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards