We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Pensions help/advice please

ClaireLR

Posts: 1,712 Forumite

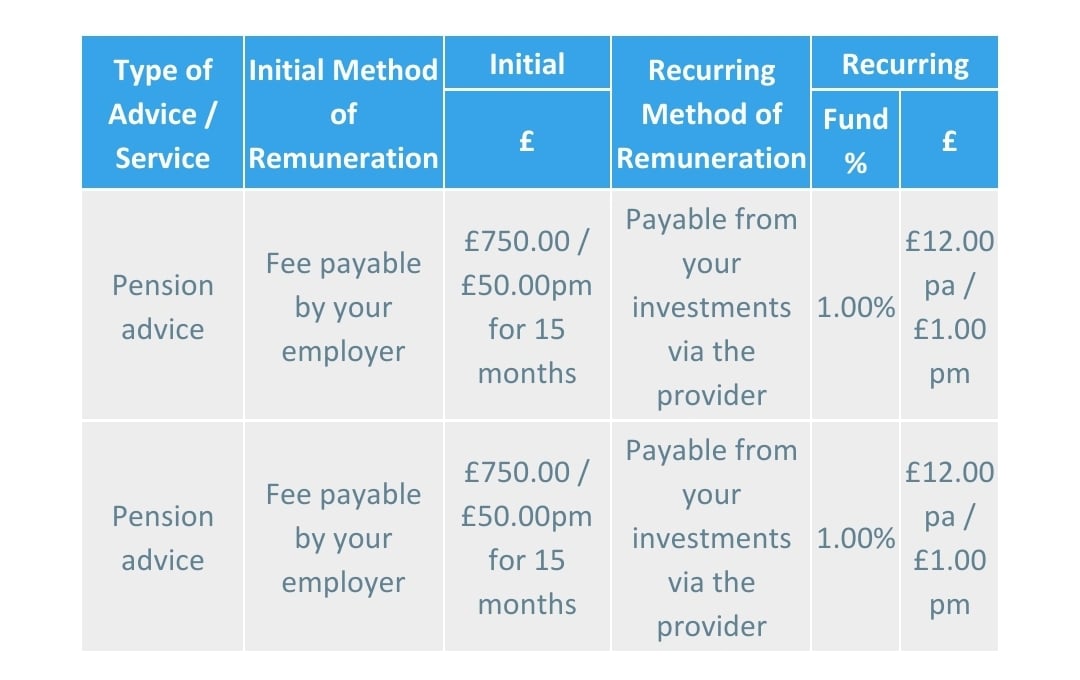

I have recently started to look into opening a pension.

Our probable pension provider has sent over these quotes.

Do they seem fair?

I dont fully understand how much he'll be charging us annually, can anyone advice

Is there anything else I need to look out for?

I don't know anything about pensions so please be gentle with me!

Thanks

Our probable pension provider has sent over these quotes.

Do they seem fair?

I dont fully understand how much he'll be charging us annually, can anyone advice

Is there anything else I need to look out for?

I don't know anything about pensions so please be gentle with me!

Thanks

Sometimes you have to go through

the rain to get to the

rainbow

0

Comments

-

Might be best to add that we'll be paying about £1500 per year per person into the pension, and it'll be done through our Ltd company.Sometimes you have to go throughthe rain to get to therainbow0

-

This is not just charges for the pension, there are charges for financial advice as well .

You can have a pension without financial advice and deal with any decisions your self .

Financial advisors have an initial fee ( £750 in this case ) but it seems your employer will pay this . Then they have an ongoing/recurring charge of !% of your funds , which you have to pay .

I have recently started to look into opening a pension.

Our probable pension provider has sent over these quotes.

You say you are looking to open a pension but these figures seem to indicate this is a workplace pension . Can you clarify the background ?1 -

It's a workplace pension for OP and her husband's limited company. A long thread started by OP last summer https://forums.moneysavingexpert.com/discussion/6292130/know-nothing-about-pensions-advice-appreciated#latest which has a lot of helpful info, so well worth OP revisiting the information given in that.Albermarle said:This is not just charges for the pension, there are charges for financial advice as well .

You can have a pension without financial advice and deal with any decisions your self .

Financial advisors have an initial fee ( £750 in this case ) but it seems your employer will pay this . Then they have an ongoing/recurring charge of !% of your funds , which you have to pay .

I have recently started to look into opening a pension.

Our probable pension provider has sent over these quotes.

You say you are looking to open a pension but these figures seem to indicate this is a workplace pension . Can you clarify the background ?

Hard to see why ongoing advice is needed given the amounts being contributed - a bit of diligent homework might be just as useful and a lot cheaper. Try https://www.moneyhelper.org.uk/en/pensions-and-retirementGoogling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!2 -

Thank you both.

Yes it's through our limited company.

I'll take a look back through that thread, I'd forgotten I'd even started it!

I understand that there is a charge for setting up the pension, I just wanted to make sure these fees were reasonable really.Sometimes you have to go throughthe rain to get to therainbow0 -

£750 initial is reasonable. Not sure you need any ongoing fee though. Not unless you plan to make regular ad-hoc contributions.

Aviva platform will not accept contributions direct from consumer and only via the adviser. So, if the ongoing avoids any future top up charges then you may consider that good value.I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

Hard to see why ongoing advice is needed given the amounts being contributed - a bit of diligent homework might be just as useful and a lot cheaper.

As Dunstonh says , the aviva platform seems to have over the years moved over to going via an advisor only , for new clients anyway . So if the OP wants to avoid this they need to pick one of the many providers that are happy to deal direct with the public, with no advice.

1 -

Thank you both. Just out of interest, would there be any reason to avoid going with a provider that's only via and advisor?Sometimes you have to go throughthe rain to get to therainbow0

-

The reason is that you have to pay for the advice .ClaireLR said:Thank you both. Just out of interest, would there be any reason to avoid going with a provider that's only via and advisor?

If you go to a provider who is happy to deal with you directly ( and there are many ) then there is no advisor cost. Of course then you have to decide yourself what to invest in .

I am presuming as well that the advice you will get will be restricted to these Aviva pensions only .

If you employed an IFA directly , they could look around the market for the best pension for you and advise you on other aspects of your personal finances. However for £1.5K pa you would struggle to find an IFA who was interested .1 -

Yes. It means any future transactions would have to be done via adviser. And in Aviva's case, they will not accept non-advised transactions. Each and every transaction must be advised. Advice means cost to you.ClaireLR said:Thank you both. Just out of interest, would there be any reason to avoid going with a provider that's only via and advisor?

That isn't a problem if you are using the adviser for ongoing servicing but where you are not, it is a problem.

The FOS uphold a complaint against an adviser a year or two back where the client was transactional but the adviser put them on a platform that would not allow direct to consumer transactions. it was believed to be the first complaint of its type. So, in reality, the adviser should really be taking this into account in their filtering of providers/platforms.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.2 -

I’m a transactional client. I pay direct into my pension once or twice a year and drop an email to my IFA to let them know when I’m going to do that. I’ve never been charged by the IFA for doing that. That’s normal, isn’t it?1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards