We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

High yield bonds: equity proxy… for what?

High yield bonds typically perform more like equities than investment grade bonds. My question is what type of equities are they could be consider a proxy for?

An example is Royal London Sterling Extra Yield Bond. The fund is 75% UK, so for the purpose of this exercise maybe we can consider it fully UK.

Map it for 15 years against UK All Companies and UK Smaller Companies and, up until mid-2013, all three performed similarly. Smaller companies then took off, while the RL fund continued to perform similarly to the UK All Companies with the difference that it held up better during market downturns.

UK All Companies holds, predominantly, FTSE 100 companies,

while RL is more distributed across the market cap spectrum. So my question is:

if the fund (and similar HY bond funds) can be considered equity proxies – and of

course feel free to challenge that – is it a proxy of UK All Companies (in many market conditions), or is

it a lower risk/lower return proxy of UK Smaller Companies (in some market conditions)? The rationale

behind the second option is that the growth of smaller companies’ share prices depends

mostly on growth in earnings; if you are a lender to those companies (ie you

buy its bonds) you only need the company to survive and meet its debt payments

to get your return – you do not need to it also to grow in size.

Comments

-

I wouldn't consider HYB as a proxy, or substitute, for equities. It's a different asset class with significant differences. They won't double or triple in a handful of years, they just can't. They do a different job. In my opinion they have no place in a growth portfolio but they have their uses in an income one. If you cannot substitute one with the other, it isn't a proxy

1 -

I think HYBs could be seen as more of an equity proxy than some defensive equities which are sometimes called bond proxies, but responding to poor terminology with slightly less poor terminology isn't necessarily helpful! Do you think it is pure coincidence that the two have tracked each other for 15+ years or does it tell us something about the UK market?

0 -

HYBs are not a proxy for equities. However, they are higher (sometimes very high) risk investment-grade bonds. When there is a fear event that impacts equities, it is likely to impact HYBs as well. However, it is possible that HYBs will not suffer similarly with all events and could suffer more than equities in others.

HYBs are a type that you hold for some of the cycle but dump for the rest. Most portfolios should only be holding 0% to less than 10% depending on the cycle and the type of investor you are.I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.3 -

dunstonh said:HYBs are a type that you hold for some of the cycle but dump for the rest. Most portfolios should only be holding 0% to less than 10% depending on the cycle and the type of investor you are.Not for the first time, I'll ask if you could expand on your post, to discuss cycle conditions that suit/don't suit HYBs (and any other kinds of bonds you feel like mentioning).Thanks.PS This seems a well written article (including "High yield bonds and equities tend to respond in a similar way to the overall market environment").

1 -

Have you tried comparing HYB with a multi-asset fund?

0 -

masonic said:Have you tried comparing HYB with a multi-asset fund?

Funny lad – Christmas crackers next year?

Care to critique the article I linked to? (Seriously, cos your posts are (usually) good.)

1 -

aroominyork said:masonic said:Have you tried comparing HYB with a multi-asset fund?

Funny lad – Christmas crackers next year?

Care to critique the article I linked to? (Seriously, cos your posts are (usually) good.)

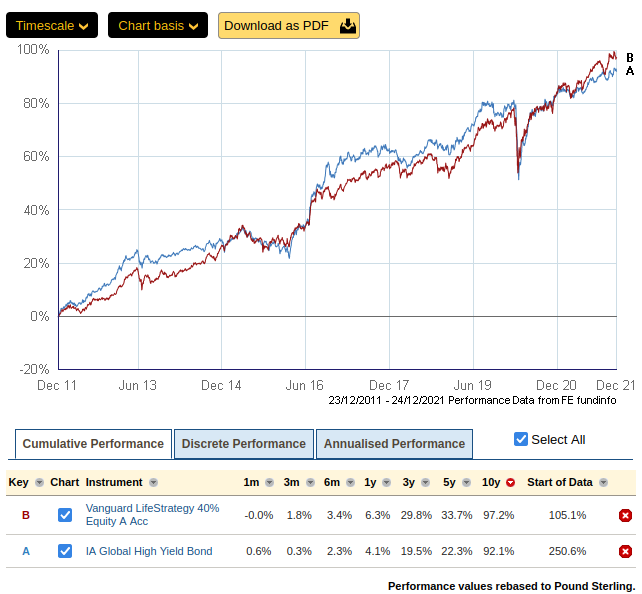

Believe it or not, I wasn't teasing you (well, maybe a little), but check this out: I broadly agree with some of the points raised in the article (low correlation with investment grade, more correlated to equities, less volatile than equities), but not others (similar total return to equities), nor the conclusion that they add diversification in addition to a mixture of equities and investment grade bonds, I submit the above chart as Exhibit A vs diversification. I'm sure I don't need to show you the equivalent with VLS100 to counter the suggestion total return is comparable.I think a case can be made for holding them instead of equities if you are a cautious investor (although I would look to other options personally, those which we have discussed elsewhere), or if you are an adventurous investor you could add them during a bear market and sell them as late as you dare during a bull market (better stated by dunstonh above).Where they might have value (I simply don't know) is in a rising interest rate environment. On a simple price basis, you wouldn't expect them to lose value in the same way as lower yielding debt, but on the other hand the companies issuing the debt are likely to be less resilient to those conditions and may well struggle with refinancing leading to increased defaults. Interest rates rising from practically nothing to "normal levels" is uncharted territory, pun intended.1

I broadly agree with some of the points raised in the article (low correlation with investment grade, more correlated to equities, less volatile than equities), but not others (similar total return to equities), nor the conclusion that they add diversification in addition to a mixture of equities and investment grade bonds, I submit the above chart as Exhibit A vs diversification. I'm sure I don't need to show you the equivalent with VLS100 to counter the suggestion total return is comparable.I think a case can be made for holding them instead of equities if you are a cautious investor (although I would look to other options personally, those which we have discussed elsewhere), or if you are an adventurous investor you could add them during a bear market and sell them as late as you dare during a bull market (better stated by dunstonh above).Where they might have value (I simply don't know) is in a rising interest rate environment. On a simple price basis, you wouldn't expect them to lose value in the same way as lower yielding debt, but on the other hand the companies issuing the debt are likely to be less resilient to those conditions and may well struggle with refinancing leading to increased defaults. Interest rates rising from practically nothing to "normal levels" is uncharted territory, pun intended.1 -

So you take my All Companies chart, masonic's VLS40 chart, and dunston would probably tell us "a little bit of data is a dangerous thing".

1 -

Charts of recent past performance tell us nothing about the future. In recent years, people have become increasingly desperate to obtain a return on their investments, and the prices of high yield bonds have risen as a result. The premium interest that they pay over safe government bonds has shrunk dramatically, but the risk of default remains the same (or may even be larger). The recent price rises are unlikely to be repeated any time soon, and there may be a nasty crash.0

-

I would also be interested in what you have to say too dunstonh, at the moment HYB are 9.5% of my portfolio, but I also have 5.7% in individual bonds which (hopefully) mature next May and August and and 8% in BTL's, which I will sell in 2-3 years, and I had earmarked those for HYB's, hence my interest in your opinion, because my holding would increase to about 23%. I do have a real issue with keeping money in cash, I just can't bring myself to lock in a guaranteed loss (with tax and inflation), despite knowing that I will go through 1-2 crashes in my lifetime (maybe I am in denial) and I do struggle to decide on the proportions of my portfolio.aroominyork said:dunstonh said:HYBs are a type that you hold for some of the cycle but dump for the rest. Most portfolios should only be holding 0% to less than 10% depending on the cycle and the type of investor you are.Not for the first time, I'll ask if you could expand on your post, to discuss cycle conditions that suit/don't suit HYBs (and any other kinds of bonds you feel like mentioning).Thanks.PS This seems a well written article (including "High yield bonds and equities tend to respond in a similar way to the overall market environment").

To give you an idea of my position I will be 64 in a couple of weeks, and I am probably going to retire in 1-3 years (maybe longer), I like my job and only work about 2 days a week on average. My current portfolio is:Cash 2% Investment property 8% Own home 12% Fixed pension 15% Bonds 15% REIT's 19% Equities (excl reits) 29%

I include my own home because my spreadsheet is more of a record of wealth than a pure investment portfolio.

Chuck Norris can kill two stones with one birdThe only time Chuck Norris was wrong was when he thought he had made a mistakeChuck Norris puts the "laughter" in "manslaughter".I've started running again, after several injuries had forced me to stop0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards