We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

PLEASE READ BEFORE POSTING: Hello Forumites! In order to help keep the Forum a useful, safe and friendly place for our users, discussions around non-MoneySaving matters are not permitted per the Forum rules. While we understand that mentioning house prices may sometimes be relevant to a user's specific MoneySaving situation, we ask that you please avoid veering into broad, general debates about the market, the economy and politics, as these can unfortunately lead to abusive or hateful behaviour. Threads that are found to have derailed into wider discussions may be removed. Users who repeatedly disregard this may have their Forum account banned. Please also avoid posting personally identifiable information, including links to your own online property listing which may reveal your address. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Am I worried for nothing? Exchanging 3 months prior to completion.Stressing out

Comments

-

What's being gambled, if the deal is off? Seems to be more risky to be obliged to complete the purchase of a smouldering ruin, even if you do have insurance to sort it.Thrugelmir said:

Property suffering a fire during the period between exchange and completion is an expensive gamble to take.user1977 said:

You couple that with risk only being transferred on completion (and presumably a condition that either party can pull out if there is significant damage).Thrugelmir said:

The sellers insurance provides you with no protection. As you are not the insured under the terms of the policy.cramsteems said:

We are going to try and make it the sellers responsibility to insure the property between exchange and completion.aoleks said:this could be financial suicide, don't agree to it any cost. extremely risky...

What I'm describing is how just about every purchase in Scotland proceeds, and there's generally a longer period between "exchange" and completion than in England.0 -

What works in other countries is unlikely to work here, as it seems like the developers / vendors are insisting on unconditional exchange. They're clearly going to reject anything that allows the buyers to pull out for any reason.

If I were in the OP's shoes, I'd probably take the risk as long as the completion date was guaranteed -- i.e., that the sellers must complete/move on that date even if the new build is not ready. This assumes their jobs are secure (as they say) and their ability to get a mortgage is typical / they're not stretched to the brink.

Yes, it's a risk, but there are also risks in doing nothing: losing the house, potentially not finding something else for a long time, when mortgage rates will likely be higher, prices may be higher, etc.

We're talking about very low likelihood events - job loss, fire, etc. in the next 90 days.0 -

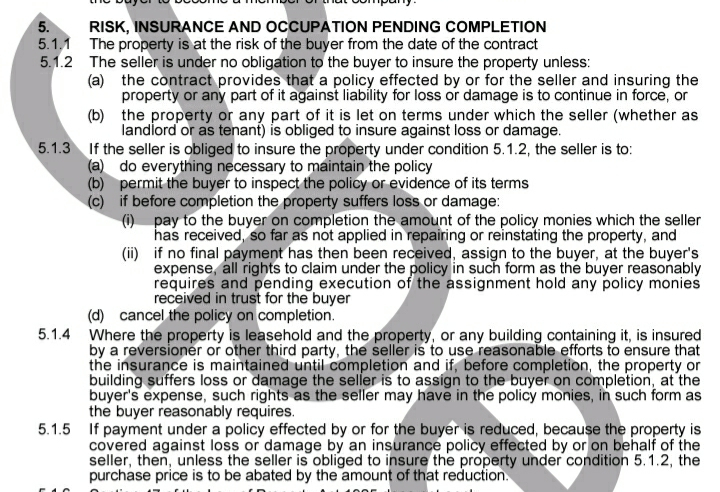

Section 5 of the Standard Conditions of Sale puts the risk on the buyer from the date of the contract, not completion. There is no onus on the seller to provide insurance unless specified in the contract.user1977 said:

You couple that with risk only being transferred on completion (and presumably a condition that either party can pull out if there is significant damage).Thrugelmir said:

The sellers insurance provides you with no protection. As you are not the insured under the terms of the policy.cramsteems said:

We are going to try and make it the sellers responsibility to insure the property between exchange and completion.aoleks said:this could be financial suicide, don't agree to it any cost. extremely risky...

0 -

Thanks for the comment. We are leaning towards taking the risk, we have very stable jobs and no financial commitments currently or due to appear. Our mortgage is 4.5x salary which I assume is standard? We have the long stop date at which the seller must move out, I have confirmed this with the solicitor, if they don’t we should get our deposit back and could take them to court for not completing. Although if this does happen we will likely renegotiate completing but would need another mortgage offer as ours expires the day of completion.LAD917 said:What works in other countries is unlikely to work here, as it seems like the developers / vendors are insisting on unconditional exchange. They're clearly going to reject anything that allows the buyers to pull out for any reason.

If I were in the OP's shoes, I'd probably take the risk as long as the completion date was guaranteed -- i.e., that the sellers must complete/move on that date even if the new build is not ready. This assumes their jobs are secure (as they say) and their ability to get a mortgage is typical / they're not stretched to the brink.

Yes, it's a risk, but there are also risks in doing nothing: losing the house, potentially not finding something else for a long time, when mortgage rates will likely be higher, prices may be higher, etc.

We're talking about very low likelihood events - job loss, fire, etc. in the next 90 days.0 -

Rather you than me, op.

What people do for bricks and mortar

0 -

Yes, I know that's the standard conditions. We're talking about a variation to those conditions.MaryNB said:

Section 5 of the Standard Conditions of Sale puts the risk on the buyer from the date of the contract, not completion. There is no onus on the seller to provide insurance unless specified in the contract.user1977 said:

You couple that with risk only being transferred on completion (and presumably a condition that either party can pull out if there is significant damage).Thrugelmir said:

The sellers insurance provides you with no protection. As you are not the insured under the terms of the policy.cramsteems said:

We are going to try and make it the sellers responsibility to insure the property between exchange and completion.aoleks said:this could be financial suicide, don't agree to it any cost. extremely risky...0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards