We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Contacted regarding missold PCP

Comments

-

Bad Credit to what level? If it isn't obvious level of bad credit, then this will be quite a high bar to climb. Going from a consumer credit score won't help much as this isn't the information that credit houses go from.sheramber said:if a rate is sky high due to bad credit then fair enough, however that hasn't happened, the rate was inflated for their own financial gain

That is what you have to prove to make a claim.0 -

There are certain area's where compliance does come into play.Deleted_User said:The analogy is that if I got into Waitrose to buy a tin of tomatoes (same as me going to a car dealership to buy a car), the person at the till (or the car salesman) doesn't have to tell me that I could go to Aldi and get the same product for less (just as the car salesman has no obligation to tell you that you could arrange finance from a bank). Claiming that you didn't know that there are other finance packages available or that you didn't shop around is not a reason for miss-selling

https://www.allvehiclecontracts.co.uk/InformationArticle/Compliance-Your-Rights/Your-Rights---Personal-Contract-Hire.html

https://www.fca.org.uk/news/news-stories/our-work-motor-finance

Working in banking. I know exactly how much notice people take when you start reading a compliance statement.....Life in the slow lane0 -

Credit "scores" do not get seen by lenders, the company has algorithms to score you internally that you will never see for commercial reasons. Someone getting a high APR does not mean the company deliberately inflated the interest rate for some bonus or commission. This is just another scam from claims companies now the PPI gravy train has run out, all the company needs to show is that they create a deal based on what the system shows them, having an APR that was supposedly set higher for a backhander is up to the CMCs to proveontheroad1970 said:

Bad Credit to what level? If it isn't obvious level of bad credit, then this will be quite a high bar to climb. Going from a consumer credit score won't help much as this isn't the information that credit houses go from.sheramber said:if a rate is sky high due to bad credit then fair enough, however that hasn't happened, the rate was inflated for their own financial gain

That is what you have to prove to make a claim.0 -

Indeed. Part f my point. To prove wrong doing, they would need access to internal scoring and decision making.Deleted_User said:

Credit "scores" do not get seen by lenders, the company has algorithms to score you internally that you will never see for commercial reasons. Someone getting a high APR does not mean the company deliberately inflated the interest rate for some bonus or commission. This is just another scam from claims companies now the PPI gravy train has run out, all the company needs to show is that they create a deal based on what the system shows them, having an APR that was supposedly set higher for a backhander is up to the CMCs to proveontheroad1970 said:

Bad Credit to what level? If it isn't obvious level of bad credit, then this will be quite a high bar to climb. Going from a consumer credit score won't help much as this isn't the information that credit houses go from.sheramber said:if a rate is sky high due to bad credit then fair enough, however that hasn't happened, the rate was inflated for their own financial gain

That is what you have to prove to make a claim.0 -

I think you meant to reply to Purplee who made the statement about bad credit.ontheroad1970 said:

Bad Credit to what level? If it isn't obvious level of bad credit, then this will be quite a high bar to climb. Going from a consumer credit score won't help much as this isn't the information that credit houses go from.sheramber said:if a rate is sky high due to bad credit then fair enough, however that hasn't happened, the rate was inflated for their own financial gain

That is what you have to prove to make a claim.0 -

Nothing note worthy. Last I heard from them was about 3-4 weeks ago saying they were trying to reach an out of court settlement.Purpleee said:

Isn't the argument that according to FCA rule they were not allowed to unjustifiably charge such a high APR? Is it not the same as no one being allowed to charge uxorious interest rates on a loan? Happy to be corrected, and I didn't relate to the whole tomato/Waitrose analogyDeleted_User said:

APR is not negotiable, you get offered what the lender deems acceptableTiptop79 said:My point about the APR was that I didn't believe it was negotiable, much like when you apply for a credit card and the rate they give you is not negotiable.

The reason for not going anywhere else for finance was that I didn't know I could and that if I have been offered that rate by the dealer, a credit check had been conducted so it would be the same wherever I go. Perhaps even worse as a search had been done on my file.

I've always had company cars and didn't know anything about car finance etc.

What doesn't seem fair is that someone has potentially been paid more for overcharging me on interest and not making that clear. It's funny how they tried to get me to sell my car back to them after two years and told me they could do a better finance deal and I was on one of the highest they had seen.

I didn't sell it back to them btw.

You didn't know you could go elsewhere for finance - that is your issue, not miss-selling. Waitrose don't need to tell customers you can get the same product cheaper at Aldi. A bit of research would have told you that you could get the finance elsewhere

A single credit check will not stop you being able to apply for credit for another type of finance, particularly a soft check before the hard check when you agree to the finance.

You were not overcharged on interest, you paid what the firm deemed right for their risk. 2 years later your credit was presumably better or their lending criteria was relaxed as you had been paying it fine for 2 years. What happened 2 years after the original sale is moot.

Daniel2curtis - Any update?Daniel2curtis said:Thanks. I'll try and remember to update people on the outcome. These pcp claim websites are all over the Web and I havent found one report of a successful claim, or to be fair one report that someone has been scammed either. It almost feels like they are building up a massive amount of claims/data.

I've chased it up twice recently and got an identical response both times about how I'm in the first stage of claim and it might take months for the financial company to reply blah blah blah.

I'll check on their progress in another week or two although I imagine I'll get the same response.0 -

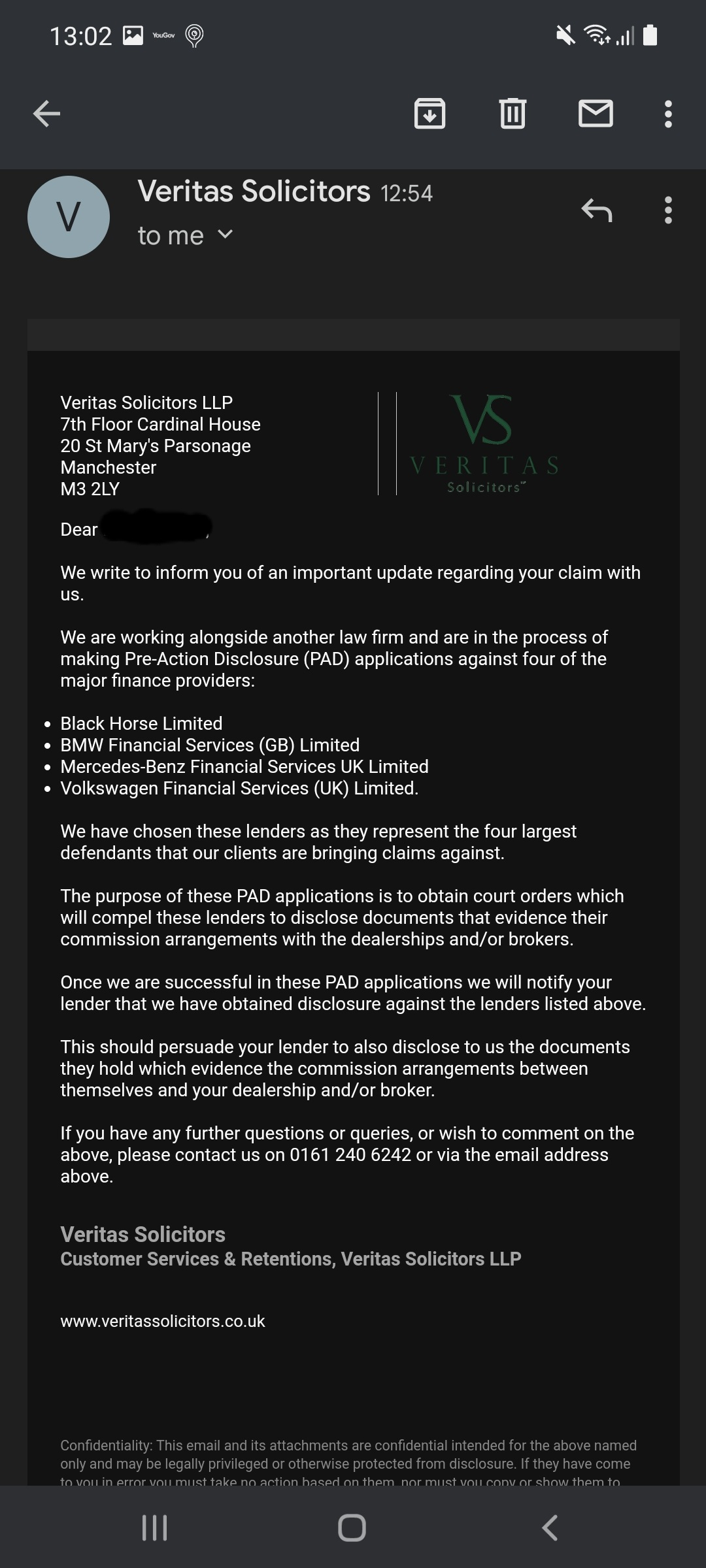

Just had this email through as an update.

0 -

Reading through this thread can someone explain how people are buying new cars with 9% APR? I’ve never seen a manufacturer with such a high rate for a new car. And I thought for new manufacturers offered a fixed rate that they guarantee by simply setting the lending criteria and deciding the percentage of deals they will take the hit on?

I didn’t think you could change the APR either way. No dealer I’ve ever dealt with has ever said ‘sorry you can’t have advertised APR but I can sell you at a higher rate’. Never. For second hand. Sure. It’s why second hand pcp is a mugs game. But for new they’ve always made clear rates are fixed. Sometimes a manufacturer will offer a low rate and a higher one but with deposits contribution and it’s up to you to work out which will be best for you with your deposit size etc but that’s still two fixed offers.So what am I missing?0 -

You're missing the bandwagon and the chance of free money/compo. I've bought cars at 9.9% when banks were offering 2.9% but the free servicing/deposit contribution etc have made the overall deal worthwhile (and I've transferred to a lower APR loan as soon as I could without losing the benefits). I also know that the dealer will have earned money out of the initial 9.9% acceptanceiwb100 said:So what am I missing?

Am I going to go back now and challenge that I was mis-sold ? Am I hell - but then I'm not one to waste my time/energy lining some bottom-feeding marketing/legal company's pockets

It's just the latest in a long line of money-making opportunities for someone2 -

I get that. But people seemingly have bought NEW cars where the dealer has jacked up the rate rather than use the manufacturer offered rate. I’ve never heard or seen that so I’m curious as to what circumstances that can happen in?k3lvc said:

You're missing the bandwagon and the chance of free money/compo. I've bought cars at 9.9% when banks were offering 2.9% but the free servicing/deposit contribution etc have made the overall deal worthwhile (and I've transferred to a lower APR loan as soon as I could without losing the benefits). I also know that the dealer will have earned money out of the initial 9.9% acceptanceiwb100 said:So what am I missing?

Am I going to go back now and challenge that I was mis-sold ? Am I hell - but then I'm not one to waste my time/energy lining some bottom-feeding marketing/legal company's pockets

It's just the latest in a long line of money-making opportunities for someone

Like I say for brand new cars I’ve always assumed rate cannot change from advertised rates.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards