We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Pension contributions- Reducing tax

Stevensuperbike

Posts: 48 Forumite

Hi there I am pretty new to the concept of retirement planning etc. I will be contributing to my pension pot through a workplace pension scheme where my employer pays 5% and so will I as a minimum (or maybe more after this).

my question is about tax relief on pension contributions… I earn 26620 a year and tax code is 1397m. I was wondering if I put 48% of my salary into a pension my gross income after pension has come out is lower than the tax free allowance so I pay 0 tax on income. Now do I still get tax relief on my contribution as I’m not paying tax? Or am I missing something here???

many thanks in advance

Steve

my question is about tax relief on pension contributions… I earn 26620 a year and tax code is 1397m. I was wondering if I put 48% of my salary into a pension my gross income after pension has come out is lower than the tax free allowance so I pay 0 tax on income. Now do I still get tax relief on my contribution as I’m not paying tax? Or am I missing something here???

many thanks in advance

Steve

0

Comments

-

It depends on the method used to make the contributions! Pensions are not the simplest topic.Stevensuperbike said:Now do I still get tax relief on my contribution as I’m not paying tax? Or am I missing something here???

If you make contributions through an employer pension scheme via a "net pay arrangement", (where contributions are deducted from your gross pay before income tax is calculated) then you won't get tax relief on the contributions you make on income below the personal allowance (£12,570 pa).

However, if you make contributions using "relief at source" (where you make contributions out of your net pay after income tax has already been taken off, and the pension provider subsequently adds basic rate tax relief on once the contributions arrive in your pension account), then you do benefit from tax relief on the full amount paid in, even on income where you didn't pay tax. However, there is a limit to the maximum amount that can be paid in, the total amount (including the tax relief) cannot exceed your annual UK earnings.

Salary sacrifice is a third method, but I'll ignore that here, because minimum wage rules would prevent you sacrificing down to £0 income anyway.

So the question is, which method does your workplace pension use? Is it NEST (that's a relief at source scheme) or another one? If you look at your pension statements, does the transaction history show basic rate tax relief being added on, or not?0 -

For most people, including yourself from what you have posted, pension contributions do not save any income tax as they are paid using the "relief at source" method.

But they mean your pension fund gets a nice boost.

For example if you contributed 48% of £26,620 that would be £12,777.60. The pension company, courtesy of HMRC, will add basic rate tax relief of £3,194.40 giving you a pension fund of £15,972.

But you will still pay the exact same amount of income tax on your £26,620 (approx £2,530).

0 -

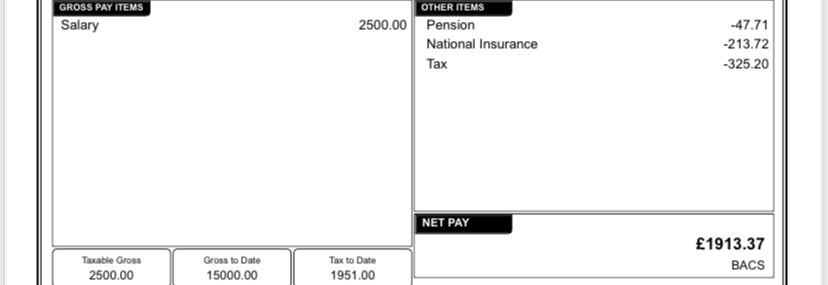

Hi thanks for you reply’s. I’m confused would anyone know by looking at this if it is relief at source contributions or the net pay arangements? My tax code on here is 1048m? Sorry for the questions. Thanks0

Hi thanks for you reply’s. I’m confused would anyone know by looking at this if it is relief at source contributions or the net pay arangements? My tax code on here is 1048m? Sorry for the questions. Thanks0 -

I think -325.20 tax refers to the 2500 gross so pension paid after tax and NI? ThanksStevensuperbike said:Hi thanks for you reply’s. I’m confused would anyone know by looking at this if it is relief at source contributions or the net pay arangements? My tax code on here is 1048m? Sorry for the questions. Thanks1 -

Your salary and taxable amount are both £2,500 so it will be relief at source.

You should see £11.92 in tax relief being added to your pension fund on top of the £47.71.

£47.71 is only 1.9% so it looks like your employer is making use of the rule which means part of your pay is ignored for pension contribution limits so maybe worth upping your %.

https://www.thepensionsregulator.gov.uk/en/business-advisers/automatic-enrolment-guide-for-business-advisers/automatic-enrolment-earnings-threshold1 -

Thanks for confirming.

So, the answer to your original question, as Dazed said above, is that yes you can get tax relief of £3194 into your pension despite having only paid tax of £2530")

So obviously beneficial to pay in as much as you can afford to tie up for the long term.1 -

I earn 26620 a year and tax code is 1397m.My tax code on here is 1048m?

Could you clarify?

0 -

Sorry the slip with 2500 gross was from last year but still is how my employer shows the pension contributions. My tax code this year is 1397m with 26620 per year gross.1

-

If you have access to the pension providers website ( you should have ) you should actually be able to see the tax relief being added.

You might want to see also on the website , in what investment(s) your pension is invested .

It is not so important when the fund is small but is worth noting at least .2 -

I have checked on their website and it shows the transactions. On my payslip has for example 47.71 deducted for pension but when I checked it says I’ve paid in 59.64 (I assume this figure includes the gov 25% tax relief boost after tax & ni) ? ThanksAlbermarle said:If you have access to the pension providers website ( you should have ) you should actually be able to see the tax relief being added.

You might want to see also on the website , in what investment(s) your pension is invested .

It is not so important when the fund is small but is worth noting at least .0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.6K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.7K Work, Benefits & Business

- 603K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards