We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Foolishness of the 4% rule

Comments

-

A 5% failure rate might be too high, but 5% is not an "excellent chance". It's quite a small chance, but it's consequences could be great... go back to my previous post and substitute "win-win" for "an excellent chance of living past 100".Deleted_User said:

A 5% chance of outliving money and dying in poverty is way too high in my book. A healthy and relatively. wealthy 65 year old has a much, much higher probability of getting to 100. The table below gives 10% for a healthy 65 yo male in the US. US is a bit behind other developed countries on longevity. Its higher if you also screen by wealth and for a female. And mortality stats trend to longivity. I am 51. For all we know, in 15 years time a quarter of well of 65 year olds will live past 100.bostonerimus said:

Ah, this is obviously some strange use of the phrase "excellent chance of living past 100" that I wasn't previously aware of.Deleted_User said:I would only consider an annuity if my life expectancy was severely shortened or I reached a seriously old age without the money to sustain my needs for an extended poeriod.A healthy 65 year old has an excellent chance of living past 100.

The beauty of an annuity is that its a win-win-win. If your house burns down its not exactly a “win” even if insurance pays out. Here you get to live longer AND you get to collect. And if thing do go wrong and you die early its still a financial win because you can afford to invest the balance of your portfolio more aggressively and spend more money safely before you die.

An annuity would have been ok for my Mum though as she was a heavy smoker who lived to 91 and she would have been buying one in 1986 when payout rates were double what they are today.“So we beat on, boats against the current, borne back ceaselessly into the past.”0 -

Its not “5%” that is an “excellent chance” if you actually read what I said. It is 10% for a healthy 65 year old American, higher for women, higher for Canadians and Brits, even higher for well off retirees and higher again if you hit 65 in 10 or 15 years.You could buy an annuity today to be paid starting from age 65 in 10 years, gain on mortality credits for ages 55 to 65, gain on investment growth and gain on improvements in life expectancy. Kinda cool.0

-

just for interest, here are a few results with annuitiesMK62 said:Thanks for the rather comprehensive reply......it pretty much sums up my current view too (despite my temporary inability to calculate 4% of 500k....😉).....

That said I'm genuinely interested in alternative views.....it would be interesting to see how the above compared to taking an annuity back in 1965......the rates on offer then might have been quite different.

I'm not against the concept of annuities, per se, just the current rates on offer........

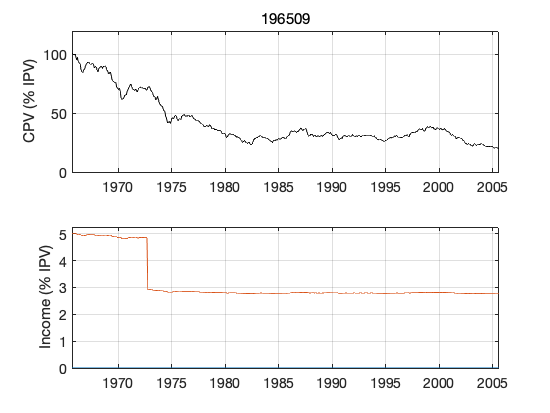

First up the portfolio with small (10%) variation in spend as I described in a previous post... it survives OK with a small reduction in expenditure from target (5% for first 7 years, 3% thereafter)

I've used annuity rates calculated with US interest rates but with current life expectancy (this means that the rates are lower than historically)

Buying an annuity at 70 years old with 50% of the remaining portfolio (the black line is the total income, the blue line income derived from annuities and the red line the income generated by the portfolio.

Not a good decision - that has definitely made things worse in terms of income.

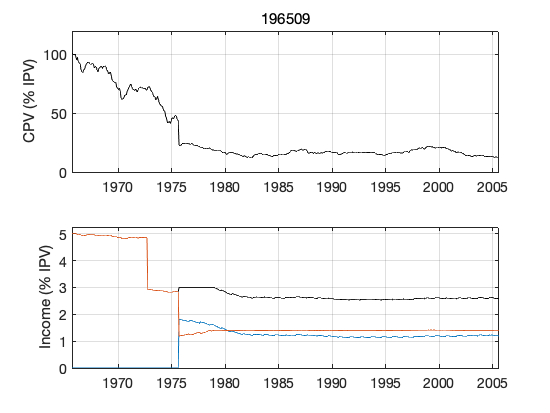

Now here are the results for using 50% of the remaining portfolio to buy an annuity at 80 years old

That has improved things somewhat meeting the 3% target from 80 years old onwards

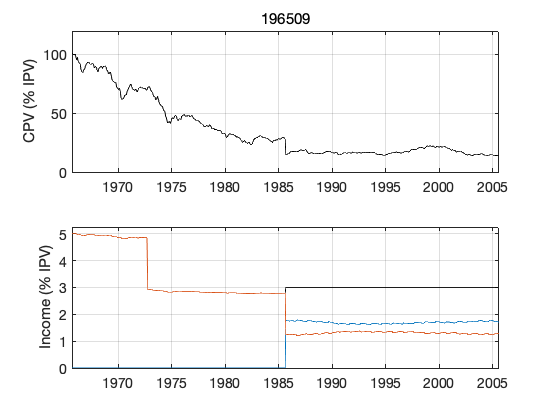

Now instead of buying an annuity at a single point in time, buy at 75, 80, and 85 with 10%, 20%, and 30% of the remaining portfolio

So, annuities could, if bought at the appropriate time have made a difference during the difficult retirements starting in the 1960s - but fairly marginal in this case. I should note that retiring at 60 makes the whole process much more difficult compared to retiring at 65 - see following result

1 -

Deleted_User said:Its not “5%” that is an “excellent chance” if you actually read what I said. It is 10% for a healthy 65 year old American, higher for women, higher for Canadians and Brits, even higher for well off retirees and higher again if you hit 65 in 10 or 15 years.The UK's Office of National Statistics disagrees......they say that the chances of a 65yo British male reaching 100 are 2.9%. (that is, only 2.9% of 65yo British males alive today, will make it to 100)Deleted_User said:You could buy an annuity today to be paid starting from age 65 in 10 years, gain on mortality credits for ages 55 to 65, gain on investment growth and gain on improvements in life expectancy. Kinda cool.Is it?...

") .......out of interest, how much does one of those cost, today?

.......out of interest, how much does one of those cost, today?

0 -

10% is still not "excellent" to me. If we are talking about deferred annuities then the maths is different, are those available in the UK and how much do they cost? Buying an immediate life time annuity right now is, IMO, a bad Idea and I would stick with cash and consider buying an annuity later in retirement or if the numbers stack up buy the longevity insurance of a deferred annuity.Deleted_User said:Its not “5%” that is an “excellent chance” if you actually read what I said. It is 10% for a healthy 65 year old American, higher for women, higher for Canadians and Brits, even higher for well off retirees and higher again if you hit 65 in 10 or 15 years.You could buy an annuity today to be paid starting from age 65 in 10 years, gain on mortality credits for ages 55 to 65, gain on investment growth and gain on improvements in life expectancy. Kinda cool.“So we beat on, boats against the current, borne back ceaselessly into the past.”0 -

The UK's Office of National Statistics disagrees......they say that the chances of a 65yo British male reaching 100 are 2.9%. (that is, only 2.9% of 65yo British males alive today, will make it to 100)

Its completely irrelevant. Sick 65 year olds have different life expectancies and annuity rates. They wouldn’t even need a longivity insurance.

I provided expectancies for healthy Americans from actuaries, the stats that matter for annuities: https://www.longevityillustrator.org/ Its a 10% chance of getting passed 98. Average life expectancy is 3 years longer for Brits, so will be higher percentage although I don’t have numbers for healthy Brits. And ones chances could be even higher if he is well off and understands money, which a lot of people on this board do.

0 -

Is it?... .......out of interest, how much does one of those cost, today?

A 55 year old female in the US would get an 8.05% payout rate at 65 based on 2012 mortality data. A male would get a better payout rate. You would need to get a quote for something accurate.

0 -

Something to think about: shares perform very well during inflationary periods ( we are not talking hyperinflation). Shares get devastated during deflation. We do not actually know what will be happening in 10 years” time. Someone in pre-retirement mode might only need another 10k of secure income to top up state pension t provide for “bucket 1” of a basic lifestyle. For a deferred annuity that could cost a small portion of the overall invested portfolio, like 10 or 5%. The rest could then be invested and spent more aggressively. .

0 -

I'm enjoying this discussion and it is refreshing to hear from someone championing annuities.

Personally I've got between 5-8 years of working/contributions to go before I have to make a decision, but it's good to fully understand the options. I found these articles in the telegraph which discuss current annuity rates in the uk. They are behind a paywall, but I think you have one free article per brower 'type' (I have firefox, edge and chrome)...

Annuity vs drawdown: which is best for a £100k, £500k and £1m pension pot (telegraph.co.uk)

https://www.telegraph.co.uk/pensions-retirement/financial-planning/how-make-pension-last-20-years-pay-less-tax-2021/?fbclid=IwAR2JhH_TdtBcuytBevhppl8qxQbI5qH-1a745tqGNxOzVs8gHBJrb-YVAEk

Neither article makes me want to put all of my hard earned cash into an annuity, but there is certainly a good argument for a combination of both annuity and drawdown. But in my case, I'll wait and see what the story is in 2026.1 -

5 years in the current environment is a long time. Already early indications of interest rate rises around the globe. Consequence of this will be higher yields on Government bonds. Annuities may well provide an attractive alternative if global growth stalls.HeyYeah said:

Neither article makes me want to put all of my hard earned cash into an annuity, but there is certainly a good argument for a combination of both annuity and drawdown. But in my case, I'll wait and see what the story is in 2026.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.9K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.4K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards