We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

A little theory ...

valiant24

Posts: 479 Forumite

We all know, or think we know, or I think we all think we know that over the long term equities always offer the best asset class returns, and for the past hundred or hundreds of years have - again over the long term - beaten inflation.

Is there any simple guide or explanation as to why equity values and returns consistently outperform inflation please?

Is there any simple guide or explanation as to why equity values and returns consistently outperform inflation please?

0

Comments

-

Equities have been shown to not provide a hedge against inflation over shorter time horizons. The underlying theory is that both company revenues and earnings will rise over time due to inflation. Some industrial sectors perform better than others in periods of high inflation. Such as those where demand is inelastic i.e. energy, medical services, drugs for example.1

-

Without wanting to trivialise your reasonable question, to embellish the background a bit:equity values and returns may not consistently outperform inflation; the chart (link below) suggests they didn't in France for a century;you can find decades with the same outcome in other countries. That's not the long term centuries that you specified, but it can be long term for individual investors. https://evergreensmallbusiness.com/rate-of-return-of-everything-study-in-line-charts/But to your question. A bond is a promise to return the money you lent, and comes with the safety of an obligation to give your money back. You lose the use of your money for that period, and thus expect compensation for any inflation which will reduce its value by the time the money is returned to you. You also expect some compensation for the deferral of the benefits you get from you spending that money. Bond returns, as safe as they are, should have above inflation returns - long term.Equities are riskier than bonds; there's no promise you'll get your principal back. Investors demand more return when there' more risk. Does that get to your question?2

-

There have been periods where the market has gone sideways for around a decade or more. Real returns are highlighted in red.

EhCv7GqUwAACMF8 (900×504) (twimg.com)

On occasions high P/E valuations have led to a stalling in the markets over the next few years.

EdnQ6gMWkAIhcXy (700×548) (twimg.com)

It has been argued markets are that point again today.

EZ_91bOXQAAp1Zo (1400×1169) (twimg.com)

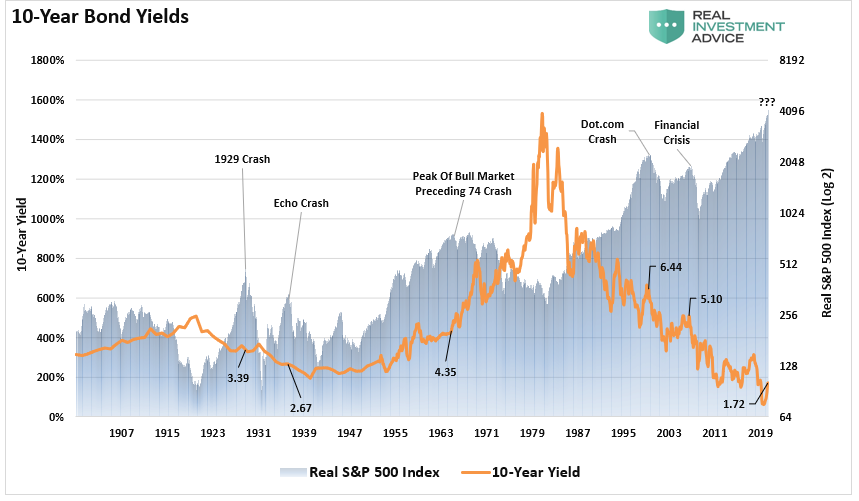

Bond yields are very low and markets are high but not all are on a high valuation. The UK for one is on a forward P/E of 12.

Bond yields were low during the 1940's similar to today but valuations were nearer P/E 10 and today over 20. Tricky times but drip feeding monthly is all you can do with your asset allocations.

Rates-Forward-Returns-042021.png (859×501) (realinvestmentadvice.com)

2 -

It was very interesting, but I'm not sure that it quite does.JohnWinder said:......

Does that get to your question?

Quite clearly, bonds- or at least gilts - are not beating inflation at present. It's difficult to see why people, including me, are invested in them other than, in my case, "Because Lars told me to".

Conversely, it's difficult to imagine that stocks can continue to rise as they have over the past 18 months, or even 5 years, yet the advice is to stay invested in VWRL and the like.

I'm just musing really. There are no "right" answers. Intuitively I want to be out of the global tracker. But, faute de mieux, I stay invested for fear of missing out!

Thanks for listening ;-)

0 -

On the final graph most of the peaks and crashes are clearly defined , like the shape of the top of a triangle . But preceding the 1974 crash there was a decade when prices remained at a high level ( with a few ups and downs) before eventually crashing.coastline said:There have been periods where the market has gone sideways for around a decade or more. Real returns are highlighted in red.

EhCv7GqUwAACMF8 (900×504) (twimg.com)

On occasions high P/E valuations have led to a stalling in the markets over the next few years.

EdnQ6gMWkAIhcXy (700×548) (twimg.com)

It has been argued markets are that point again today.

EZ_91bOXQAAp1Zo (1400×1169) (twimg.com)

Bond yields are very low and markets are high but not all are on a high valuation. The UK for one is on a forward P/E of 12.

Bond yields were low during the 1940's similar to today but valuations were nearer P/E 10 and today over 20. Tricky times but drip feeding monthly is all you can do with your asset allocations.

Rates-Forward-Returns-042021.png (859×501) (realinvestmentadvice.com)

Maybe that is what will happen this time . No further significant growth in equities but no crash either , although a few mini ones and recoveries .

Pure speculation of course .2 -

Equities are for the long term. Private investors generally uses safe bonds for short/medium term reasons, either you cant stomach a major short term loss or you have short/medium term needs for the money.valiant24 said:

It was very interesting, but I'm not sure that it quite does.JohnWinder said:......

Does that get to your question?

Quite clearly, bonds- or at least gilts - are not beating inflation at present. It's difficult to see why people, including me, are invested in them other than, in my case, "Because Lars told me to".

Conversely, it's difficult to imagine that stocks can continue to rise as they have over the past 18 months, or even 5 years, yet the advice is to stay invested in VWRL and the like.

I'm just musing really. There are no "right" answers. Intuitively I want to be out of the global tracker. But, faute de mieux, I stay invested for fear of missing out!

Thanks for listening ;-)

Dont do anything purely because some guru tells you to. Test out his/her arguments, If you cant justify something to yourself dont do it.

As an equity investor you should believe that in the long term shares generally must rise, if you dont you would be foolish to invest in them. Fortunately there are good reasons for beliving that equities will generally rise the same or faster than inflation:

- equities in solid companies are a real asset as they represent ownership of businesses which in turn own both physical and intangible assets. Inflation is a decreasing value of currency against real assets.

- the profits of the businesses you part own are the differences between the costs and the incomes. Both should broadly rise with inflation and so therefore should the profits.

- as living standards rise across the world increasing numbers of people are investing. In the UK more people are investing in equity based pensions. Generally there is a growing demand for equities.

I agree with the aim of investing as widely as possible but dont use a global tracker. The reason is that global trackers are insufficiently diversified for me as I believe they focus too much on particular large companies and particular geographies leaving insufficient opportunities for gains from elsewhere.

5 -

In my opinion there isn't a reason why equities outperform inflation, it's just the case that in stable economies (where hyperinflation is the exception rather than the norm), they just do. It's an observation, not a corollary.The comments I post are my personal opinion. While I try to check everything is correct before posting, I can and do make mistakes, so always try to check official information sources before relying on my posts.0

-

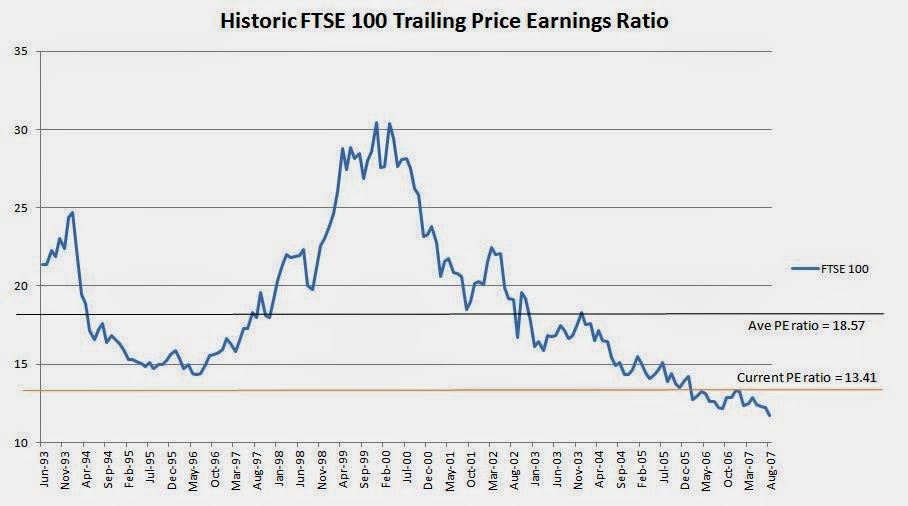

Had a link where it showed various ratios by country but I'm afraid I can't find it for now. Found this which shows the FTSE 100.Bobziz said:

From headwinds to tailwinds – a reversal in fortune for the FTSE 100? | FTSE Russell

Set this to MAX the FTSE All Share. Things will be improving since the pandemic.

UK P/E ratio, 1993 – 2021 | CEIC Data

This highlights the UK problems since the year 2000. P/E at 30 and many of the big guns in the index have since gone ex growth. Banks oils etc.

FTSE+100+trailing+PE+chart.JPG (908×506) (bp.blogspot.com)

Kind of shows historically the FTSE being P/E 10-15. Will it change ?

1620982432961.png (751×437) (c-dn.net)

Thing is there's a lot hidden away in a P/E ratio. Look here at Growth 28 and Value 16. Big difference. Again as this is the SP 500 forward P/E's showing Value at 16 it's hard to imagine many of the FTSE shares trading any higher ?

5HjmFY57 (855×483) (twimg.com)

Just to throw in at the bottom here. There was a thread in January 2020 ? from this investor. Well he's at it again with a read or podcast. Take your pick. He likes the UK for value.

Jeremy Grantham’s Bubble Predictions — MoneySavingExpert Forum

Jeremy Grantham, we're in one of the greatest bubbles in financial history | MoneyWeek

1 -

That's the danger of reading a book (and is based on data of an era) that was conceived before the impact of QE kicked in.valiant24 said:JohnWinder said:......

Does that get to your question?

Quite clearly, bonds- or at least gilts - are not beating inflation at present. It's difficult to see why people, including me, are invested in them other than, in my case, "Because Lars told me to".0

{kind=link}

{kind=link}

{kind=link}

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.5K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.6K Work, Benefits & Business

- 603K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards