We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

2 mortgages chances or options?

Would I be able to get a second mortgage for a property for myself? What likely mortgage could I get? Or would I need to turn the first mortgage to a buy to let? I either need a second mortgage or will be forced to rent

Comments

-

@col81 Plug your data into (including the background property and running costs) a couple of lender affordability calculators and see what it returns. That will give you a very very rough idea of whether the numbers stack up for what you are looking to borrow keeping the existing property. Depending on the lender, with a property in the background you may also be capped at a certain LTV.

https://www.santanderforintermediaries.co.uk/calculators-and-forms/affordability/

https://www.nationwide-intermediary.co.uk/calculators/affordability-calculatorI am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

You may struggle to convert to buy to let considering you are renting to family.0

-

I have completed the Santander application it suggests I could borrow upto £140k I presume this is because I pay 350 mortgage but take 250 rent so its only costing me 100 per month0

-

@col81 Generally speaking, mainstream residential lenders are unlikely to take into account the rent you get from this property unless it's formally tenanted.col81 said:I have completed the Santander application it suggests I could borrow upto £140k I presume this is because I pay 350 mortgage but take 250 rent so its only costing me 100 per month

Just to be clear, the affordability calculator is only as good as the data you put in and the criteria for the lender, so anything you get from that may change.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

It is a family member that lives there with a full tenancy agreement0

-

I had to produce the tenancy for the housing benefit/council. I take a 250 income costs me 350 so as a lender I presume they will look at it as 100 a month commitment the houses I am looking at are in the £120k region0

-

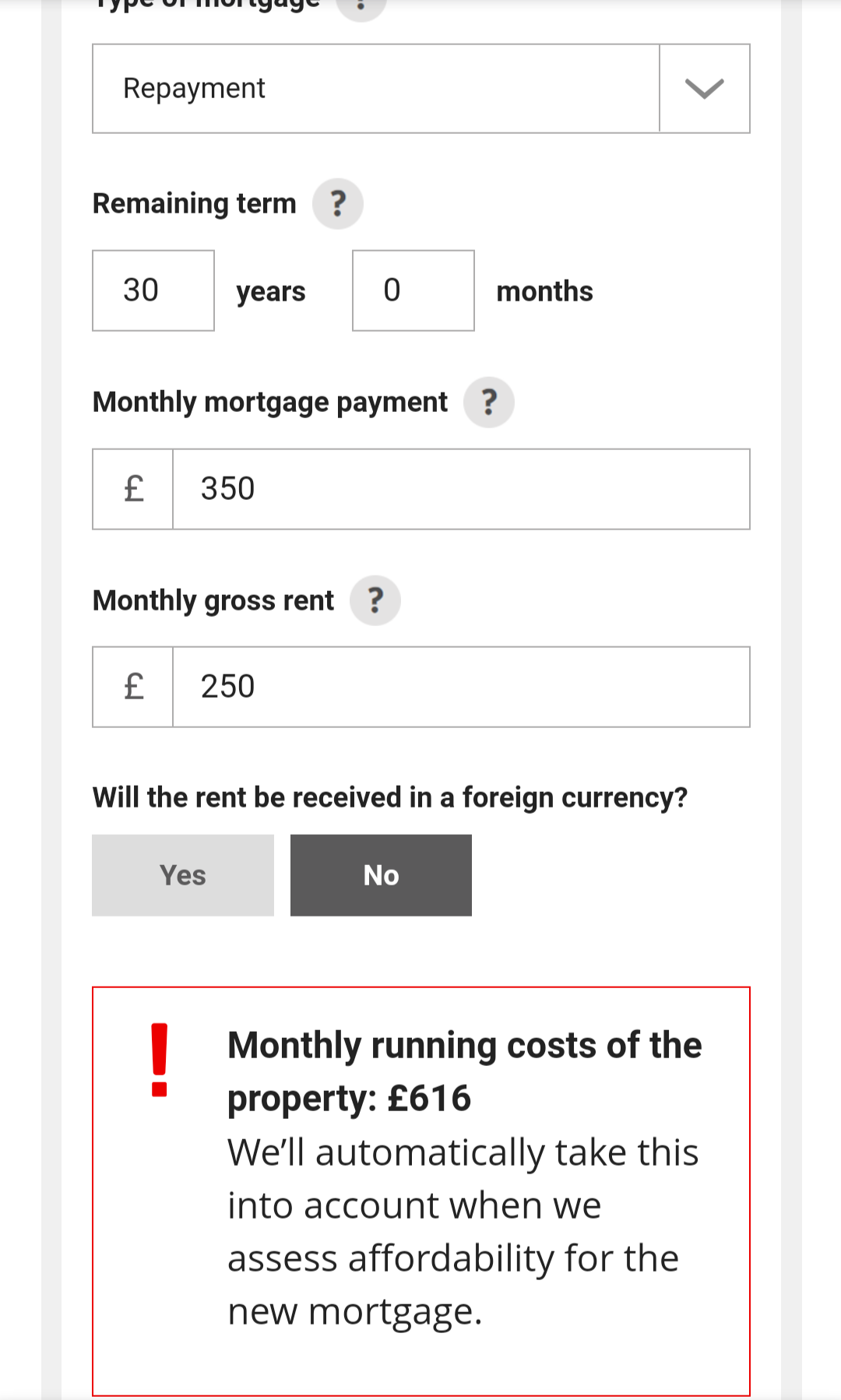

@col81 It's not that straight forward unfortunately. The Santander calculator should show you what the calculated monthly running costs are (as per Santander, every lender will look at it differently) is from the numbers you put in. Like so -

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

3 -

OP, you will struggle to get a 120k BTL mortgage with a monthly rental income of £250 due to stress testing. It will have to be closer to £550-600, perhaps more since you will be a higher rate taxpayer with 45k salary and over 5k rental income. Talk to an MB.0

-

Can I not just keep the current mortgage running? It is only 350 pcm and I receive 250. Surely I can borrow a lot more for a second mortgage I want around £120k on the next house and will have 10% deposit.0

-

If the bank will give you what you want then of course you don't need to change. I only commented based on what you mentioned about changing to BTL.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.6K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.7K Work, Benefits & Business

- 603.1K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards