We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Poor credit rating caused by HSBC account fees

markcromwell80

Posts: 7 Forumite

Hi,

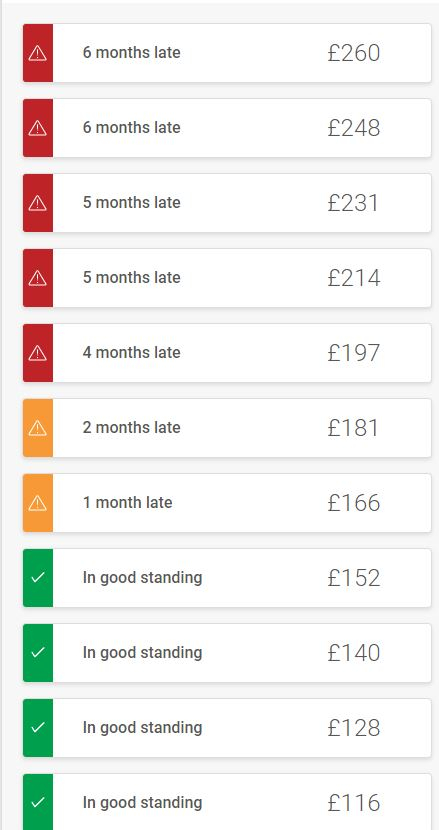

I have recently applied to a lender for a re-mortgage in order to fund some home improvements. I was refused immediately due to a poor credit score. Upon investigation, this is because of late payments on a HSBC account that I no longer use. The account has a £150 agreed overdraft on it which has gone over this amount due to the HSBC Insurance Aspects fee being applied (12.95). As you can see from the attached image, the account was £116 overdrawn and is now £260 overdrawn due of this fee (with added overdraft charges that have also increased due the balance increase). A payment was previously put over every month by standing order from another account to cover this but this has accidently been removed and the account has been forgotten about - I know this is poor on my behalf. I have now cleared the balance but according to Experian, which the lender used, it will take up to 6th months to put me in the 'good' credit rating. Can I do anything about this as the only reason the account has breached the overdraft terms is a insurance policy that has never been used? I have had this account since 2002 when I started University which had an account fee attached to it and I am in the process of trying to claim back the account fees as I was told that I needed to take this out as a student account.

I have discovered this online - 'To be eligible for HSBC Advance, you'll need to pay in a minimum of £1,750 per month or £10,500 over 6 months.'

I have recently applied to a lender for a re-mortgage in order to fund some home improvements. I was refused immediately due to a poor credit score. Upon investigation, this is because of late payments on a HSBC account that I no longer use. The account has a £150 agreed overdraft on it which has gone over this amount due to the HSBC Insurance Aspects fee being applied (12.95). As you can see from the attached image, the account was £116 overdrawn and is now £260 overdrawn due of this fee (with added overdraft charges that have also increased due the balance increase). A payment was previously put over every month by standing order from another account to cover this but this has accidently been removed and the account has been forgotten about - I know this is poor on my behalf. I have now cleared the balance but according to Experian, which the lender used, it will take up to 6th months to put me in the 'good' credit rating. Can I do anything about this as the only reason the account has breached the overdraft terms is a insurance policy that has never been used? I have had this account since 2002 when I started University which had an account fee attached to it and I am in the process of trying to claim back the account fees as I was told that I needed to take this out as a student account.

I have discovered this online - 'To be eligible for HSBC Advance, you'll need to pay in a minimum of £1,750 per month or £10,500 over 6 months.'

So it appears that the account shouldn't even be open as I do not meet this criteria??

Are there any grounds for help with this during COVID-19 as our finances have become very tight due to some time on furlough?

Any help is much appreciated.

Thanks,

Mark

Are there any grounds for help with this during COVID-19 as our finances have become very tight due to some time on furlough?

Any help is much appreciated.

Thanks,

Mark

0

Comments

-

Tight spot, but afraid there is nothing you can do here. As you note management of this account has been poor by yourself and this is the result. HSBC have done nothing wrong here and won't remove the data from your report. Best thing you can do now is pay this off and close the said account.

I am afraid the lender you are applying to will probably still decline come the 6th owing to the payment history. While it may be updated on the 6th to say its in good standing, the late payments are still going to be there for the next 6 years. Would reccomend approaching a mortgage broker who may be able to assist.

J0 -

There's no grounds for removing the markers, but the good news is that Experian don't decide your credit rating. Lenders do that.

Get the account up to date and then get yourself a decent broker who will place your application with the right lender for your circumstances.2 -

Thanks for the reply.

Will the lender discover the missed payments too?

What do you mean about getting the account up to date? As I mentioned in the original post, the account balance is now cleared.

I am going to contact the bank to try to get the fees removed over the weekend. Do you think this is viable?

Thanks,

Mark

0 -

Lenders will see missed payments and assess you accordingly.

I doubt they'll return the fees, but no real harm in asking. But I'd focus on your remortgage.1 -

I agree with the above - the missed payment markers are an accurate representation of what has happened so it's unlikely you'll get them removed. By all means give them a call and ask nicely if they can remove them, but I'd expect them to say no.

Lenders will see the missed payments when they view your credit file (note they see the credit data not the "score") and use their own criteria to determine if that's something they care about or not. I'd either wait 6-12 months before making any further applications or look for a broker who specialises in people with adverse credit if you need to make your application sooner.1 -

That is going to be really frustrating to wait that long as there will be nothing else affecting the score. I would guess that the quality of mortgage that I would be able to get would be severely affected by having adverse credit? In terms of how much they would lend and the interest rate offered?

Having a poor credit score because of this is very annoying. I haven't ever missed anything else like a mortgage, loan, credit card, utilities etc. And I am guessing that the lender would never read between the lines on this.

0 -

markcromwell80 said:That is going to be really frustrating to wait that long as there will be nothing else affecting the score. I would guess that the quality of mortgage that I would be able to get would be severely affected by having adverse credit? In terms of how much they would lend and the interest rate offered?

Having a poor credit score because of this is very annoying. I haven't ever missed anything else like a mortgage, loan, credit card, utilities etc. And I am guessing that the lender would never read between the lines on this.

It very much depends on how much weight the particular lender places on these missed payments. As ZX81 says, all lenders will look at the data in your file, and assess you based purely on that. One lender may not care too much about a few missed payments in an otherwise well-managed history, another may not touch you with a barge pole - it depends on their individual lending criteria. As has already been mentioned, a broker can often be a good option for someone in your position.And please ignore your score, it's not even seen by lenders.

0 -

The original application was done through a broker. Their advice was just to wait for a while0

-

Do I look elsewhere or is it really best to wait? We have just put in for planning permission 0

-

There's no harm in looking elsewhere, but I wouldn't get your hopes up.markcromwell80 said:Do I look elsewhere or is it really best to wait? We have just put in for planning permission0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards