We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Interest Rates and Inflation

jim8888

Posts: 430 Forumite

As I project forward into my retirement, I construct disaster scenarios in my head such as "What if inflation went to 10%"?

I remember mortgage interest rates being 14% at one point in the Nineties. I'd no savings or investments then but, I assume if I had, I'd have been earning 14% on those if I did have money in the bank.

I wondered, therefore, if inflation goes up by 5%, would you then assume a return on your investments would move up to, say, 9% to enable you to continue with a Safe Withdrawal Rate of 4% from your Direct Contribution pension fund?

I remember mortgage interest rates being 14% at one point in the Nineties. I'd no savings or investments then but, I assume if I had, I'd have been earning 14% on those if I did have money in the bank.

I wondered, therefore, if inflation goes up by 5%, would you then assume a return on your investments would move up to, say, 9% to enable you to continue with a Safe Withdrawal Rate of 4% from your Direct Contribution pension fund?

0

Comments

-

Many moons ago I posted asking if there is a "link" between inflation and interest / investment rates for the same reason that you are asking.The general conclusion is that there isn't one. However for my long term budget planning I use a figure for inflation, I then use a percentage of this for savings and investment. (eg I assume inflation is 4%, then savings / investments would be (say) 50% of this ie 2%..."It's everybody's fault but mine...."2

-

I would assume the opposite. As inflation goes up, especially if it goes above the target of around 2%, you can expect interest rates to follow eventually. This would likely cause your investments in equities and bonds to drop at least for a while. Now whether that causes you to change the 4% withdrawal rate is up to you. The 4% comes from a time in the late 1960's when inflation began to kick in and interest rates rose. Returns were terrible for over 10 years but the 4% survived even that.0

-

There is a link but it's now broken since the 2008 GFC. Base rates were used as a buffer against inflation, trying to slow things down , but worldwide governments are now running huge deficits and national debt.

Today we've just heard the UK borrowed £300bn in 2020-21 to cope with the pandemic and will borrow another £200bn this year 2021-22. It'll be loaded onto the national debt as ever but the bonus, that's if you can call it that , is it's borrowed at 0.8% which makes a huge difference. Can you imagine if new bond rates were 10% , that would be £50bn a year to finance in interest payments.

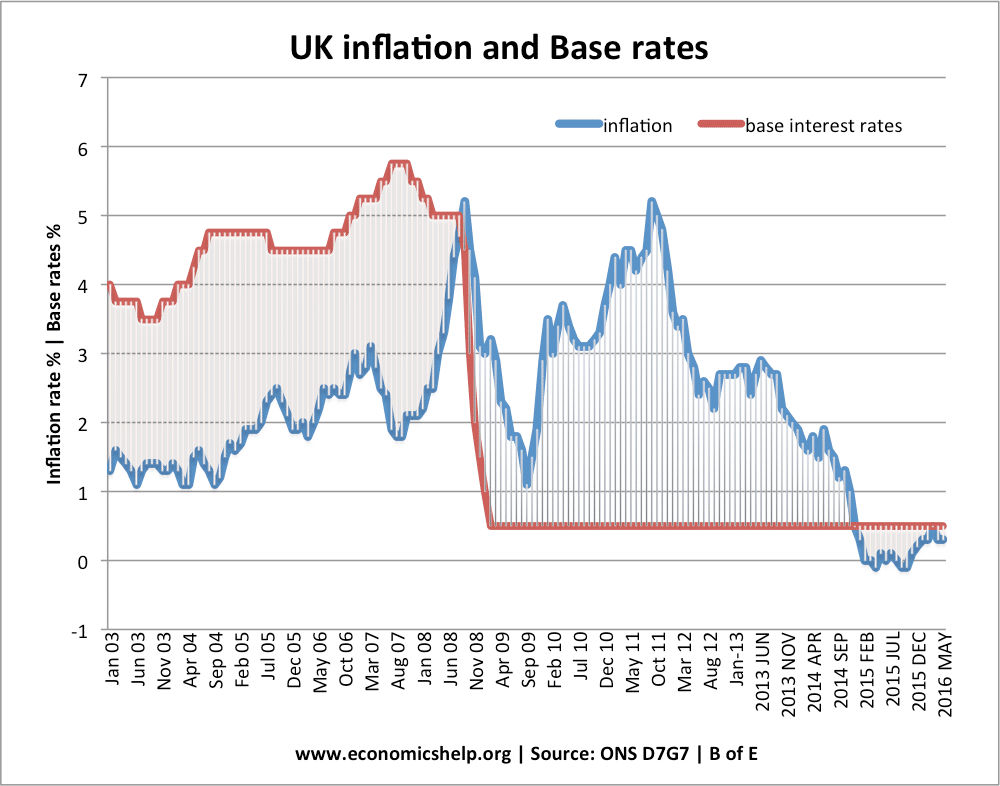

interest-rates-inflation.png (1000×786) (economicshelp.org)

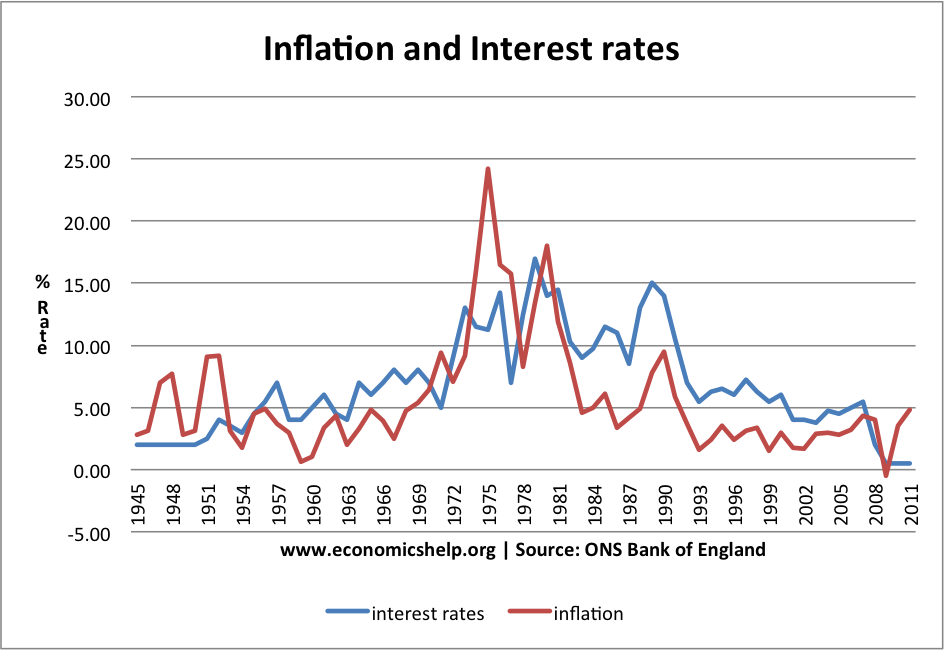

inflation-interest-rates-1945-2011.png (944×650) (economicshelp.org)

Base rates and bank interest rates - Economics Help

Interest payments are falling despite huge borrowing as a result of renewed bonds at very low rates. This is one of the reasons for keeping rates low. I can't see much of a rise in my lifetime. Inflation picked up a little around 2010 at 4% ?? but nothing was done.

UK Government Total Spending Chart Gallery (ukpublicspending.co.uk)

20 years to go up to the peak and another 20 years to go down. When you consider the rate moved from say 5% to 6% that's probably the equivalent of 0.25% up to 0.35% today. Hardly going to move up 1% a time ?. Then there's the cycle to consider. Never a straight line.

Federal Funds Rate - 62 Year Historical Chart | MacroTrends

1 -

coastline said:There is a link but it's now broken since the 2008 GFC. Base rates were used as a buffer against inflation, trying to slow things down , but worldwide governments are now running huge deficits and national debt.

Today we've just heard the UK borrowed £300bn in 2020-21 to cope with the pandemic and will borrow another £200bn this year 2021-22. It'll be loaded onto the national debt as ever but the bonus, that's if you can call it that , is it's borrowed at 0.8% which makes a huge difference.On top of that £303 billion that we have borrowed, you should add the £2,085 billion QE in 2020So years ago the Government would have increased interest rates, now they can bung some QE into the economy and Joe Public thinks that the economy is doing fine.

2 -

No chance. As you appear not to yet realize....the government can't afford higher interest rates so inflation will rip, wiping out savers with it while at the same time reducing the real cost of government debt. Welcome to MMT.jim8888 said:As I project forward into my retirement, I construct disaster scenarios in my head such as "What if inflation went to 10%"?

I remember mortgage interest rates being 14% at one point in the Nineties. I'd no savings or investments then but, I assume if I had, I'd have been earning 14% on those if I did have money in the bank.

I wondered, therefore, if inflation goes up by 5%, would you then assume a return on your investments would move up to, say, 9% to enable you to continue with a Safe Withdrawal Rate of 4% from your Direct Contribution pension fund?0 -

The Fed has shown a willingness to allow inflation to run free in the short term. A likely indication as to how other Central Banks will also use the tool to stabilise Government finances.1

-

When inflation reached 26% in 1975 , the best building society monthly savings accounts were paying around 9.75% interest per annum. Fresh money from salary each month had to be used to try to keep-up the value of saving accounts.

0 -

Commodities might be due a sustained rise, been in the doledrums for a long time now ? Relies on China growth to an extent I guess though...0

-

Inflation tends to benefit people in work with debt, as pay rises go up and the value of their house goes up, while their debt (mortgage) gets eroded. People with money and not in work lose out.1

-

If that is the case, its not appropriate to use a bar chart.Deleted_User said:lol no ... first, you seem to have got that £2,085bn figure by adding up the 3 different figures for QE in 2020. That's not what the figures mean. They are new figures for the total QE the BoE is planning to do since QE began (in 2009). So the last figure, £895bn in November 2020, means that's when they raised the target for total QE to date from £745bn to £895bn, meaning that at that point they decided to do an additional £150bn of QE. Which they then probably did gradually, not all in November. The total new QE carried out during the 2020-21 financial year was the best part of £300bn.

0

{kind=link}

{kind=link}

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards