We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Workplace pension transfer

Comments

-

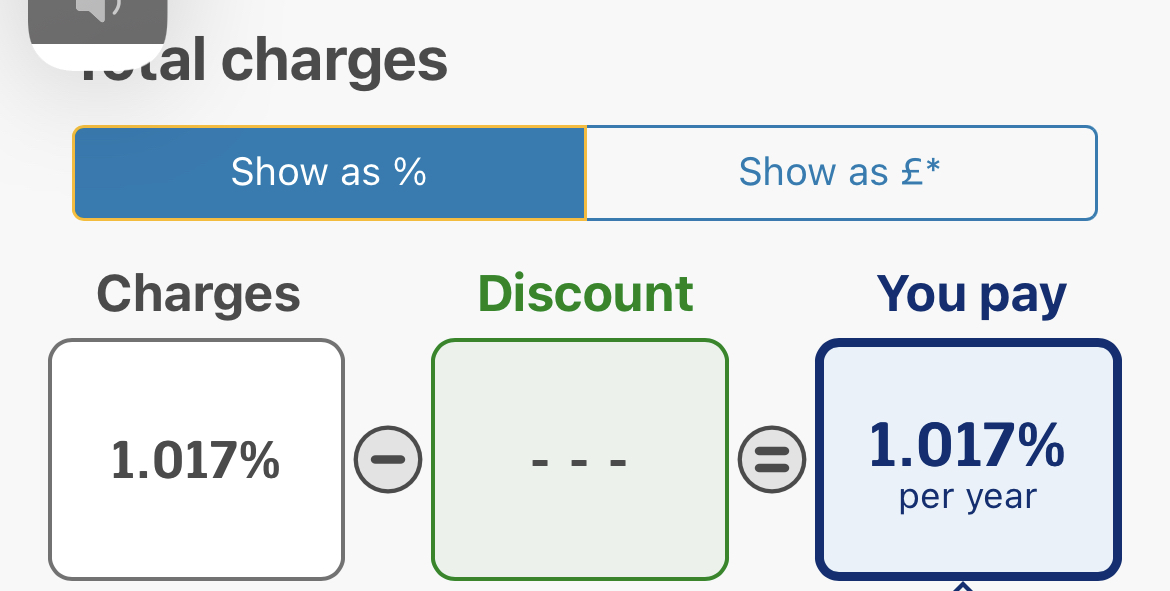

Usually, the SL pensions have riskier funds from the internal fund range (and a number of them are actually managed by Vanguard). Unless your employer has really cut the range down. I come across more SL workplace pensions at 0.3% p.a. than those at the maximum 0.75%.Nuggy96 said:I have chosen a different more risky fund than the default fund selected when I first joined the scheme I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0 -

Edit: Op disregard my post below, just noticed you already switched to an alternative fund within the SL pension scheme

")

Op I reviewed my pensions last year (with the help of this forum), my current employer uses SL and the standard/default funds performance was relatively poor. Rather than go through the hassle of a transfer (Ive done this before), I switched from the default option to a 100% Equities active fund...higher fees but the performance difference has been significant....it's a BNY Mellon fund if that matters. I am 39 hence not too concerned with the higher risk, obviously DYOR but might be another option to consider before pulling the trigger to transfer out.

I've transferred one old pension that was also with SL however I have another from my last employer that has been doing ok performance-wise and has some bonds and property funds exposure. Given the reasonable performance and diversification I'm leaving it alone so that I can run my LISA and Vanguard S&SISA at 100% Equities without the need to faff about and concern myself with bonds and allocation etc.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards