We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

PLEASE READ BEFORE POSTING: Hello Forumites! In order to help keep the Forum a useful, safe and friendly place for our users, discussions around non-MoneySaving matters are not permitted per the Forum rules. While we understand that mentioning house prices may sometimes be relevant to a user's specific MoneySaving situation, we ask that you please avoid veering into broad, general debates about the market, the economy and politics, as these can unfortunately lead to abusive or hateful behaviour. Threads that are found to have derailed into wider discussions may be removed. Users who repeatedly disregard this may have their Forum account banned. Please also avoid posting personally identifiable information, including links to your own online property listing which may reveal your address. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Help with mortgage

Comments

-

OP, this is incorrect.moneysavinghero said:Brokers are never free of charge. They want paying for what they do. Some may not charge you directly but will get a fee from the mortgage provider (who will of course accounted for this in the rates they give - this is why it is not always cheaper to go with a broker)

The procuration fee (commission) paid by the bank to the broker has no effect on the interest rate of the product.

Even if you go direct, you won't get a "discount" on the interest rate, the bank also has to incur costs to service your application, take on the risk of advice, etc.

0 -

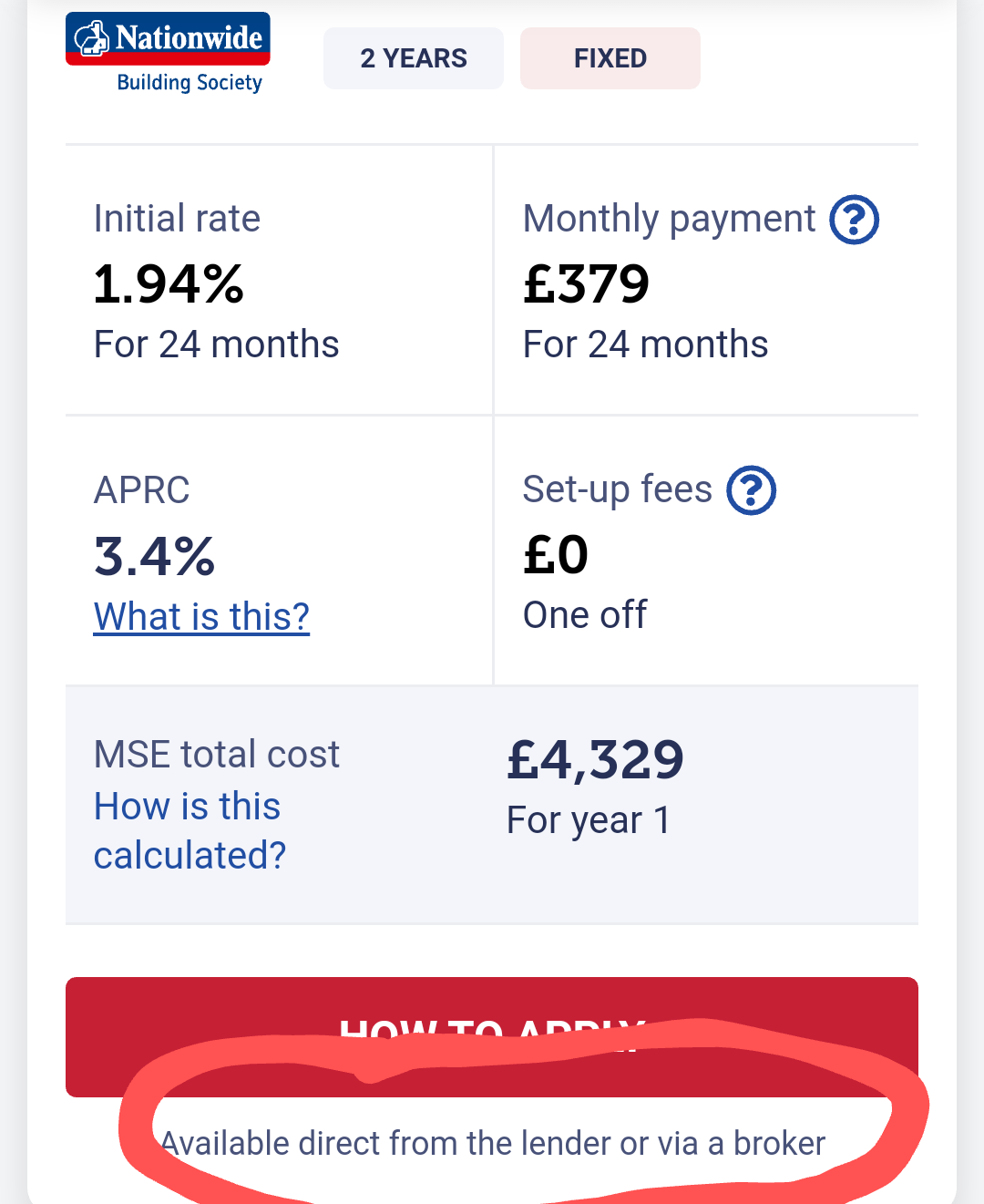

As Lonibra (one of the mortgage brokers that stalk this forum) shows, you can get exactly the same rate going direct with Nationwide as you get going through a broker. What the above doesn't show is whether said broker will be charging a direct fee to the consumer. No such thing as a free lunch in life - but will always be plenty of people making easy money selling 'free' lunches that will swear they are really are free.lonibra said:

OP, this is incorrect.moneysavinghero said:Brokers are never free of charge. They want paying for what they do. Some may not charge you directly but will get a fee from the mortgage provider (who will of course accounted for this in the rates they give - this is why it is not always cheaper to go with a broker)

The procuration fee (commission) paid by the bank to the broker has no effect on the interest rate of the product.

Even if you go direct, you won't get a "discount" on the interest rate, the bank also has to incur costs to service your application, take on the risk of advice, etc.

Bank has to incur costs wherever you go direct or not, but if you go via a 'free' broker they also have to incur the cost of the brokers fee.0 -

How to apply for DIP? I'm not looking for a big sum of money anyway as i don't want yo pay huge amount of money a month.moneysavinghero said:Firstly you need to get a Decision in Principle (DIP). This is the mortgage provider saying in theory they would be willing to lend you x sum of money. Once you know how much you can get a mortgage for you will know which houses are within your budget. The Estate Agent will likely also want to see your DIP before they allow you to view houses (they don't want to waste time showing houses to people who can never actually buy them). Once you have viewed a house you like just call up the Estate Agent and make your offer. Once your offer has been accepted then you apply for the full mortgage.

In your situation as you don't really know what you are doing it might be better to go with a broker who can hold your hand throughout the process.

The most confusing for me is, the process.

I'm not sure if i need first to apply for mortgage or find a property. And all other procedures.0 -

I'm also confused regarding fixed rate or initial one, what's the difference, and which one is the best to choose in long term?0

-

Initial rate may be a discount, but still variable.Will123321 said:I'm also confused regarding fixed rate or initial one, what's the difference, and which one is the best to choose in long term?

Fixed rate is... fixed, no matter what the variable rate does.

Which is better? Hold my crystal ball for me a second...0 -

I'm not a broker, but I know enough about mortgages to know that you don't get a discount on the rate by going direct, which is what you said. None of this is hidden, you can check the MSE mortgage finder to compare for yourself.moneysavinghero said:

As Lonibra (one of the mortgage brokers that stalk this forum) shows, you can get exactly the same rate going direct with Nationwide as you get going through a broker. What the above doesn't show is whether said broker will be charging a direct fee to the consumer. No such thing as a free lunch in life - but will always be plenty of people making easy money selling 'free' lunches that will swear they are really are free.lonibra said:

OP, this is incorrect.moneysavinghero said:Brokers are never free of charge. They want paying for what they do. Some may not charge you directly but will get a fee from the mortgage provider (who will of course accounted for this in the rates they give - this is why it is not always cheaper to go with a broker)

The procuration fee (commission) paid by the bank to the broker has no effect on the interest rate of the product.

Even if you go direct, you won't get a "discount" on the interest rate, the bank also has to incur costs to service your application, take on the risk of advice, etc.

Bank has to incur costs wherever you go direct or not, but if you go via a 'free' broker they also have to incur the cost of the brokers fee.

Are you saying that an 80% LTV purchase mortgage from Halifax/HSBC/Nationwide has a higher rate through a free broker (Habito, L&C, other MSE recommended free brokers) than if you went direct?0 -

If the whole thing is confusing you then maybe it is best that you find a mortgage broker. They will be able to get the DIP sorted for you. They will also advise you on anything else you need help with.

You could also get a DIP by visiting your chosen mortgage providers website and going through their application process.

Fixed Rate vs Variable rate.

FIXED: You know what rate you are going to pay for the length of the fix. Great if you are worried interest rates might rise, not so great if they fall

VARIABLE: The interest rate may change throughout the length of the mortgage. It could either go up or down depending on central bank decisions.

1 -

moneysavinghero said:If the whole thing is confusing you then maybe it is best that you find a mortgage broker. They will be able to get the DIP sorted for you. They will also advise you on anything else you need help with.

You could also get a DIP by visiting your chosen mortgage providers website and going through their application process.

Fixed Rate vs Variable rate.

FIXED: You know what rate you are going to pay for the length of the fix. Great if you are worried interest rates might rise, not so great if they fall

VARIABLE: The interest rate may change throughout the length of the mortgage. It could either go up or down depending on central bank decisions.

Example, if I'm based in London, but would like to buy property in an other city, where should i look for a broker?0 -

Any broker will do. They don't have be in the same city as the house is. If you really don't have a clue how to find a broker then you could find a property first and call up the estate agent to book a viewing - they would then probably direct you towards their in-house broker to get a DIP from them before continuing.1

-

Thanks. So first i need to see the property and if I like it, ask for DIP?moneysavinghero said:Any broker will do. They don't have be in the same city as the house is. If you really don't have a clue how to find a broker then you could find a property first and call up the estate agent to book a viewing - they would then probably direct you towards their in-house broker to get a DIP from them before continuing.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.5K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.6K Work, Benefits & Business

- 603K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards