We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

...Is the BTL proposition now dead?

Robwales

Posts: 67 Forumite

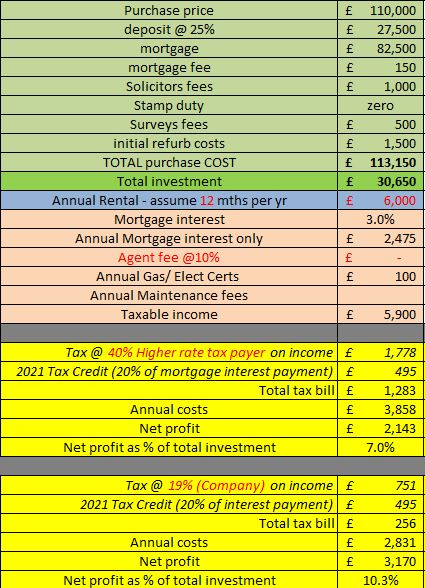

After talking to a collegue again this week who rents out several BTLs (and singing its virtues vs my pension + ISA portfoilio) i looked again at some (what i think are sensible) numbers for a £110k flat with a 25% mortgage @ 3% interest only

As said, i have tried to be sensible...so assumed 11 mths per anum rental rather than 12, and added costs for maintenance and agency

For a higher rate tax payer..it seems to drive a whopping £193 profit per year...0.6% rtn!? If it was set up via a limited company, it would be £1.2k...4% rtn.

Am i missing something?

i guess if i assumed full occupancy, and no maitenance costs and no agency involved + go via a limited company then its more viable - but then it isnt passive and isnt risk free:

0

Comments

-

I haven’t analysed your numbers, however what I will say is that if you’re not sure about it then don’t do it. If you were 100% sure then my advice would be to think twice, and only do it if you’re still sure.

For Higher Rate tax payers especially there are options that are far more tax efficient, with a lot less hassle.

If you’re looking for a debate on the pros and cons of BTL then bear in mind that this forum is very much anti BTL. Opinions on other forums will vary.

1 -

Are you assuming no capital gain or loss?

0 -

Think there is stamp duty to pay, no? You have to pay an extra 3% on what you would have paid were it a purchase for your main residence.

The whole thing's just not worth it in my book. Your £27,500 invested in the stock market might return you £2k/year on average without any of the hassle.0 -

Stamp duty won't be zero if it's a second home for BTL. There's a 3% tax (4% if you're in the People's Republic of Scotland).

0 -

yeah my mistake - i saw stamp duty was zero in wales for under 250k, but for a BTL property for £110k its 4% in Wales....so the numbers would be as follows:

PS

PS

i am not contemplating it seriously...i was just piqued by a mate saying how great the BTL rtn was, and my maths tell me a very different story and wanted to sanity check my logic on here!

I *suspect* they simply take the rent (full occupancy) and minus the interest only mortgage (and no other costs) and on the surface it looks OK1 -

As John464 says, your mate might be including asset appreciation on the property itself as part of their return too.

But, FWIW, I'm happy chucking my money at the stock markets instead which don't tend to call me in the middle of the night saying there's been a flood.2 -

Is anyone actually paying their rent at the moment?

1 -

BTL is about finding the right property to make the figures stack up. In the boom years the focus was on capital appreciation. The greatest danger now to BTL in the medium term is rising interest rates.

Nor have you made any provision for long term maintenance costs etc. Also an in built allowance if your are unfortunate enough to get the tenant from hell. Then there's the loss of income/additional expense when you decide to exit.3 -

Right now seems a bad moment if you are hoping for capital appreciation while renting. With Brexit + Covid + the Stamp Duty Holiday ending estate agents I have spoken to are expecting house prices to fall now as people feel insecure in their jobs.0

-

I think if you're a higher rate tax payer, then owning through a company is the most profitable route. I think where the money starts to mount is by having quite a few properties - because as you've calculates, I think the profit per property does tend to be quite low unless you've bought cheaply and done the property up. These are from my observations of friends with BTLs, no personal experience in the area.Statement of Affairs (SOA) link: https://www.lemonfool.co.uk/financecalculators/soa.phpFor free, non-judgemental debt advice, try: Stepchange or National Debtline. Beware fee charging companies with similar names.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards