We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Complicated House Buying Scenario!

Comments

-

@Thrugelmir Interest is no longer tax-deductible for BTLs in personal names. You get a "basic rate tax reduction" in its place.Thrugelmir said:

Wasn't clear from your post. Many people don't declare the income. Nor understand that only the interest element is tax deductible. So the real return is actually considerably lower if tax is factored in.About-time said:

How do you mean? Obviously we do pay tax on the rental income if that's what you're referring to?Thrugelmir said:

No mention of tax?About-time said:

That's what I wondered. It's never been a big money-spinner, but it used to contribute a steady £200-300 a month in rent after mortgage, insurance etc was paid for.K_S said:

@about-time It is unlikely to contribute towards affordability, especially given that you are currently living in the property. Is it mortgage-free, on a BTL interest-only mortgage or consent to let?About-time said:

Thank you for your reply, and I think you are right on this point - we could sell it, or keep it on as a rental, whichever works out best for us (and we're undecided) - I just wondered whether the monthly rent would contribute to the amount we can borrow on another mortgage, and whether a lender is likely to accept last year's statements as proof of rental income?K_S said:@About-time

1) Hard to comment without more detail. I wouldn't want to unknowingly mislead you one way or the other. Imho, whether to sell the property or not needn't necessarily be based on the ease of getting a resi mortgage.

https://www.gov.uk/government/publications/restricting-finance-cost-relief-for-individual-landlords/restricting-finance-cost-relief-for-individual-landlordsI am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

Amounts to the same thing. Other than relief is restricted to 20% not the taxpayers own highest rate of tax.K_S said:

@Thrugelmir Interest is no longer tax-deductible for BTLs in personal names. You get a "basic rate tax reduction" in its place.Thrugelmir said:

Wasn't clear from your post. Many people don't declare the income. Nor understand that only the interest element is tax deductible. So the real return is actually considerably lower if tax is factored in.About-time said:

How do you mean? Obviously we do pay tax on the rental income if that's what you're referring to?Thrugelmir said:

No mention of tax?About-time said:

That's what I wondered. It's never been a big money-spinner, but it used to contribute a steady £200-300 a month in rent after mortgage, insurance etc was paid for.K_S said:

@about-time It is unlikely to contribute towards affordability, especially given that you are currently living in the property. Is it mortgage-free, on a BTL interest-only mortgage or consent to let?About-time said:

Thank you for your reply, and I think you are right on this point - we could sell it, or keep it on as a rental, whichever works out best for us (and we're undecided) - I just wondered whether the monthly rent would contribute to the amount we can borrow on another mortgage, and whether a lender is likely to accept last year's statements as proof of rental income?K_S said:@About-time

1) Hard to comment without more detail. I wouldn't want to unknowingly mislead you one way or the other. Imho, whether to sell the property or not needn't necessarily be based on the ease of getting a resi mortgage.

https://www.gov.uk/government/publications/restricting-finance-cost-relief-for-individual-landlords/restricting-finance-cost-relief-for-individual-landlords0 -

@Thrugelmir Not really, they don't amount to the same thing.Thrugelmir said:

Amounts to the same thing. Other than relief is restricted to 20% not the taxpayers own highest rate of tax.K_S said:

@Thrugelmir Interest is no longer tax-deductible for BTLs in personal names. You get a "basic rate tax reduction" in its place.Thrugelmir said:

Wasn't clear from your post. Many people don't declare the income. Nor understand that only the interest element is tax deductible. So the real return is actually considerably lower if tax is factored in.About-time said:

How do you mean? Obviously we do pay tax on the rental income if that's what you're referring to?Thrugelmir said:

No mention of tax?About-time said:

That's what I wondered. It's never been a big money-spinner, but it used to contribute a steady £200-300 a month in rent after mortgage, insurance etc was paid for.K_S said:

@about-time It is unlikely to contribute towards affordability, especially given that you are currently living in the property. Is it mortgage-free, on a BTL interest-only mortgage or consent to let?About-time said:

Thank you for your reply, and I think you are right on this point - we could sell it, or keep it on as a rental, whichever works out best for us (and we're undecided) - I just wondered whether the monthly rent would contribute to the amount we can borrow on another mortgage, and whether a lender is likely to accept last year's statements as proof of rental income?K_S said:@About-time

1) Hard to comment without more detail. I wouldn't want to unknowingly mislead you one way or the other. Imho, whether to sell the property or not needn't necessarily be based on the ease of getting a resi mortgage.

https://www.gov.uk/government/publications/restricting-finance-cost-relief-for-individual-landlords/restricting-finance-cost-relief-for-individual-landlords

Relief is given as a reduction in tax liability instead of a reduction to taxable income. Erstwhile Basic rate tax payers could move into a higher rate tax band as a result of these changes with a range of knock-on effects from that.

https://www.rossmartin.co.uk/land-a-property/1948-restricting-mortgage-interest-relief-freeview

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

But does the fact that they are now living in their rental property not mean that that is their main residence? As I understood it, they had sold their main residence to move into their rental, which now becomes their main residence? I'm not educated enough to know for certain, but it strikes me they may get hit for the extra stamp duty on this basis?K_S said:Windofchange said:Surely the solution is to sell the rental, clear all your debts, have a larger deposit (depending on what equity you had in the rental) and buy a larger main residence? With all the recent changes in tax on rentals, was it really making you much money anyway? The other consideration is that if you hold onto the rental, you will be liable for the extra stamp duty as you will have two properties on completion of whatever new house you buy. Depending on which part of the country etc, this could be a significant sum of money. Does it really sense to keep holding it?@windofchange They just sold their main residence, and so can use the main residence exemption to escape the 3% (in England) surcharge. That applies irrespective of the number of additional properties in the background.

We went through this last year, admittedly though with a rental. We rented our main residence and also owned a second property. When we brought the house we are in now to replace the rental property as our main residence, we got stung with the higher stamp duty because we would own two properties. Our solicitor was having none of it in terms of us having replaced our main residence. Luckily the stamp duty holiday came along to save the day so we ended up paying what we would have done if we just had the one property, but seems the OP may be liable?1 -

@windofchange That's a good point.

As I understand it, the previous main residence will be considered as such if it was at some point during a period of 3 years before the purchase.

But this is just my interpretation of the guidance, might well be wrong. I'm not an SDLT expert by any stretch.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

They will probably be able to get past the 'main residence' point on this basis:"Merely occupying a property will not in itself make it a main residence. There needs to be a permanence and expectation of continuation to the occupation to establish it as a main residence. "So as long as they don't stay there too long they should be OK.Obviously the other elephant in the room is that living in your own Buy-to-Let is not usually allowed by the lenders so hopefully they have given approval for this occupation, and similarly the house insurance may not be properly covering them while it is not actually rented to a 3rd party, and of course the longer they stay there the older their proof of income from the property becomes.On the flip-side, if they do intend to sell the rental property they should not assume that their current occupation will necessarily allow them to avoid CGT on its sale by seeking to consider it as their 'main residence'.Should take advice on that point...

0 -

Probably something to take professional advice on then? As I say, when we went through this last year the advice from our solicitor was very black and white - if you have a home already that you are occupying then that is your main residence whether you are renting there temporarily or are an owner occupier. Depending on which bit of the country the OP is looking at, it may / may not make much difference, but assuming an average house price of 256k ish then it will be a nasty sting if it does apply, and may then influence quite heavily the decision about what to do with the rental property in my view.0

-

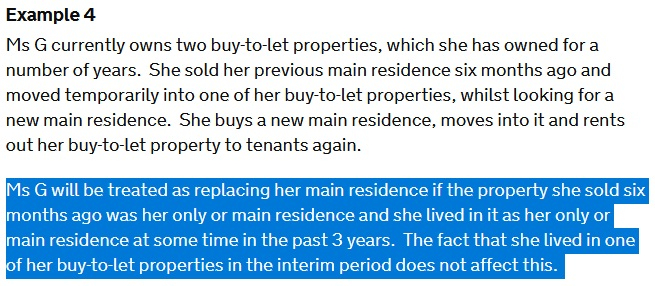

Windofchange said:Probably something to take professional advice on then? As I say, when we went through this last year the advice from our solicitor was very black and white - if you have a home already that you are occupying then that is your main residence whether you are renting there temporarily or are an owner occupier. Depending on which bit of the country the OP is looking at, it may / may not make much difference, but assuming an average house price of 256k ish then it will be a nasty sting if it does apply, and may then influence quite heavily the decision about what to do with the rental property in my view.@windofchange Tbf conveyancers aren't always SDLT experts. The advice you were given re the part about renting in between is most definitely questionable as I have seen at least 2 cases of clients (who also own rental/second properties) who moved into private rentals between house purchases to be chain free and didn't pay the 3% surchage on their onward purchase.Edit: Same scenario as OP's from the gov.uk SDLT pages https://www.gov.uk/hmrc-internal-manuals/stamp-duty-land-tax-manual/sdltm09810

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

Not all solicitors are good on the subtleties of SDLT and prefer a simple life so will err on the side of paying it if in any doubt, this is where the roving band of specialist firms make money by appealing cases where it has unnecessarily been paid.Similarly a solicitor is not always a great place for CGT advice.The advice given of "if you have a home already that you are occupying then that is your main residence whether you are renting there temporarily or are an owner occupier" seems to be wrong in both directions, it takes more to establish a property as a main residence than simply temporary occupation if you want to establish that for CGT purposes, and it isn't enough on its own if you didn't want to establish it as your 'main residence' for SDLT purposes.Advice is good, but hopefully better advice than that.

1 -

Interesting. I might delve into this a bit further then as it would be a tidy sum of money to get back. We had been renting for a number of years in various properties, and the other property that my partner was gifted by her family has been held under her name for about 5 years. Our main residence was the rented property that we had been in for two years, and we then brought the house that we are currently in. My hope at the time was definitely that the purchased property would replace our rental as a main residence, therefore avoiding the extra stamp duty, but as I said, the solicitor was having none of it. In terms of getting a definitive answer, can I just raise this with HMRC and see what they say, or do I need to employ some sort of service who will no doubt take 25% or whatever as their payment?K_S said:Windofchange said:Probably something to take professional advice on then? As I say, when we went through this last year the advice from our solicitor was very black and white - if you have a home already that you are occupying then that is your main residence whether you are renting there temporarily or are an owner occupier. Depending on which bit of the country the OP is looking at, it may / may not make much difference, but assuming an average house price of 256k ish then it will be a nasty sting if it does apply, and may then influence quite heavily the decision about what to do with the rental property in my view.@windofchange Tbf conveyancers aren't always SDLT experts. The advice you were given re the part about renting in between is most definitely questionable as I have seen at least 2 cases of clients (who also own rental/second properties) who moved into private rentals between house purchases to be chain free and didn't pay the 3% surchage on their onward purchase.Edit: Same scenario as OP's from the gov.uk SDLT pages https://www.gov.uk/hmrc-internal-manuals/stamp-duty-land-tax-manual/sdltm09810

I think the distinction made at the time was we had never owned a property as a main residence, therefore couldn't include it as such. We hadn't sold something, rented something in the meantime and then brought again.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards