We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Transferring out of Defined Benefit pension

Comments

-

True Potential's Portfolio Funds launched fully financed in Nov '15 - obviously with a full suite of investments.

If anyone can explain to me how a new investment fund comes to market as a fully fledged proposition, I should be grateful.

0 -

First of all, in most jurisdictions advisers are not allowed to claim that they would “ deliver a higher return”. Promising higher returns is a major red flag. Good reason for that. Anyone talking to an adviser like that should run.AlanP_2 said:

I thought the point was a repsonse to the question posed by Mickey66 - "No doubt the IFA will argue that their management would result in a higher return, but would it really? I guess that's the bet."Deleted_User said:

What exactly is the point of a plot comparing a bad fund against one carefully selected IFA’s portfolios? Why not put AMZN returns on the same plot and conclude that everyone should just buy Amazon?dunstonh said:I understand there will be a one-off IFA fee because of the need to get formal advice for such a move, but after that I see no reason for further on-going fees.If the OP no longer requires advice and is using investments that dont require ongoing adjustments then there is no need for ongoing servicing.

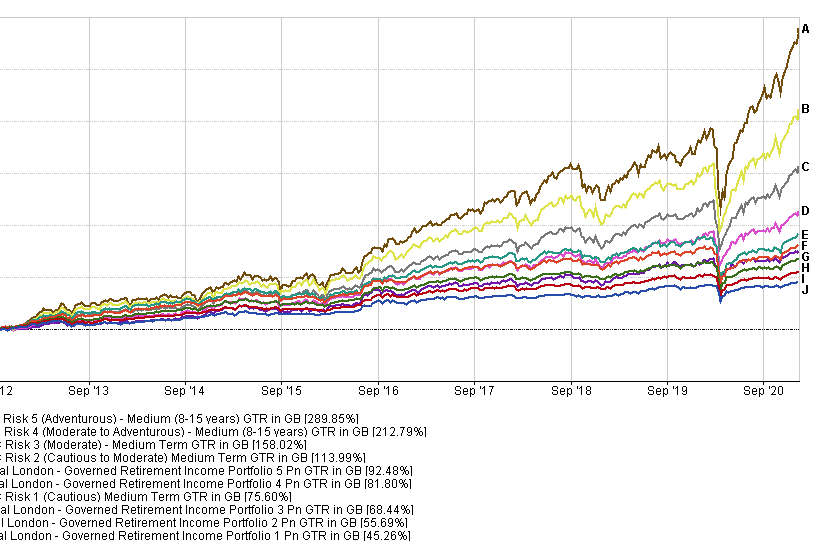

If the OP is using an investment portfolio that the IFA controls then the IFA is the one being paid to rebalance and adjust.Why not just put the £800k into a managed fund with drawdown?That is a possible scenario. However, why not just put the £800k into a managed portfolio with drawdown? It can be cheaper. it can be more expensive. It can have higher returns than a single managed fund. It may end up with lower returns but that is a choice someone makes.Eg, Royal London annual fee for that amount of money would be around 0.35% pa. The fund would only have to increase by 1.75% pa to return the £14k alternative of not transferring the money, which seems fairly safe to me.This is the problem with putting charge before the investments. With that mindset you would never invest at all but leave the whole lot in cash as its cheaper. (actually, it's not historically. It's just that you cant see the charges with cash savings)No doubt the IFA will argue that their management would result in a higher return, but would it really? I guess that's the bet.Nothing is guaranteed but it hasn't been that difficult to beat historically. below is chart that shows RLs 5 risk profiles for drawdown. And 5 real IFA portfolios (no hindsight - these are actual).

As mentioned on your own threads, RL is cheap and simple but you shouldn't expect much more than middle of the road in respect of returns.The implication that IFA will deliver above average returns, and that you get better returns by paying more = marketing á-la dodgy car salesman.

OK, Dunston isn't the specific IFA referenced but a reasoned, evidenced repsonse seems reasonable to me.Secondly, picking an arbitrary set of investments and putting them on a plot over an arbitrary period of time is always designed to mislead. There are many thousands of investment vehicles and advisers out there. You get thousands of monkeys to pick investments, a few will outperform Royal London over some periods (which isn’t great to start with).Quoting returns over an 8 year time frame is another red flag. Fund managers used to be famous for carefully picking starting points for their comparisons (and forgetting to mention all their funds that have failed).On top of that, proper meaningful analysis needs to be independently peer reviewed. For a good reason.There can be no other purpose to pick arbitrary investments and put them on an 8 year plot than to mislead.1 -

It is treated as a global equity fund though rather than a multi-asset fund. But it is a global managed fund. I bet many of those using VLS100 would refer to it as a tracker though. It's not a very good global fund either. Q4 in 2020, Q3 in 2019. Even cumulatively it is Q3 over most periods. There is nothing about VLS100 that makes it stand out against alternatives.zagfles said:

The point of VLS100 is that it isn't a global tracker. Those who constantly bang on about global trackers doing better and being cheaper are missing the point. It's "active" in so far as selection of the underlying passives to use.dunstonh said:Has anyone actually said that? Maybe someone on my ignore list did. Bog standard global trackers have beaten VLS100, as discussed here a lot. I have. It's hardly an achievement.VLS100 is the least effective VLS fund. I am sure it's only there for completeness. Although considering the large amount of money in that fund, it is clear that it appeals to some instead of a global tracker.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0 -

dunstonh said:

It is treated as a global equity fund though rather than a multi-asset fund. But it is a global managed fund. I bet many of those using VLS100 would refer to it as a tracker though. It's not a very good global fund either. Q4 in 2020, Q3 in 2019. Even cumulatively it is Q3 over most periods. There is nothing about VLS100 that makes it stand out against alternatives.zagfles said:

The point of VLS100 is that it isn't a global tracker. Those who constantly bang on about global trackers doing better and being cheaper are missing the point. It's "active" in so far as selection of the underlying passives to use.dunstonh said:Has anyone actually said that? Maybe someone on my ignore list did. Bog standard global trackers have beaten VLS100, as discussed here a lot. I have. It's hardly an achievement.VLS100 is the least effective VLS fund. I am sure it's only there for completeness. Although considering the large amount of money in that fund, it is clear that it appeals to some instead of a global tracker.

Of course it's a global managed fund, and not multi-asset, the clue is the 100 (ie 100% equities). It uses underlying trackers so some may refer to it as a "tracker", so what? Genuine global trackers are >50% US, IMO not very well diversified even if genuinely representative of global market cap. And as we all know, US stocks have done much better than UK over the last few years so a fund with a US bias will likely have beaten a fund with UK bias. History might repeat itself, or it might not and the UK may outperform the US over the next few years.1 -

Yes, the recency bias often drives people to take returns of funds with different allocations and to translate Q4 or Q3 ranking into “this is important for selecting investments”. If you want to take issue with VLS allocation to Britain, you need to challenge their white paper on the subject rather than some meaningless numbers from 2019 and 2020.dunstonh said:

It is treated as a global equity fund though rather than a multi-asset fund. But it is a global managed fund. I bet many of those using VLS100 would refer to it as a tracker though. It's not a very good global fund either. Q4 in 2020, Q3 in 2019. Even cumulatively it is Q3 over most periods. There is nothing about VLS100 that makes it stand out against alternatives.zagfles said:

The point of VLS100 is that it isn't a global tracker. Those who constantly bang on about global trackers doing better and being cheaper are missing the point. It's "active" in so far as selection of the underlying passives to use.dunstonh said:Has anyone actually said that? Maybe someone on my ignore list did. Bog standard global trackers have beaten VLS100, as discussed here a lot. I have. It's hardly an achievement.VLS100 is the least effective VLS fund. I am sure it's only there for completeness. Although considering the large amount of money in that fund, it is clear that it appeals to some instead of a global tracker.

Here is another example... Fidelity Growth Strategies Fund (FDEGX) returned 40% in 2019 (vs 32% for the category, top quartile). It returned 30% in 2020. Not bad. Also, it was the worst US fund for the decade ending in 2010 (67% loss). An IFA ought to know that past performance over a couple of years does not make a fund either good or bad.

1 -

Ask yourselves why are nearly all the common active funds held by retail investors today been around for the last 10-15 years only? Only a handful of the common ones have been around for more than 20 years.Then ask yourselves why that may be. It is because retail investors chase performance and move onto the next out-performer. And you get different actives performing differently during different periods - no style ever continues to out-perform. The problem is you can not buy past returns and you can not easily make back "lost returns" in the original active fund. Thus, a passive index tracker should form at least the core for any retail investor.And its not just advisable to stick to a tracker directly due to long term performance. It is to prevent adverse behaviour by retail investors that would otherwise be detrimental to returns. There is a lot of value in that.1

-

Thus, a passive index tracker should form at least the core for any retail investor.I go along with that. Although that is because its the method I use. Also, if you look at the propositions from firms that have active, passive and hybrid (both) you do tend to find the hybrid is the best in terms of returns.And its not just advisable to stick to a tracker directly due to long term performance.

If that is your strategy and you want discrete mid table consistency then that is fine.

t is to prevent adverse behaviour by retail investors that would otherwise be detrimental to returns.This comes down to the knowledge and understanding of the investor. If you have a twitchy investor that moves about on a whim then they shouldn't really be near passives or managed. They should just get in a multi-asset fund and leave the decision making well alone.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0 -

From another point of view I am not exactly sure why anyone would recommend Vanguard Life Strategy over its peers. I certainly don't.Deleted_User said:

Yes, the recency bias often drives people to take returns of funds with different allocations and to translate Q4 or Q3 ranking into “this is important for selecting investments”. If you want to take issue with VLS allocation to Britain, you need to challenge their white paper on the subject rather than some meaningless numbers from 2019 and 2020.dunstonh said:

It is treated as a global equity fund though rather than a multi-asset fund. But it is a global managed fund. I bet many of those using VLS100 would refer to it as a tracker though. It's not a very good global fund either. Q4 in 2020, Q3 in 2019. Even cumulatively it is Q3 over most periods. There is nothing about VLS100 that makes it stand out against alternatives.zagfles said:

The point of VLS100 is that it isn't a global tracker. Those who constantly bang on about global trackers doing better and being cheaper are missing the point. It's "active" in so far as selection of the underlying passives to use.dunstonh said:Has anyone actually said that? Maybe someone on my ignore list did. Bog standard global trackers have beaten VLS100, as discussed here a lot. I have. It's hardly an achievement.VLS100 is the least effective VLS fund. I am sure it's only there for completeness. Although considering the large amount of money in that fund, it is clear that it appeals to some instead of a global tracker.

Here is another example... Fidelity Growth Strategies Fund (FDEGX) returned 40% in 2019 (vs 32% for the category, top quartile). It returned 30% in 2020. Not bad. Also, it was the worst US fund for the decade ending in 2010 (67% loss). An IFA ought to know that past performance over a couple of years does not make a fund either good or bad.0 -

Its one of many reasonable options out there. Certainly a solid choice. Why? Because it offersPrism said:

From another point of view I am not exactly sure why anyone would recommend Vanguard Life Strategy over its peers. I certainly don't.Deleted_User said:

Yes, the recency bias often drives people to take returns of funds with different allocations and to translate Q4 or Q3 ranking into “this is important for selecting investments”. If you want to take issue with VLS allocation to Britain, you need to challenge their white paper on the subject rather than some meaningless numbers from 2019 and 2020.dunstonh said:

It is treated as a global equity fund though rather than a multi-asset fund. But it is a global managed fund. I bet many of those using VLS100 would refer to it as a tracker though. It's not a very good global fund either. Q4 in 2020, Q3 in 2019. Even cumulatively it is Q3 over most periods. There is nothing about VLS100 that makes it stand out against alternatives.zagfles said:

The point of VLS100 is that it isn't a global tracker. Those who constantly bang on about global trackers doing better and being cheaper are missing the point. It's "active" in so far as selection of the underlying passives to use.dunstonh said:Has anyone actually said that? Maybe someone on my ignore list did. Bog standard global trackers have beaten VLS100, as discussed here a lot. I have. It's hardly an achievement.VLS100 is the least effective VLS fund. I am sure it's only there for completeness. Although considering the large amount of money in that fund, it is clear that it appeals to some instead of a global tracker.

Here is another example... Fidelity Growth Strategies Fund (FDEGX) returned 40% in 2019 (vs 32% for the category, top quartile). It returned 30% in 2020. Not bad. Also, it was the worst US fund for the decade ending in 2010 (67% loss). An IFA ought to know that past performance over a couple of years does not make a fund either good or bad.

a) simplicity

b) reputable provider with trillions in assets under management

c) better diversification than the other “fund of funds” options available in Britain

d) well justified choices for bonds (although not VLS 100) and well justified home bias.For various reasons its not my choice but there are lots of good reasons to recommend it.4 -

dunstonh said:Thus, a passive index tracker should form at least the core for any retail investor.I go along with that. Although that is because its the method I use. Also, if you look at the propositions from firms that have active, passive and hybrid (both) you do tend to find the hybrid is the best in terms of returns.And its not just advisable to stick to a tracker directly due to long term performance.

If that is your strategy and you want discrete mid table consistency then that is fine.

t is to prevent adverse behaviour by retail investors that would otherwise be detrimental to returns.This comes down to the knowledge and understanding of the investor. If you have a twitchy investor that moves about on a whim then they shouldn't really be near passives or managed. They should just get in a multi-asset fund and leave the decision making well alone.

You are an IFA. You would say all this. Your opinion will always be biased about these matters.

0

![[Deleted User]](https://us-noi.v-cdn.net/6031891/uploads/defaultavatar/nFA7H6UNOO0N5.jpg)

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards