We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Transferring out of Defined Benefit pension

Comments

-

They probably wouldn't as it's not likely to be in their interests. Bear in mind that they might be more inclined to offer you a lower fee for the transfer advice if they think they'll retain you as an ongoing client paying them 0.75% of your portfolio every year. So might be worth considering moving to whatever they're advising, then once in DC you are free to move out to whatever you want then. Check for any transfer out fees etc.wiimixer said:And can anyone recommend a Defined Benefit Pension Transfer Advisor who could help me transfer into a VanguardLifeStrategy fund? (should that be what I decide to do)

0 -

I think some people have ongoing advice , let the IFA set the portfolio up and explain their reasons, and then after a suitable period of time , go it alone using the same/similar portfolio.0

-

Once again, thanks to all respondents. I've had fresh conversations with a couple more IFAs, and both (independently) explained how the 'DB transfer market' has changed significantly since October. The advisor is apparently now very much more 'on the hook' for inappropriate advice, leading to a hike in their indemnity costs etc. Hence, through their retained services they're trying to cover a large (but not unreasonable) fee, whilst demonstrating interest/involvement with their clients.

I'm as cynical as the next man, but the way it was explained chimes with the attitude of the IFA I initially approached - so I'm inclined to pursue with them, and possibly look to reduce costs by finding a well performing fund with low management costs - e.g. Vanguard. As my retained IFA, I figure they should be happy to discuss financially beneficial options!?0 -

What exactly is the point of a plot comparing a bad fund against one carefully selected IFA’s portfolios? Why not put AMZN returns on the same plot and conclude that everyone should just buy Amazon?dunstonh said:I understand there will be a one-off IFA fee because of the need to get formal advice for such a move, but after that I see no reason for further on-going fees.If the OP no longer requires advice and is using investments that dont require ongoing adjustments then there is no need for ongoing servicing.

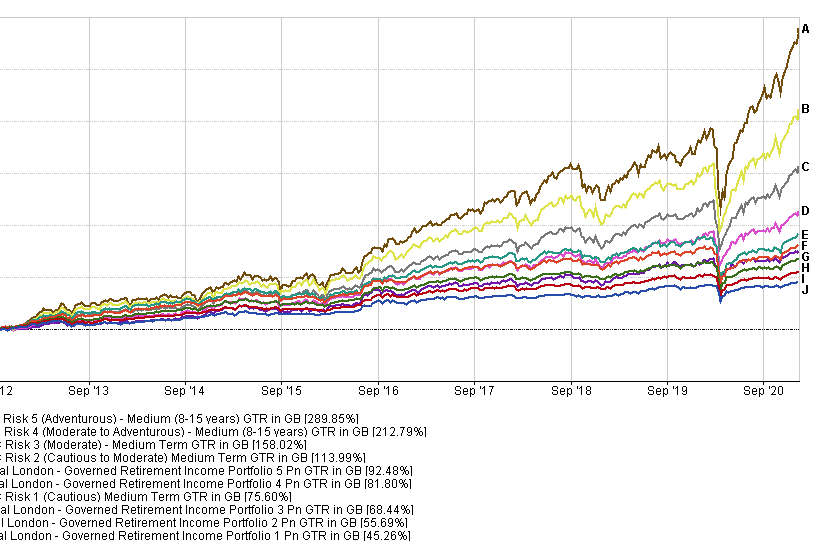

If the OP is using an investment portfolio that the IFA controls then the IFA is the one being paid to rebalance and adjust.Why not just put the £800k into a managed fund with drawdown?That is a possible scenario. However, why not just put the £800k into a managed portfolio with drawdown? It can be cheaper. it can be more expensive. It can have higher returns than a single managed fund. It may end up with lower returns but that is a choice someone makes.Eg, Royal London annual fee for that amount of money would be around 0.35% pa. The fund would only have to increase by 1.75% pa to return the £14k alternative of not transferring the money, which seems fairly safe to me.This is the problem with putting charge before the investments. With that mindset you would never invest at all but leave the whole lot in cash as its cheaper. (actually, it's not historically. It's just that you cant see the charges with cash savings)No doubt the IFA will argue that their management would result in a higher return, but would it really? I guess that's the bet.Nothing is guaranteed but it hasn't been that difficult to beat historically. below is chart that shows RLs 5 risk profiles for drawdown. And 5 real IFA portfolios (no hindsight - these are actual).

As mentioned on your own threads, RL is cheap and simple but you shouldn't expect much more than middle of the road in respect of returns.The implication that IFA will deliver above average returns, and that you get better returns by paying more = marketing á-la dodgy car salesman.2 -

It is true that the DB transfer market has got more difficult and there are numerous threads on this forum about it . Many people struggle to find a Pension Transfer Specialist at all .wiimixer said:Once again, thanks to all respondents. I've had fresh conversations with a couple more IFAs, and both (independently) explained how the 'DB transfer market' has changed significantly since October. The advisor is apparently now very much more 'on the hook' for inappropriate advice, leading to a hike in their indemnity costs etc. Hence, through their retained services they're trying to cover a large (but not unreasonable) fee, whilst demonstrating interest/involvement with their clients.

I'm as cynical as the next man, but the way it was explained chimes with the attitude of the IFA I initially approached - so I'm inclined to pursue with them, and possibly look to reduce costs by finding a well performing fund with low management costs - e.g. Vanguard. As my retained IFA, I figure they should be happy to discuss financially beneficial options!?

I would not be too starry eyed about Vanguard Life Strategy funds . There are similar funds that are cheaper and have performed better recently ( no guarantee of course this will continue ) such as HSBC global strategy funds; Legal and General Multi Index funds ; Fidelity Multi Allocator funds and Blackrock MY Map funds.0 -

Thanks Albemarle. I'm happy that through this forum I now have a range of funds to raise with the IFA and see how they stack up against the ones on offer.0

-

The focus on recent performance isn’t a good way of approaching it.One needs to invest a bit of time in designing an appropriate asset allocation. Then pick a good vehicle(s) to implement.And yes, cost is important because its the only thing impacting future performance which is certain.Recent performance is only meaningful in the context of checking that the fund/portfolio performed during major events as you expected it would. Otherwise its a bad criterion, although apparently favoured by IFAs.Multi-asset funds overweight in Britain underperformed a bit because... Well, Brexit. And US outperformed the world; by having more UK you have less Amazon and Tesla. That tells us zero about the future. Being a little overweight in the home market makes sense.1

-

I thought the point was a repsonse to the question posed by Mickey66 - "No doubt the IFA will argue that their management would result in a higher return, but would it really? I guess that's the bet."Deleted_User said:

What exactly is the point of a plot comparing a bad fund against one carefully selected IFA’s portfolios? Why not put AMZN returns on the same plot and conclude that everyone should just buy Amazon?dunstonh said:I understand there will be a one-off IFA fee because of the need to get formal advice for such a move, but after that I see no reason for further on-going fees.If the OP no longer requires advice and is using investments that dont require ongoing adjustments then there is no need for ongoing servicing.

If the OP is using an investment portfolio that the IFA controls then the IFA is the one being paid to rebalance and adjust.Why not just put the £800k into a managed fund with drawdown?That is a possible scenario. However, why not just put the £800k into a managed portfolio with drawdown? It can be cheaper. it can be more expensive. It can have higher returns than a single managed fund. It may end up with lower returns but that is a choice someone makes.Eg, Royal London annual fee for that amount of money would be around 0.35% pa. The fund would only have to increase by 1.75% pa to return the £14k alternative of not transferring the money, which seems fairly safe to me.This is the problem with putting charge before the investments. With that mindset you would never invest at all but leave the whole lot in cash as its cheaper. (actually, it's not historically. It's just that you cant see the charges with cash savings)No doubt the IFA will argue that their management would result in a higher return, but would it really? I guess that's the bet.Nothing is guaranteed but it hasn't been that difficult to beat historically. below is chart that shows RLs 5 risk profiles for drawdown. And 5 real IFA portfolios (no hindsight - these are actual).

As mentioned on your own threads, RL is cheap and simple but you shouldn't expect much more than middle of the road in respect of returns.The implication that IFA will deliver above average returns, and that you get better returns by paying more = marketing á-la dodgy car salesman.

OK, Dunston isn't the specific IFA referenced but a reasoned, evidenced repsonse seems reasonable to me.2 -

Deleted_User said:The focus on recent performance isn’t a good way of approaching it.One needs to invest a bit of time in designing an appropriate asset allocation. Then pick a good vehicle(s) to implement.And yes, cost is important because its the only thing impacting future performance which is certain.Recent performance is only meaningful in the context of checking that the fund/portfolio performed during major events as you expected it would. Otherwise its a bad criterion, although apparently favoured by IFAs.

It seems to me that it isn't IFAs that focus on performance (as in returns), as per this comment from ZPZ:

2) Should be your major consideration. Your investment journey is likely to be a long run and your choices will almost certainly impact the ongoing value by six figures quite soon. For example, if your adviser had ushered you into True Potential three years ago, instead of a popular benchmark like VanguardLifestrategy - your portfolio would be adrift a minimum of £80,000 already, on any of either's five risk profiles. In fact, TP's agressive portfolio has performed worse than VL20.

This deficit would be aside from on-going fees.

So would you see one of the TP portfolios as a better option than one of the VLS (or competitor) options based on perfromance as in excpected behaviour? Sounds to me like you would as the if the TP option is expected to underperform VLS and it goes on to actually underperform then it meets your criteria.

Returns must be a factor you consider otherwise every poor fund would be deleivering what was expected of it and thus a good candidate for inclusion in your portfolio/0 -

Investment management is commoditised. Anyone relying on selling superior performance has got a limited shelf life, IMO.AlanP_2 said:

I thought the point was a repsonse to the question posed by Mickey66 - "No doubt the IFA will argue that their management would result in a higher return, but would it really? I guess that's the bet."Deleted_User said:

What exactly is the point of a plot comparing a bad fund against one carefully selected IFA’s portfolios? Why not put AMZN returns on the same plot and conclude that everyone should just buy Amazon?dunstonh said:I understand there will be a one-off IFA fee because of the need to get formal advice for such a move, but after that I see no reason for further on-going fees.If the OP no longer requires advice and is using investments that dont require ongoing adjustments then there is no need for ongoing servicing.

If the OP is using an investment portfolio that the IFA controls then the IFA is the one being paid to rebalance and adjust.Why not just put the £800k into a managed fund with drawdown?That is a possible scenario. However, why not just put the £800k into a managed portfolio with drawdown? It can be cheaper. it can be more expensive. It can have higher returns than a single managed fund. It may end up with lower returns but that is a choice someone makes.Eg, Royal London annual fee for that amount of money would be around 0.35% pa. The fund would only have to increase by 1.75% pa to return the £14k alternative of not transferring the money, which seems fairly safe to me.This is the problem with putting charge before the investments. With that mindset you would never invest at all but leave the whole lot in cash as its cheaper. (actually, it's not historically. It's just that you cant see the charges with cash savings)No doubt the IFA will argue that their management would result in a higher return, but would it really? I guess that's the bet.Nothing is guaranteed but it hasn't been that difficult to beat historically. below is chart that shows RLs 5 risk profiles for drawdown. And 5 real IFA portfolios (no hindsight - these are actual).

As mentioned on your own threads, RL is cheap and simple but you shouldn't expect much more than middle of the road in respect of returns.The implication that IFA will deliver above average returns, and that you get better returns by paying more = marketing á-la dodgy car salesman.

OK, Dunston isn't the specific IFA referenced but a reasoned, evidenced repsonse seems reasonable to me.

(But please don't confuse investment management with paying someone to stop you making suboptimal decision (chasing performance etc) - two very different things).2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards