We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Paying back a loan after death

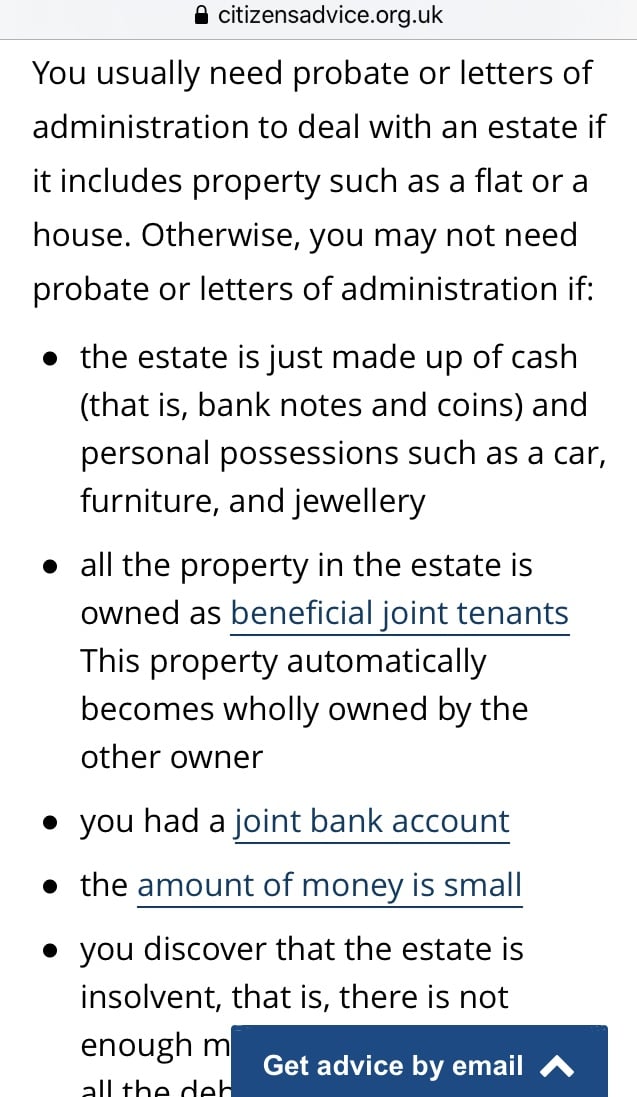

My father in law recently died. No probate was needed as he only had a joint bank account and the house was jointly owned with his wife.

He had taken out a personal loan from M&S in his name a couple of years ago. It was paid into the joint account, and payments were taken out of the joint account, but the loan was only in his name.

M&S have now cancelled the repayments upon hearing of his death and asked for the balance to be paid in full from the estate.

Is my mother in law responsible for paying this back when there was no probate and therefore no estate as such? I know morally she should, but she has no income of her own, as they lived off of my father in laws pension, his attendance allowance, and her carers allowance, all of which have now been stopped. She would struggle to pay this back even with a payment plan.

I’d appreciate any advice. Thanks!

He had taken out a personal loan from M&S in his name a couple of years ago. It was paid into the joint account, and payments were taken out of the joint account, but the loan was only in his name.

M&S have now cancelled the repayments upon hearing of his death and asked for the balance to be paid in full from the estate.

Is my mother in law responsible for paying this back when there was no probate and therefore no estate as such? I know morally she should, but she has no income of her own, as they lived off of my father in laws pension, his attendance allowance, and her carers allowance, all of which have now been stopped. She would struggle to pay this back even with a payment plan.

I’d appreciate any advice. Thanks!

0

Comments

-

Were they joint tenants or tenants in common?Pine said:No probate was needed as he only had a joint bank account and the house was jointly owned with his wife.

https://www.thisismoney.co.uk/money/cardsloans/article-1689651/Does-my-uncles-debt-die-with-him.html

0 -

Thank you for your reply. They were joint tenants.0

-

Sorry for your loss - did FiL have any assets in his own name - savings, Premium Bonds, ISA, Life policies?

Mother in law does not have to pay the loan from her own monies - only the estate of the deceased can a claim be made.

It probably will depend on the amount outstanding but if there are no monies to pay the loan then M&S will have to write it off, for a small amount I cannot see them putting a charge on the property.0 -

Thank you for your reply. He didn’t have any savings or insurance policies in his own name. He had a private pension but we have checked and it does not come with any death benefits. Their shared car was in his name - could she be forced to sell that? The amount outstanding on the loan is approx £2000.0

-

I would not think that the car would need to be sold.Pine said:Thank you for your reply. He didn’t have any savings or insurance policies in his own name. He had a private pension but we have checked and it does not come with any death benefits. Their shared car was in his name - could she be forced to sell that? The amount outstanding on the loan is approx £2000.

Whoever is dealing with the estate as administrator needs to write to M&S loans advising them that the estate has no funds to pay the loan. If all goes well that should be the end of the matter.0 -

The car form part of his estate and any assets in his estate should be used to repay any debts in his estate.Pine said:Thank you for your reply. He didn’t have any savings or insurance policies in his own name. He had a private pension but we have checked and it does not come with any death benefits. Their shared car was in his name - could she be forced to sell that? The amount outstanding on the loan is approx £2000.Are you positive probate is not required because we’ve now got a car that was solely in his name.1 -

How much is the car worth? Is there any outstanding finance on the car?Indecision is the key to flexibility

") 0

0 -

Thank you. I will let my mother in law know to contact them.jonesMUFCforever said:

I would not think that the car would need to be sold.said:Thank you for your reply. He didn’t have any savings or insurance policies in his own name. He had a private pension but we have checked and it does not come with any death benefits. Their shared car was in his name - could she be forced to sell that? The amount outstanding on the loan is approx £2000.

Whoever is dealing with the estate as administrator needs to write to M&S loans advising them that the estate has no funds to pay the loan. If all goes well that should be the end of the matter.0 -

We were using this as a guide, and I haven’t seen anywhere else say a car has to go through probate. His name was on the V5, but I’ve seen that a V5 is not considered proof of ownership. It was purchased from their joint account.Are you positive probate is not required because we’ve now got a car that was solely in his name. 0

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.9K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 246.9K Work, Benefits & Business

- 603.5K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards