We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

'Annuities are poor value' - what do they know that we don't?

Comments

-

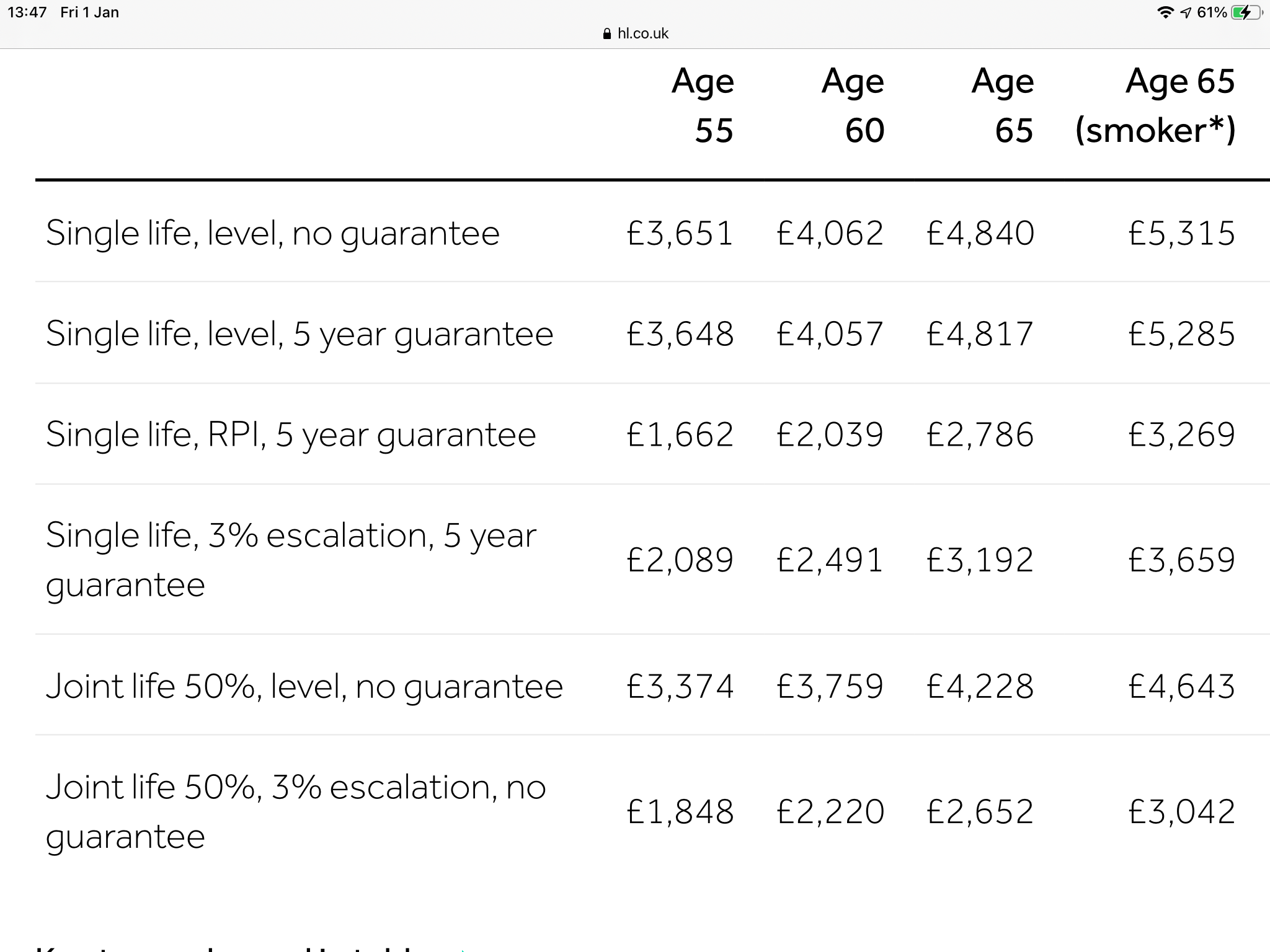

garmeg said:If you look at the amount of level annuity and RPI annuity purchased for the same purchase amount, the annuity market seems to be pricing in a very high level of future inflation compared to that we have been witnessing recently.Not sure if the RPI annuity received will ever catch up with the level one but certainly unlikely to pay out as much if you allow for prior annuity underpayments since purchase!

eg level annuity at 55 is about £3,650 and RPI annuity is about £1,660 ... The annuity market should be valued according to how much it costs the providers to hedge the product (+ other less impactful factors). So for RPI linked it should be priced according to inflation expectations (usually derived from inflation linked securities or break-evens). For nominal it will be nominal government bonds (+corp bonds). The difference reflects the expensiveness in inflation linked securities relative to nominal counterparts. This difference in price perhaps reflects the limited supply of inflation securities.If inflation expectations rise, the difference in the two products should get worse, all else equal (i.e. if REAL yields fall).1

The annuity market should be valued according to how much it costs the providers to hedge the product (+ other less impactful factors). So for RPI linked it should be priced according to inflation expectations (usually derived from inflation linked securities or break-evens). For nominal it will be nominal government bonds (+corp bonds). The difference reflects the expensiveness in inflation linked securities relative to nominal counterparts. This difference in price perhaps reflects the limited supply of inflation securities.If inflation expectations rise, the difference in the two products should get worse, all else equal (i.e. if REAL yields fall).1 -

Deleted_User said:The rules of the game are changing in several fairly fundamental ways. The governments across the world are inflating assets and following MMT without saying so. All these money governments are throwing at people are accompanied by decreases in production. Facebook and Netflix are producing as much as before the pandemic but food production has been reduced. Yet the money supply is growing fast in most countries around the world.That money is going somewhere eventually. Will people just leave the extra cash in savings accounts with negative real interest? Will they buy shares? Will they take cruises? Will they buy Bitcoin or houses? Do we have asset bubbles? Will the secular decrease in inflation since 1980s be reversed? Which assets will be favoured as a result of new and increasing taxation?

I don’t know the answers to any of these questions but its not obvious why statistics on past market performance should be used to predict the future. Diversification is going to be key to wealth preservation and annuity is one of the tools within that mix.Agree.Much will depends on what form MMT takes. We saw a form of MMT in 2020 - incomes went up to levels more than in 2019, all because of fiscal spending.And given what happened to asset prices, it makes sense that MMT up to a certain level will actually worsen wealth inequality (although income inequality would reduce) - the poor have a much higher propensity to spend than the rich.The only way to reduce wealth inequality is through asset price deflation (perhaps through reversal of most/all the QE of past 10 years) or wealth taxes (a high enough level of MMT may achieve similar results but would probably have bad outcomes for savers - so a direct wealth tax is ideal).I think further MMT alone can only be bullish for risk assets and damaging for risk free ones. But there will be a point where risk assets have priced in a lot more MMT than the economy can handle WITHOUT INFLATION rising to concerning levels.0 -

It maybe very damaging for savers/bond holders if the government FORCES lending at below market rates to the private market. Potentially also damaging for risky assets if lenders are forced to sell risky assets to fund the lending - i.e. the lenders are not banks but institutions investing on behalf of private individuals/corporations.I am very scared about the future.0

-

The past 40-50 years has been a bull market in bonds as interest rates have fallen........... 60/40 portfolio may have worked in the past. Future looks very different.michaels said:Age 55 no health issues annuity for self and 100% for spouse, RPI increase (HL tool): 1.39%

No fail in 40 years SWR based on historic data 75:25 stocks/bonds 0.25% fees drag (cfiresim): 3%

Seems to me there is not much chance of your withdrawals having to go down below 1.39% based on any reasonable drawdown strategy?2 -

If bonds are not the optimal constituent of the '40' component of a 60/40 balanced portfolio, will the purveyors of ready-made multi-asset products (HSBC, Vanguard, etc.) use something else? I'd be more inclined to trust their respective fund managers than the folks posting here (no offenceThrugelmir said:

The past 40-50 years has been a bull market in bonds as interest rates have fallen........... 60/40 portfolio may have worked in the past. Future looks very different.michaels said:Age 55 no health issues annuity for self and 100% for spouse, RPI increase (HL tool): 1.39%

No fail in 40 years SWR based on historic data 75:25 stocks/bonds 0.25% fees drag (cfiresim): 3%

Seems to me there is not much chance of your withdrawals having to go down below 1.39% based on any reasonable drawdown strategy?") ) 1

) 1 -

The 40 are mainly expected to be bonds, but short term, intermediate or long term makes a difference.

I suspect though that Thrugelmir's objection is that using 60-40 will not generate the returns which seem to form the basis of support for DIY and objecting to Annuities where the alternative would be someone else's problem (as it is with DB schemes)I think I saw you in an ice cream parlour

Drinking milk shakes, cold and long

Smiling and waving and looking so fine0 -

Not an objection. Just a statement of fact. In the absence of a secure long term returns from Government stocks. The only option currently available is to take a higher degree of risk with alternative investments to supplement bonds. There's no magical return on bonds that's suddenly going to materialise.mark55man said:

I suspect though that Thrugelmir's objection is that using 60-40 will not generate the returns which seem to form the basis of support for DIY and objecting to Annuities where the alternative would be someone else's problem (as it is with DB schemes)

2 -

Plenty of quality discussion in the public domain regarding bonds for some time. Fund managers provide products that match risk profiles. They neither predict or guarantee returns. My observation is purely from the aspect of investor disappointment. That future returns cannot be of the same magnitude of the past as matters currently stand. Might change in the future but who knows when. Likewise fund managers will offer products as long as the demand exists and the fund itself remain economic to run. That's the inherent danger in not taking advice and understanding fully what you are invested in. Self investment to lower management costs could ultimately backfire for some. Balanced portfolios are built to dampen volatility not improve returns. Optimisation over maximisation.shinytop said:

If bonds are not the optimal constituent of the '40' component of a 60/40 balanced portfolio, will the purveyors of ready-made multi-asset products (HSBC, Vanguard, etc.) use something else? I'd be more inclined to trust their respective fund managers than the folks posting here (no offenceThrugelmir said:

The past 40-50 years has been a bull market in bonds as interest rates have fallen........... 60/40 portfolio may have worked in the past. Future looks very different.michaels said:Age 55 no health issues annuity for self and 100% for spouse, RPI increase (HL tool): 1.39%

No fail in 40 years SWR based on historic data 75:25 stocks/bonds 0.25% fees drag (cfiresim): 3%

Seems to me there is not much chance of your withdrawals having to go down below 1.39% based on any reasonable drawdown strategy?)

1 -

Absolute safety costs a lot of money when interest rates are low. I seem to recall that they dropped at the time of the Great Financial Crash around 2008. Central banks pulled down interest rates to encourage lending, and restart the economy, which had stalled due to fears over bad debt. Interest rates are likely to stay low given the parlous state of the economy, although it is only certain sectors that have been hit, mainly leisure and retail.

Historically stocks and shares are safe in the long term and the longer you are invested the safer they become thanks to compound growth. The big danger in the short term of course is a mega crash, your funds drop 90%, and you consume the now depleted funds by withdrawals. In practice this is incredibly unlikely, albeit possible. If this happens, it means something really bad has happened, in which case would annuity companies be in a position to honour their obligations?

A more likely scenario is a halving of the markets due to a shock such as an energy crisis. Historically markets have recovered in a few years, and this level of crash can be hedged against with a cash safety buffer equal to several years living costs. Obviously there is a cost associated with gains lost from this money not being in the markets. And this does assume a recovery in a few years. But if you’ve already been invested in the markets many years, chances are you’ve had very good growth and your funds can take some losses, even 50% over many years, without you suffering unduly.

This does assume someone who can budget responsibly and not blow the lot on a Ferrari and posh holidays. It also assumes future markets behave ‘as expected’ and the absence of a serious event such as a global war. IMO a war, or at least a conflict, with China is quite likely given the way that China is behaving.

I’m quite happy to accept these risks, I have investments in SIPP and ISA wrappers which I am drawing down, and I have a full UK pension entitlement arriving in 10 years time, equal to £8500/year in today’s money which will cover the basics ie council tax, heating, food etc. Yes there’s a risk, but it’s managed.

1 -

US stocks 1929-1932 drawdown: 84%. And thats just 100 years of historic data. Other markets lost more, up to 100%. Someone 50 today can easily live another 50 years. A major event over that period of time is credible.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards