We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Bond index fund vs savings account

Comments

-

It's one theory, and a crude one at that.masonic said:Another_Saver said:

I wish I would claim credit, but if you search Peter Zeihan, David Willetts The Pinch or The Great Demographic Reversal you'll find I'm as novel as a Star Wars sequel.masonic said:Another_Saver said:

Er... I think you've misunderstood me in your first para. I don't understand you at all sorry.masonic said:Another_Saver said:Interest rates have to stay this low until Boomers start materially divesting. Peter Zeihan has put this at 2022 for the US, for the UK the post-war boom are already there but the 60s boom peaked in 1964. Most people retire around or shortly before SPA, but then wealth is very sharply distributed with a Gini of 0.63-0.73. This lowers the capital supply or ratio of wealth to GDP which has been rising sharply since the Boomers started saving in the 80s ("big bang" or "expansionary 80s") and lowers the working population relative to the total, probably driving inflation and a rise in interest rates though nowhere near 60s-90s levels...Please never get a job at The Plain English Campaign! Please could you explain why interest rates, which principally determine how much companies can affordably borrow and how much leverage they can use to drive earnings, should be determined by the date of birth of their shareholders or the number of working age people available for employment? Company shares can be traded at any time and are owned at all times. The number of employees needed to generate the same quantity of earnings has been continuously falling.Or are you saying, to put it in simple terms, that most of the world's wealth is trapped in cash held by old people, and we have to wait for them to die and their heirs to invest it before the economy can get back to normal?Im talking about demographics and capital supply. In a neo-liberal economy wealth tends to be concentrated at the age of retirement. Different age structures affect the relative capital suppl, cash/bonds is the largest form of capital in the UK, all other assets need to be divested into cash or generate cash before they can be used for consumption. I think this is the main factor in determining rates but plenty of others come into it.

Your second para is so extremely simplified that it's not an accurate representation of y point - I haven't mentioned inheritance and Boomers dying and the inheritance of their wealth won't solve the problem, the abnormal savings glut needs to be consumed to reduce the wealth/GDP ratio for interest rates to get back to normal.Yes, very crudely, people have peak wealth at the point they retire, they build it through paid employment up to that point, and after that point they use it to fund their living costs and deplete it. I think that has little to do with the setting of interest rates, which is mainly dependent on the predicted state of the economy several months ahead, which in turn depends on various factors, such as the rate of inflation, the rate of GDP growth, unemployment figures etc. It is not typically impacted at all by the amount of consumer savings held in deposit accounts, or the amount people have in their pensions. The MPC, who set the BoE base rate, outline the factors they consider when deciding the rate, so this is not a matter for speculation.You mention the UK boom of the 60s, centred on 1964. Someone born in 1964 will be around 57 years old today and therefore could have another 8 years of human capital left in them until reaching state retirement age. Due to the changing nature of work, people can and often do stay engaged with paid work up to and beyond the point they could choose to retire. This is especially true of high earners, so they may not dip into their pension savings for quite some time. If your prediction is that UK interest rates will stay at historic lows until these people have depleted their retirement savings, then that is certainly an interesting and novel view.Is that the same David Willetts who is a Conservative peer in the House of Lords and was the universities minister who orchestrated the rise in university tuition fees to £9,000 per year?Zeihan, so far as I can surmise, blames a lot on demographics, but I've not been able to find anything linking them to the historically low central bank interest rates we find today, or suggesting said interest rates cannot be raised until those fresh retirees spend down their capital. He does suggest that asset buying has driven up capital values in the bond market and that is evidence based, but the MPC and other interest rate setters do not need to mirror bond yields - otherwise rates would already be negative. At least I now know the origin of the rather abstruse text in your earlier post. If I read much more of his blog my eyes might cross.So, if we entertain the notion that in the US in 2022 there is going to be a 'tsunami of government-bond-capital' and that that interest rates must be held at historic lows until the start or end of that process (based on your earlier posts, not anything I found Zeihan state), then you are making a prediction that the UK will have historic low rates for many years to come. Here are the UK demographics: That 'boomer' generation you mentioned, that was born in the 60s and centred on 1964, whose average member is age 57 today, is right in the middle of the 55-59 year old band. Behind that are two highly populous bands, the 50-54 year-olds and the 45-49 year-olds. The youngest of these have over 20 years until state retirement age. Behind that comes another boom of 25-39 year olds, born in the 1980s and 1990s and almost as populous as the 45-59 year olds. Having survived into their 20s, very few of these will die off before they reach their 50s and 60s, and will have greater life-expectancy. So as the older group starts to shed their bond holdings, the younger group will be 'lifestyling' into bonds and slurp them up. Could be another 40+ years until the tsunami in the UK.

That 'boomer' generation you mentioned, that was born in the 60s and centred on 1964, whose average member is age 57 today, is right in the middle of the 55-59 year old band. Behind that are two highly populous bands, the 50-54 year-olds and the 45-49 year-olds. The youngest of these have over 20 years until state retirement age. Behind that comes another boom of 25-39 year olds, born in the 1980s and 1990s and almost as populous as the 45-59 year olds. Having survived into their 20s, very few of these will die off before they reach their 50s and 60s, and will have greater life-expectancy. So as the older group starts to shed their bond holdings, the younger group will be 'lifestyling' into bonds and slurp them up. Could be another 40+ years until the tsunami in the UK.

A few corrections - Willetts didn't orchestrate the £9k fees that aren't really fees, it was the Browne review started under Gordon Brown and both main parties were for it. Also I don't engage with the old argumentum and hominem. Zeihan's an entertainer but I think there is some merit in what he says.

Current developed world demographics are unlike anything the world has ever known. Nost countries fall into one of four categories:

1. Poor undeveloped - convex. life expectancy 30-40. Almost no opportunity for capital.

2. UK in 1900 - pyramid (or triangle if using a single axis rather than a gender split one). 1/5 kids die by 5, Starting to build capital, population able to grow.

3. Developing - sanitation, vaccination, medicine, sewage, hygiene, clean tap water, education, availability of contraception etc. Stops kids dying by 5, a demographic dividend grows up through the generations and starts to fill out the upper age brackets. The need for a broader financial system, savings, retirement arises, people don't need to have as many kids. Capital becomes cheaper (in the 1800/s the UK's dividend yield was often 7-8%, in the 1900s typically 4-6%, now we think of 4% as cheap, and the US has averaged 2% for the last 30 years in spite of following similar historical patterns). Im not aware of other decent explanations for why stock market valuations, house prices have all been rising and interest rates falling for so long (over the very long term, as in multi generational time spans, but you could argue demographics also explain that big inflation and interest rates bulge from the 60s through the 90s, obviously intersected with plenty of political explanations i.e. OPEC, Bretton Woods, Gold Standard, transition to service economy, Thatcher/Reagan-isms) so if you know of any I'd really appreciate a link") 4a) Developed, chimney stack, capital is cheap.

4a) Developed, chimney stack, capital is cheap.

4b) developed with a baby boom, baby bust an no recovery (Japan, Germany, Korea, China) weird things start to happen.

So although a UK population age pyramid doesn't look to have anything wrong with it, comparing it with global and historical examples shows current demographics to be abnormal.0 -

Linton said:

The phrase "an interesting and novel view" may be used in academic circles when one doesnt want to offend someone expounding their latest dubious theory. Whether that is the case here I cannot say.Another_Saver said:

I wish I would claim credit, but if you search Peter Zeihan, David Willetts The Pinch or The Great Demographic Reversal you'll find I'm as novel as a Star Wars sequel.masonic said:Another_Saver said:

Er... I think you've misunderstood me in your first para. I don't understand you at all sorry.masonic said:Another_Saver said:Interest rates have to stay this low until Boomers start materially divesting. Peter Zeihan has put this at 2022 for the US, for the UK the post-war boom are already there but the 60s boom peaked in 1964. Most people retire around or shortly before SPA, but then wealth is very sharply distributed with a Gini of 0.63-0.73. This lowers the capital supply or ratio of wealth to GDP which has been rising sharply since the Boomers started saving in the 80s ("big bang" or "expansionary 80s") and lowers the working population relative to the total, probably driving inflation and a rise in interest rates though nowhere near 60s-90s levels...Please never get a job at The Plain English Campaign! Please could you explain why interest rates, which principally determine how much companies can affordably borrow and how much leverage they can use to drive earnings, should be determined by the date of birth of their shareholders or the number of working age people available for employment? Company shares can be traded at any time and are owned at all times. The number of employees needed to generate the same quantity of earnings has been continuously falling.Or are you saying, to put it in simple terms, that most of the world's wealth is trapped in cash held by old people, and we have to wait for them to die and their heirs to invest it before the economy can get back to normal?Im talking about demographics and capital supply. In a neo-liberal economy wealth tends to be concentrated at the age of retirement. Different age structures affect the relative capital suppl, cash/bonds is the largest form of capital in the UK, all other assets need to be divested into cash or generate cash before they can be used for consumption. I think this is the main factor in determining rates but plenty of others come into it.

Your second para is so extremely simplified that it's not an accurate representation of y point - I haven't mentioned inheritance and Boomers dying and the inheritance of their wealth won't solve the problem, the abnormal savings glut needs to be consumed to reduce the wealth/GDP ratio for interest rates to get back to normal.Yes, very crudely, people have peak wealth at the point they retire, they build it through paid employment up to that point, and after that point they use it to fund their living costs and deplete it. I think that has little to do with the setting of interest rates, which is mainly dependent on the predicted state of the economy several months ahead, which in turn depends on various factors, such as the rate of inflation, the rate of GDP growth, unemployment figures etc. It is not typically impacted at all by the amount of consumer savings held in deposit accounts, or the amount people have in their pensions. The MPC, who set the BoE base rate, outline the factors they consider when deciding the rate, so this is not a matter for speculation.You mention the UK boom of the 60s, centred on 1964. Someone born in 1964 will be around 57 years old today and therefore could have another 8 years of human capital left in them until reaching state retirement age. Due to the changing nature of work, people can and often do stay engaged with paid work up to and beyond the point they could choose to retire. This is especially true of high earners, so they may not dip into their pension savings for quite some time. If your prediction is that UK interest rates will stay at historic lows until these people have depleted their retirement savings, then that is certainly an interesting and novel view.Well if I didn't find it interesting I wouldn't write about it. As for novel or dubious:- Willetts wrote a book (with a politicial agenda and commercial title, but still very well researched) about demographics in 2011 (https://www.amazon.co.uk/Pinch-Boomers-Childrens-Future-Should/dp/1848872321), is a Fellow of the Academy of Social Sciences, delivered a lecture about this at the Royal Society earlier this year ( https://www.youtube.com/watch?v=ZuXzvjBYW8A, if you don't have 47 minutes you can glance slides from an earlier speech here: https://www.resolutionfoundation.org/app/uploads/2015/12/DW-slides-for-website.pdf), and chaired the Resolution Foundation's Intergenerational Commission.- You can read the credentials of the authors of the Great Demographic Reversal here: https://www.lse.ac.uk/Events/Open/202010261700/the-great-demographic-reversal- This was mentioned in a paper in 2003, I've written more at the bottom of this post.

https://www.youtube.com/watch?v=ZuXzvjBYW8A, if you don't have 47 minutes you can glance slides from an earlier speech here: https://www.resolutionfoundation.org/app/uploads/2015/12/DW-slides-for-website.pdf), and chaired the Resolution Foundation's Intergenerational Commission.- You can read the credentials of the authors of the Great Demographic Reversal here: https://www.lse.ac.uk/Events/Open/202010261700/the-great-demographic-reversal- This was mentioned in a paper in 2003, I've written more at the bottom of this post.

Perhaps some of your assumptions could be open to question. Naturally wealth will tend to be concentrated in older people generally, though far from particularly, because it takes time to accumulate. However that does not mean the reduction in the numbers of older people will reduce the amount of stored wealth. Far more employees are accumulating personal pension pots and those pension pots will be larger than was the case in the past. Perhaps this will outweigh the decrease in numbers.Agreed, participation in financial products is wider and widening, this represents a material, structural difference.I would agree that the distribution of wealth does have major economic consequences many of them undesirable. But this is not necessarily linked to age. For example if you give more money to the very poor they will tend to use it for immediate consumption, thus adding to the economy. If you give more money to the very rich they are far more likely to use it on buying assets so potentially inceasing inflation. In the case of retirees there are comparatively few in the bracket where their assets greatly exceed their ability to consume.Which makes both the total wealth distribution and the distribution of different assets interesting and messy, both now and over time.

Whether my comments address your theory I am far from clear so would appreciate it if you rephrased it in simple language, ideally incuding the mechanisms whereby the predicted undesirable consequences will be caused.In a sentence all I did was combine supply-side models of capital with demography. A country's demographics (age structure, population pyramid) are related. Go on https://www.populationpyramid.net/burundi/2019/, the poorest countries look like a convex curve, lower-middle income countries start to look like a triangle, in upper-middle income countries the triangle starts to turn into the hooded chimney of the developed world, and if you're not careful you end up like Germany or Japan, and if you try and manipulate things you end up like China with a double peak of Boomers providing the capital and experience and Millennials providing the cheap labour and consumption, for now...Arnott and Bernstein said this in their 2003 paper on stock dilution published in the CFA Journal:"Two independent analytical methods point to the same conclusion: In stable nations, a roughly 2 percent net annual creation of new shares-the Two Percent Dilution-leads to a separation between long-term economic growth and longterm growth in dividends per share, earnings per share, and share price. The markets are probably in the eye of a storm and can expect further turmoil as the rest of the storm passes over. If normalized S&P 500 earnings are $30-$36 per share, if payout ratios on those normalized earnings are at the low end of the historical range (implying lower-than-normal future earnings growth), if normal earnings growth is really only about 1 percent a year above inflation, if stock buybacks have been little more than an appealing fairy tale, if the credibility of earnings is at an all-time low, and if demographics suggest Baby Boomer dis-saving in the next 20 years, then we have a problem."For historic context this was in the aftermath of the arrest of the Wolf of Wall Street, Dot-Com Bubble, 9/11, Enron and start of the Iraq War.I just think it's an interesting perspective, it makes sense and seems to be fairly well supported by data when used.0 -

Another_Saver said:It's one theory, and a crude one at that.I wouldn't call it a theory, just a series of observations that would need to be addressed by a theory. I'm not trying to theorise what is going to happen to interest rates in the next few years based on demographics, you are. I'm just trying to get to the bottom of what you are trying to say, and it seems I'm not the only poster that is finding your explanations unintelligible. It's rather uncharitable of you to send me off to research the background to your claims and then disparage me for not having as refined understanding as you after about 45 minutes trying to get up to speed on the topic.

It wasn't argumentum ad hominem (I'm not aware of any arguments he put forward, I was unable to find any comments at all on the topic at hand that were attributed to him). I was merely surprised to see that name and that's all I remember him for. Perhaps my choice of wording could have been better - 'presided over' would have been more appropriate. While I don't want to drag us onto a completely different topic, it was the original call for 50% of people to go to university that was the questionable policy setting off this chain of events, and that was Tony Blair's legacy.Another_Saver said:A few corrections - Willetts didn't orchestrate the £9k fees that aren't really fees, it was the Browne review started under Gordon Brown and both main parties were for it. Also I don't engage with the old argumentum and hominem.

I'm not really sure what phrases like "capital becomes cheaper" mean. You've used capital in your point (2) to denote assets owned by people, such as savings, investments and property (I assume that's what you mean by 'build capital'), but assets have not been getting progressively cheaper over the centuries. There is also human capital (the ability of people to sell their money for time), but in general people have been paid more as economies develop, so human capital becomes more expensive. The bit in brackets after "capital becomes cheaper" leads me to believe you are actually making a statement about dividends.Another_Saver said:Current developed world demographics are unlike anything the world has ever known. Nost countries fall into one of four categories:

1. Poor undeveloped - convex. life expectancy 30-40. Almost no opportunity for capital.

2. UK in 1900 - pyramid (or triangle if using a single axis rather than a gender split one). 1/5 kids die by 5, Starting to build capital, population able to grow.

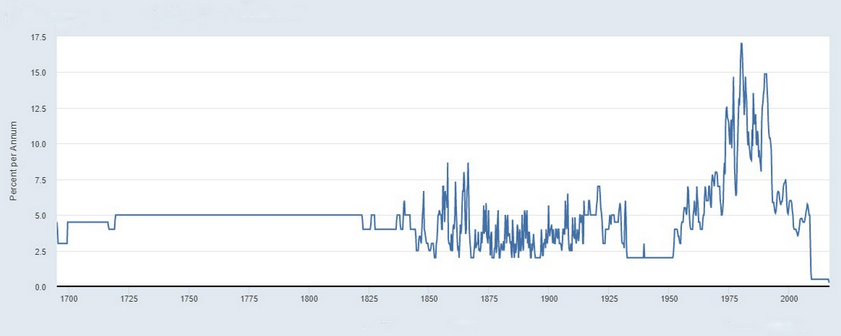

3. Developing - sanitation, vaccination, medicine, sewage, hygiene, clean tap water, education, availability of contraception etc. Stops kids dying by 5, a demographic dividend grows up through the generations and starts to fill out the upper age brackets. The need for a broader financial system, savings, retirement arises, people don't need to have as many kids. Capital becomes cheaper (in the 1800/s the UK's dividend yield was often 7-8%, in the 1900s typically 4-6%, now we think of 4% as cheap, and the US has averaged 2% for the last 30 years in spite of following similar historical patterns).You can use measures such as the price:earnings ratio to value stocks and determine that they are cheap or expensive, but dividends are not correlated with earnings - if a company can increase future earnings through reinvesting current earnings then it will do so and not pay out those current earnings as a dividend. Companies perceived to be able to grow their earnings substantially will see their share prices rise to higher earnings multiples than those who can not. The average yield of the FTSE100 over the past 30 years is about 3.2%, the current yield is 3.01%. It has ranged from 2% (at the peak of of the dotcom bubble) to nearly 5% (at the low point of the global financial crisis). It's going to fluctuate as asset prices fluctuate due to market sentiment.Another_Saver said:Im not aware of other decent explanations for why stock market valuations, house prices have all been rising and interest rates falling for so long (over the very long term, as in multi generational time spans, but you could argue demographics also explain that big inflation and interest rates bulge from the 60s through the 90s, obviously intersected with plenty of political explanations i.e. OPEC, Bretton Woods, Gold Standard, transition to service economy, Thatcher/Reagan-isms) so if you know of any I'd really appreciate a linkPresumably you are aware of explanations for why stock market valuations and house prices have been rising. It is not necessary for interest rates to fall when the stock market rises or when houses become more expensive, and the rationale for separate factors governing asset prices and interest rates is much simpler and more compelling. If we examine the premise that "interest rates falling for so long (over the very long term, as in multi generational time spans..." using a chart from the Bank of England showing the base rate since the late 17th century: It's quite clear that over 300 years, interest rates have not been gradually falling over the very long term. You quite rightly point out the bulge around the 70s and 80s that was due to high inflation, there were also periods like the 30s and 40s, and the late 1800s where it was lower than average. The real anomaly is what happened in 2008 in response to the global financial crisis and this marked quite a departure from previous economic policy - the drastic cutting of interest rates and expansion of the money supply to avert a great depression. That is what has led to such a sudden drop in interest rates from ~5%, which is the historic norm, almost straight down to sub-1%, where it has been held for fear of the economic impact on debtors were it to be raised. Inflation has also not been a bother during this period, despite warnings that mass QE would create hyperinflation, so the main impetus to bring up rates has been largely missing.I realise you requested a link, so here you go: https://www.economicshelp.org/macroeconomics/monetary-policy/effect-raising-interest-rates/

It's quite clear that over 300 years, interest rates have not been gradually falling over the very long term. You quite rightly point out the bulge around the 70s and 80s that was due to high inflation, there were also periods like the 30s and 40s, and the late 1800s where it was lower than average. The real anomaly is what happened in 2008 in response to the global financial crisis and this marked quite a departure from previous economic policy - the drastic cutting of interest rates and expansion of the money supply to avert a great depression. That is what has led to such a sudden drop in interest rates from ~5%, which is the historic norm, almost straight down to sub-1%, where it has been held for fear of the economic impact on debtors were it to be raised. Inflation has also not been a bother during this period, despite warnings that mass QE would create hyperinflation, so the main impetus to bring up rates has been largely missing.I realise you requested a link, so here you go: https://www.economicshelp.org/macroeconomics/monetary-policy/effect-raising-interest-rates/

I don't disagree the UK population age pyramid is bulging to the right, and there is a danger of the UK becoming susceptible to Japanification over the long term, what I'm not getting is what the relevance of that is to when interest rates will start to rise.Another_Saver said:So although a UK population age pyramid doesn't look to have anything wrong with it, comparing it with global and historical examples shows current demographics to be abnormal.2 -

...masonic said:Another_Saver said:It's one theory, and a crude one at that.I wouldn't call it a theory, just a series of observations that would need to be addressed by a theory. I'm not trying to theorise what is going to happen to interest rates in the next few years based on demographics, you are. I'm just trying to get to the bottom of what you are trying to say, and it seems I'm not the only poster that is finding your explanations unintelligible. It's rather uncharitable of you to send me off to research the background to your claims and then disparage me for not having as refined understanding as you after about 45 minutes trying to get up to speed on the topic.

I didn't

It wasn't argumentum ad hominem (I'm not aware of any arguments he put forward, I was unable to find any comments at all on the topic at hand that were attributed to him). I was merely surprised to see that name and that's all I remember him for. Perhaps my choice of wording could have been better - 'presided over' would have been more appropriate. While I don't want to drag us onto a completely different topic, it was the original call for 50% of people to go to university that was the questionable policy setting off this chain of events, and that was Tony Blair's legacy.Another_Saver said:A few corrections - Willetts didn't orchestrate the £9k fees that aren't really fees, it was the Browne review started under Gordon Brown and both main parties were for it. Also I don't engage with the old argumentum and hominem.

I'm not really sure what phrases like "capital becomes cheaper" mean.Another_Saver said:Current developed world demographics are unlike anything the world has ever known. Nost countries fall into one of four categories:

1. Poor undeveloped - convex. life expectancy 30-40. Almost no opportunity for capital.

2. UK in 1900 - pyramid (or triangle if using a single axis rather than a gender split one). 1/5 kids die by 5, Starting to build capital, population able to grow.

3. Developing - sanitation, vaccination, medicine, sewage, hygiene, clean tap water, education, availability of contraception etc. Stops kids dying by 5, a demographic dividend grows up through the generations and starts to fill out the upper age brackets. The need for a broader financial system, savings, retirement arises, people don't need to have as many kids. Capital becomes cheaper (in the 1800/s the UK's dividend yield was often 7-8%, in the 1900s typically 4-6%, now we think of 4% as cheap, and the US has averaged 2% for the last 30 years in spite of following similar historical patterns).

Capital/wealth, and the demand for it, are a supply demand model. Capital has to come from somewhere and be deployed somewhere, and in a neo-liberal economy (ie one with capitalism, a financial system, social mobility, education etc.) it tends to be owned by older generations and used by younger generations.

If capital is cheap, there it lots of it, a high wealth/GDP ratio, returns are low, interest rates are low, and this coincides with having more older people.If capital is expensive, interest rates are high, there tend to be more younger people, a lower wealth to GDP ratio, returns tend to be higher.

You've used capital in your point (2) to denote assets owned by people, such as savings, investments and property (I assume that's what you mean by 'build capital'), but assets have not been getting progressively cheaper over the centuries. There is also human capital (the ability of people to sell their money for time), but in general people have been paid more as economies develop, so human capital becomes more expensive. The bit in brackets after "capital becomes cheaper" leads me to believe you are actually making a statement about dividends.You can use measures such as the price:earnings ratio to value stocks and determine that they are cheap or expensive, but dividends are not correlated with earnings - if a company can increase future earnings through reinvesting current earnings then it will do so and not pay out those current earnings as a dividend. Companies perceived to be able to grow their earnings substantially will see their share prices rise to higher earnings multiples than those who can not. The average yield of the FTSE100 over the past 30 years is about 3.2%, the current yield is 3.01%. It has ranged from 2% and(at the peak of of the dotcom bubble) to nearly 5% (at the low point of the global financial crisis). It's going to fluctuate as asset prices fluctuate due to market sentiment.

This isn't related to my point. Also both in theory and fact dividends (or the total payout) should be and are correlated with earnings and prices at the level of a national index. In reality, higher dividend payout ratios have been found to indicate higher future earnings growth more than lower payout ratios in spite of perceptions (I think the coincidence of manipulation of earnings with compankest that fail explains a chunk of this phenomenon).Regardless, across the developed world valuations have increased materially over the very long term. Sentiment does not create extra wealth to flow into the market. Demographics is one factor to explain the difference, other potential explanations include widening market participation.Another_Saver said:Im not aware of other decent explanations for why stock market valuations, house prices have all been rising and interest rates falling for so long (over the very long term, as in multi generational time spans, but you could argue demographics also explain that big inflation and interest rates bulge from the 60s through the 90s, obviously intersected with plenty of political explanations i.e. OPE, Bretton Woods, Gold Standard, transition to service economy, Thatcher/Reagan-isms) so if you know of any I'd really appreciate a linkPresumably you are aware of explanations for why stock market valuations and house prices have been rising. It is not necessary for interest rates to fall when the stock market rises or when houses become more expensive, and the rationale for separate factors governing asset prices and interest rates is much simpler and more compelling. If we examine the premise that "interest rates falling for so long (over the very long term, as in multi generational time spans..." using a chart from the Bank of England showing the base rate since the late 17th century:It's quite clear that over 300 years, interest rates have not been gradually falling over the very long term. You quite rightly point out the bulge around the 70s and 80s that was due to high inflation, there were also periods like the 30s and 40s, and the late 1800s where it was lower than average. The real anomaly is what happened in 2008 in response to the global financial crisis and this marked quite a departure from previous economic policy - the drastic cutting of interest rates and expansion of the money supply to avert a great depression. That is what has led to such a sudden drop in interest rates from ~5%, which is the historic norm, almost straight down to sub-1%, where it has been held for fear of the economic impact on debtors were it to be raised. Inflation has also not been a bother during this period, despite warnings that mass QE would create hyperinflation, so the main impetus to bring up rates has been largely missing.I realise you requested a link, so here you go: https://www.economicshelp.org/macroeconomics/monetary-policy/effect-raising-interest-rates/

That's standard modern monetary theory which ignores demography and relies on agency theory. Again, other historical structural changes become relevant over those kinds of timescales (1692 Britain and 2020 Britain are so different an economic comparison is hardly possible).

I don't disagree the UK population age pyramid is bulging to the right, and there is a danger of the UK becoming susceptible to Japanification over the long term, what I'm not getting is what the relevance of that is to when interest rates will start to rise.Another_Saver said:So although a UK population age pyramid doesn't look to have anything wrong with it, comparing it with global and historical examples shows current demographics to be abnormal.

Because of the (potential) relationship between demographics and capital supply/wealth. The Boomer savings glut is a recognised phenomenon.0 -

Your answers make no sense to me. We are disagreeing on what the facts are (e.g. dividends correlating with earnings - some companies and types of company pay zero dividends yet generate impressive profits, while others will pay out almost all of their profits to shareholders). I also still fail to see anything resembling a nuts and bolts explanation for how this successor to "standard modern monetary theory" operates in the topic at hand. It all seems very nebulous. Regretfully I don't think there is any productive discussion to be had here, I'm out.

3 -

That's because we are talking about different things. I never said anything about dividends not did I claim to offer a successor to MMT.masonic said:Your answers make no sense to me. We are disagreeing on what the facts are (e.g. dividends correlating with earnings - some companies and types of company pay zero dividends yet have impressive earnings and even profits, while others will pay out almost all of their profits to shareholders). I also still fail to see anything resembling a nuts and bolts explanation for how this successor to "standard modern monetary theory" operates in the topic at hand. It all seems very nebulous. Regretfully I don't think there is any productive discussion to be had here, I'm out.I was talking about the fact that demographics are a factor in an economy's wealth or supply of capital that in part explain interest rates, and that as Boomers retire and divest their accumulated wealth, the "savings glut" we hear so much about, into consumption, we should expect rates to return to normal.This idea has been mentioned in sources going back to at least the Arnott and Bernstein paper in 2003. PIMCO have published an article to the contrary, challenging this idea as a "popular view" (https://blog.pimco.com/en/2016/06/70-is-the-new-65-savings-glut-alive-and-well/), though they have an obvious interest in downplaying the risk of rising rates to fixed income investors.0 -

In the interest of correcting the record only:Another_Saver said:

That's because we are talking about different things. I never said anything about dividends not did I claim to offer a successor to MMT.masonic said:Your answers make no sense to me. We are disagreeing on what the facts are (e.g. dividends correlating with earnings - some companies and types of company pay zero dividends yet have impressive earnings and even profits, while others will pay out almost all of their profits to shareholders). I also still fail to see anything resembling a nuts and bolts explanation for how this successor to "standard modern monetary theory" operates in the topic at hand. It all seems very nebulous. Regretfully I don't think there is any productive discussion to be had here, I'm out.Another_Saver said:Capital becomes cheaper (in the 1800/s the UK's dividend yield was often 7-8%, in the 1900s typically 4-6%, now we think of 4% as cheap, and the US has averaged 2% for the last 30 years in spite of following similar historical patterns).(my first mention of dividends was a response to this post)Another_Saver said:That's standard modern monetary theory which ignores demography and relies on agency theory. Again, other historical structural changes become relevant over those kinds of timescales (1692 Britain and 2020 Britain are so different an economic comparison is hardly possible).(if there is a 'better' theory that incorporates demography and/or does not rely on agency theory, and was formulated after MMT, then that would be a 'successor')Another_Saver said:I was talking about the fact that demographics are a factor in an economy's wealth or supply of capital that in part explain interest rates, and that as Boomers retire and divest their accumulated wealth, the "savings glut" we hear so much about, into consumption, we should expect rates to return to normal.This idea has been mentioned in sources going back to at least the Arnott and Bernstein paper in 2003. PIMCO have published an article to the contrary, challenging this idea as a "popular view" (https://blog.pimco.com/en/2016/06/70-is-the-new-65-savings-glut-alive-and-well/), though they have an obvious interest in downplaying the risk of rising rates to fixed income investors.The precise statement was "Interest rates have to stay this low until Boomers start materially divesting. Peter Zeihan has put this at 2022 for the US, for the UK the post-war boom are already there but the 60s boom peaked in 1964." If I completely misinterpreted that to mean that interest rates in the UK have to stay this low until the 60s-Boomers start materially divesting in circa. 2030, then I apologiseAlso, not wishing to flog a dead horse, but I seem to recall US interest rates went up steadily between 2016-2019. They of course came right back down again as the pandemic struck.

0 -

...masonic said:

In the interest of correcting the record only:Another_Saver said:

That's because we are talking about different things. I never said anything about dividends not did I claim to offer a successor to MMT.masonic said:Your answers make no sense to me. We are disagreeing on what the facts are (e.g. dividends correlating with earnings - some companies and types of company pay zero dividends yet have impressive earnings and even profits, while others will pay out almost all of their profits to shareholders). I also still fail to see anything resembling a nuts and bolts explanation for how this successor to "standard modern monetary theory" operates in the topic at hand. It all seems very nebulous. Regretfully I don't think there is any productive discussion to be had here, I'm out.Another_Saver said:Capital becomes cheaper (in the 1800/s the UK's dividend yield was often 7-8%, in the 1900s typically 4-6%, now we think of 4% as cheap, and the US has averaged 2% for the last 30 years in spite of following similar historical patterns).(my first mention of dividends was a response to this post)https://forums.moneysavingexpert.com/discussion/comment/77902038/#Comment_77902038

Ah, my bad, i was using historical dividend yieldas an example to illustrate how equity capital has gotten cheaper for issuers/valuation have risen over time. I wasn't making a point about dividends.Another_Saver said:That's standard modern monetary theory which ignores demography and relies on agency theory. Again, other historical structural changes become relevant over those kinds of timescales (1692 Britain and 2020 Britain are so different an economic comparison is hardly possible).(if there is a 'better' theory that incorporates demography and/or does not rely on agency theory, and was formulated after MMT, then that would be a 'successor')https://forums.moneysavingexpert.com/discussion/comment/77902476/#Comment_77902476

I don't know if what I'm talking about has a name or if anyone has created a theoretical framework.Another_Saver said:I was talking about the fact that demographics are a factor in an economy's wealth or supply of capital that in part explain interest rates, and that as Boomers retire and divest their accumulated wealth, the "savings glut" we hear so much about, into consumption, we should expect rates to return to normal.This idea has been mentioned in sources going back to at least the Arnott and Bernstein paper in 2003. PIMCO have published an article to the contrary, challenging this idea as a "popular view" (https://blog.pimco.com/en/2016/06/70-is-the-new-65-savings-glut-alive-and-well/), though they have an obvious interest in downplaying the risk of rising rates to fixed income investors.The precise statement was "Interest rates have to stay this low until Boomers start materially divesting. Peter Zeihan has put this at 2022 for the US, for the UK the post-war boom are already there but the 60s boom peaked in 1964." If I completely misinterpreted that to mean that interest rates in the UK have to stay this low until the 60s-Boomers start materially divesting in circa. 2030, then I apologise

No you've understood a lazily phrased point correctly. I should clarify, I didn't mean have as in there is a condition, I used have to add emphasis, that I don't see how rates could rise until that starts to happen, I don't see another factor or a set of economic conditions on the horizon that could make that happen, therefore rates have to stay this low because there is nothing making rates rise or allowing rates

to rise, other than the possibility of a complete and unlikely change of central bank policy and perhaps a few other unlikelies/unknowns.Also, not wishing to flog a dead horse, but I seem to recall US interest rates went up steadily between 2016-2019. They of course came right back down again as the pandemic struck.

Short term wobbles0 -

Another_Saver said:

I don't know if what I'm talking about has a name or if anyone has created a theoretical framework.masonic said:(if there is a 'better' theory that incorporates demography and/or does not rely on agency theory, and was formulated after MMT, then that would be a 'successor')Any supposition intended to explain something, especially one based on general principles independent of the thing being explained can be referred to as a theory. But let's not get drawn into an argument over the meaning of words.Another_Saver said:The precise statement was "Interest rates have to stay this low until Boomers start materially divesting. Peter Zeihan has put this at 2022 for the US, for the UK the post-war boom are already there but the 60s boom peaked in 1964." If I completely misinterpreted that to mean that interest rates in the UK have to stay this low until the 60s-Boomers start materially divesting in circa. 2030, then I apologiseNo you've understood a lazily phrased point correctly. I should clarify, I didn't mean have as in there is a condition, I used have to add emphasis, that I don't see how rates could rise until that starts to happen, I don't see another factor or a set of economic conditions on the horizon that could make that happen, therefore rates have to stay this low because there is nothing making rates rise or allowing rates

to rise, other than the possibility of a complete and unlikely change of central bank policy and perhaps a few other unlikelies/unknowns.Also, not wishing to flog a dead horse, but I seem to recall US interest rates went up steadily between 2016-2019. They of course came right back down again as the pandemic struck.

Short term wobblesUS interest rates, with a long term average of 4.71%, were cut from 5.25% to 0.1% in the wake of the global financial crisis, but then 'wobbled' to 2.4% (about 50% of the way towards the long term average).If UK rates have to stay this low (0.1%) until c. 2030, but 'this low' incorporates an allowance for 'wobbles' of up to 50% of the long term average of about 5%, then they could theoretically wobble up to about 2.5% over the next few years.As covered in a previous post, the impact on bond funds of a 'wobble' of +2.4% would be a substantial capital loss (but dependent on the average duration of the fund in question). That is the reason for the comment bond funds are "almost offering a return-free risk", and this comment was the precursor to my comments around the dilemma facing those currently holding bonds.So it seems we are talking at cross purposes. I have no objection to the notion that rates will remain below historical averages for quite some years, but they do have the potential to wobble/rise in the short-term. Even a small rise in BoE base rate would have the effect of tipping the balance further in favour of cash over bonds.0 -

I don't think we're disagreeing. I agree bonds don't make sense while the YTM net of fees remains below cash savings and premium bonds. Also, because the yields are so damn low even very meagre rate changes will imply hefty negative returns as we saw on gilts in the 60s going into that mid 70s interest rates peak except without the nice yield you would have gotten then to alleviate the capital loss.masonic said:Another_Saver said:

I don't know if what I'm talking about has a name or if anyone has created a theoretical framework.masonic said:(if there is a 'better' theory that incorporates demography and/or does not rely on agency theory, and was formulated after MMT, then that would be a 'successor')Any supposition intended to explain something, especially one based on general principles independent of the thing being explained can be referred to as a theory. But let's not get drawn into an argument over the meaning of words.Another_Saver said:The precise statement was "Interest rates have to stay this low until Boomers start materially divesting. Peter Zeihan has put this at 2022 for the US, for the UK the post-war boom are already there but the 60s boom peaked in 1964." If I completely misinterpreted that to mean that interest rates in the UK have to stay this low until the 60s-Boomers start materially divesting in circa. 2030, then I apologiseNo you've understood a lazily phrased point correctly. I should clarify, I didn't mean have as in there is a condition, I used have to add emphasis, that I don't see how rates could rise until that starts to happen, I don't see another factor or a set of economic conditions on the horizon that could make that happen, therefore rates have to stay this low because there is nothing making rates rise or allowing rates

to rise, other than the possibility of a complete and unlikely change of central bank policy and perhaps a few other unlikelies/unknowns.Also, not wishing to flog a dead horse, but I seem to recall US interest rates went up steadily between 2016-2019. They of course came right back down again as the pandemic struck.

Short term wobblesUS interest rates, with a long term average of 4.71%, were cut from 5.25% to 0.1% in the wake of the global financial crisis, but then 'wobbled' to 2.4% (about 50% of the way towards the long term average).If UK rates have to stay this low (0.1%) until c. 2030, but 'this low' incorporates an allowance for 'wobbles' of up to 50% of the long term average of about 5%, then they could theoretically wobble up to about 2.5% over the next few years.As covered in a previous post, the impact on bond funds of a 'wobble' of +2.4% would be a substantial capital loss (but dependent on the average duration of the fund in question). That is the reason for the comment bond funds are "almost offering a return-free risk", and this comment was the precursor to my comments around the dilemma facing those currently holding bonds.So it seems we are talking at cross purposes. I have no objection to the notion that rates will remain below historical averages for quite some years, but they do have the potential to wobble/rise in the short-term. Even a small rise in BoE base rate would have the effect of tipping the balance further in favour of cash over bonds.

Demographics are just one component that often gets overlooked.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards