We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Independent Financial Advisors

Comments

-

Look, some people can’t be bothered to spend a bit of effort to understand something that will define their family’s financial well being. They really do need hand holding. That’s fine. However there is lots of evidence that as more information and better investment vehicles have become available, people don’t suddenly sell all their retirement savings during a major bear. If you have a simple multiasset fund in a retirement account it makes it psychologically easier to avoid messing. Don’t even look. Behaviours have improved.Malthusian said:Deleted_User said:The best advice the IFA can give when someone is calling about market turbulence is “bug off”.For a second before hitting "post" I thought I'd crossed the line from satire (tweaking what someone would say to comic effect) to strawman (putting words in someone's mouth that they'd never say). Shouldn't have worried."Bug off" has the same value as telling someone "just run faster" has in athletics coaching and "cheer up" has in grief counselling. Telling someone they should do something is not the same thing as helping them do it.The problem is that the people needing handholding don’t understand just how much it is costing them and cant make an informed decision. Sooner or later this will change. Probably sooner.0 -

Perhaps you need the services of an IFA to guide you when it comes investing internationally.Deleted_User said:dunstonh said:Transparency - how did you get a figure of "easily £300k"? I ran a quick worksheet on the following assumptions:-

1. £30k starting salary at 30

2. 5% increase p.a.

3. 2% fee going into fund and 1/2% p.a.

4. 20% of income into pot

5. 2% growth after fees and 2.5% without any fees

6. At 65 £100k differenceOn point 3, an IFA cannot charge an initial fee beyond the first year So, they could charge 2% for 12 months but after that, the initial fee would be zero. Barely any providers have initial charges any more. On that scenario, a fee of around £500-£750 is likely. Taken fully in year one.

The best advice the IFA can give when someone is calling about market turbulence is “bug off”.But you wouldn't give them any advice on that follow up call as they are not paying you. Mrs Miggins used the method you prefer of transactional advice. So, the response to Mrs Miggins would be "I can tell you but it will cost you £x. However, if you dont pay, I won't tell you". Mrs Miggins then does exactly what that person did on another thread here from the other day and transfers it all to cash and it costs tens of thousands of pounds.

Is handholding a worthwhile service worth massive amounts of money?Its not just handholding.

You have no basis to say that the clients want this charging model.Yes we do. a) the model reflects what people want b) research time and again (including commissions by the regulator) fund that percentage was by far the most popular with consumers. c) hourly rates were the least popular with consumers.

So popular, they put clients money into platforms only accessible through advisors so its harder to just take over the portfolio you paid a fee to set up.IFA platforms can be cheaper than DIY platforms. Most DIY platforms don't accept intermediaries. Most IFA platforms will take instructions from a client if they dont have an adviser. Some cannot or they will increase their charge to cover the increased costs.

The clients don’t get to decide. At least not based on transparent information. If they were given options with clear illustrations of the impact the fees will have, it would be a different matter.You are not in this country. So, how can you say what disclosure is like in the UK? I suspect you are very out-of-date. Indeed, disclosure in the UK (and EU) has got so detailed and transparent that people can now suffer information overload. Ironically, I find the disclosures on the DIY side to be far less transparent. Just look at some fo the DIY platforms and the way they hide the TC & IC and only show the OCF. Or give a typical TC & IC rather than an actual.

Why do you believe a MIFIDII disclosure is not transparent?

am not entirely happy with the selection of ETFs (why can’t I buy US domiciled ETFs?) but its not the providers fault. The ETFs themselves are very transparent, I know exactly whats in them today.0 -

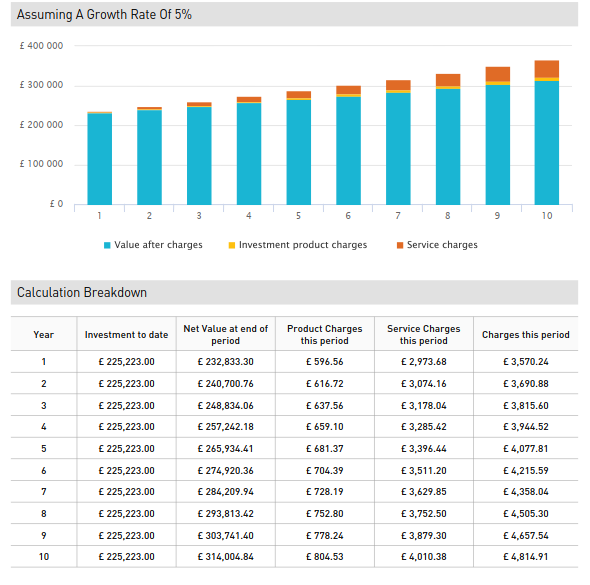

3. a) First of all, its not “your portfolio”. Its your client’s with third parties doing stock-picking for you . And you are rare if not unique. Assuming you pick active funds, worldwide they have underperformed for quite a while. How about we do a forward test based on a given level of FI? Items B and C - ok so its a bad system. I am not saying its IFA’s fault.dunstonh said:3. DIY platforms don’t need to accept intermediaries. An advisor can advise. And the advice could be: “put your money into the cheapest DIY platform, buy a simple well diversified portfolio or fund, keep adding more money and sleep well”.Why would I want to do that? a) our portfolios have consistently outperformed multi-asset funds after charges. So, why would I want to put the client in something worse? b) the adviser fee would become VATable as it is no longer intermediary business. c) it prevents the adviser from complying with regulatory requirements as the DIY platforms do not meet the required standards that advice has to meet.4. You are right, I have not seen recent disclosures. You have. So can you help me? Can you provide an example of the disclosure illustrating the impact of ongoing IFA fees on the final value of the pot, similar to the examples provided above? Do the disclosure materials promote the value of simplicity?Ongoing charges are included in all charges disclosures. And since 1994, the effect of charges over the term (for retirement that would be selected retirement age) have been required to be included in the illustration. MIFDII made some changes to that and introduced IC & TC. So, now you get a breakdown showing platform charge, adviser charges, OCF/TER, TC & IC (IC sometimes being referred to as other). For life and pension investments, you get projections showing the impact of charges to a defined term. For ISAs or unwrapped you get a defined period that can vary with platforms/providers. Here is an example:

Promotion of simplicity should certainly not be included as that is a choice. A choice that may or may not be the right option for an individual. Options that are not suitable should not be promoted.5. I opened a new SIPP less than 12 months ago. Everything was transparent. The Platform costs me less than 0.1% on a 130k fund. The charges do not increase with the pot. Charges are as advertised. Additional charges for moving money out, also advertised. I am not entirely happy with the selection of ETFs (why can’t I buy US domiciled ETFs?) but its not the providers fault. The ETFs themselves are very transparent, I know exactly whats in them today.It cannot recall where you are but if its within the EU then it will be because many US-domiciled ETFs do not provide charges details that are compliant with the distribution within the EU. Some ETF providers have decided they dont want to do that. It could be that they think there isn't the market vs the cost. It may be that they are not as transparent as you think and the standards required would disclose something they dont want to disclose (TC & IC became embarrassing for some fund houses)

What you have done would be equally transparent in the UK. Whether the charges were fixed cost, percentage or other.4. Thanks. Can you clarify something else for me please... Are they showing the projected charges? Thats what it looks like. The actual effect on the portfolio is massively larger. Certainly the past valuation table is not showing the effect charges had on this portfolio. The real question: what your portfolio would be worth without service charges snd assuming the same gross growth rate at the end of 30 years (typical outlook)?

I live in Canada but the SIPP I referenced is an account I set up in Britain. In Canada we can buy funds like VTI or VWO or Blackrock versions at lower costs and zero platform charges. More competition, lower costs, more options. Are you implying that VTI isn’t transparent? Really?0 -

We are not going to agree. Advisors understanding Canadian as well as British rules, taxes and investment vehicles are rare if in existence - and expensive. No point getting advice on a tiny portion of my overall portfolio. And I’ve done OK. At 0.18% charges on funds like EMIM are certainly higher than what I am used to but its tolerable.Thrugelmir said:

Perhaps you need the services of an IFA to guide you when it comes investing internationally.Deleted_User said:dunstonh said:Transparency - how did you get a figure of "easily £300k"? I ran a quick worksheet on the following assumptions:-

1. £30k starting salary at 30

2. 5% increase p.a.

3. 2% fee going into fund and 1/2% p.a.

4. 20% of income into pot

5. 2% growth after fees and 2.5% without any fees

6. At 65 £100k differenceOn point 3, an IFA cannot charge an initial fee beyond the first year So, they could charge 2% for 12 months but after that, the initial fee would be zero. Barely any providers have initial charges any more. On that scenario, a fee of around £500-£750 is likely. Taken fully in year one.

The best advice the IFA can give when someone is calling about market turbulence is “bug off”.But you wouldn't give them any advice on that follow up call as they are not paying you. Mrs Miggins used the method you prefer of transactional advice. So, the response to Mrs Miggins would be "I can tell you but it will cost you £x. However, if you dont pay, I won't tell you". Mrs Miggins then does exactly what that person did on another thread here from the other day and transfers it all to cash and it costs tens of thousands of pounds.

Is handholding a worthwhile service worth massive amounts of money?Its not just handholding.

You have no basis to say that the clients want this charging model.Yes we do. a) the model reflects what people want b) research time and again (including commissions by the regulator) fund that percentage was by far the most popular with consumers. c) hourly rates were the least popular with consumers.

So popular, they put clients money into platforms only accessible through advisors so its harder to just take over the portfolio you paid a fee to set up.IFA platforms can be cheaper than DIY platforms. Most DIY platforms don't accept intermediaries. Most IFA platforms will take instructions from a client if they dont have an adviser. Some cannot or they will increase their charge to cover the increased costs.

The clients don’t get to decide. At least not based on transparent information. If they were given options with clear illustrations of the impact the fees will have, it would be a different matter.You are not in this country. So, how can you say what disclosure is like in the UK? I suspect you are very out-of-date. Indeed, disclosure in the UK (and EU) has got so detailed and transparent that people can now suffer information overload. Ironically, I find the disclosures on the DIY side to be far less transparent. Just look at some fo the DIY platforms and the way they hide the TC & IC and only show the OCF. Or give a typical TC & IC rather than an actual.

Why do you believe a MIFIDII disclosure is not transparent?

am not entirely happy with the selection of ETFs (why can’t I buy US domiciled ETFs?) but its not the providers fault. The ETFs themselves are very transparent, I know exactly whats in them today.0 -

3. a) First of all, its not “your portfolio”. Its your client’s with third parties doing stock-picking for you . And you are rare if not unique. Assuming you pick active funds, worldwide they have underperformed for quite a while. How about we do a forward test based on a given level of FI? Items B and C - ok so its a bad system. I am not saying its IFA’s fault.

Third parties provide the asset allocations. We pick the funds to fill those weightings. The investments within the funds are controlled by investment managers. You assume wrong on the active funds side. We use active and passive in our portfolios. The ratio of passive to active varies across the risk profiles. More passive at the lower end and more active at the higher. You also make the mistake of assuming that all active funds perform badly. And we are neither unique or rare. I know that the anti-advice brigade don't like it but plenty of firms and DIY investors regularly return better than multi-asset funds like VLS.

4. Thanks. Can you clarify something else for me please... Are they showing the projected charges? Thats what it looks like. The actual effect on the portfolio is massively larger. Certainly the past valuation table is not showing the effect charges had on this portfolio. The real question: what your portfolio would be worth without service charges snd assuming the same gross growth rate at the end of 30 years (typical outlook)?Those are the projected charges. In this case, it used a 10 year timescale at 5% pa. However, the timescale is configurable. It could have been 2 years or 50 years. The effect is shown in the graph.

In Canada we can buy funds like VTI or VWO or Blackrock versions at lower costs and zero platform charges. More competition, lower costs, more options. Are you implying that VTI isn’t transparent? Really?I am not implying anything. I am just stating the factual reason as to why many US ETFs are not available within the EU. Why they refuse to comply with EU disclosure requirements is something that would likely vary with different fund houses. I mentioned no specific fund house or ETF.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0 -

My point was in reference to your lack of knowledge with regards to ETF's. What else are you basing assumption on rather than actual facts?Deleted_User said:

We are not going to agree. Advisors understanding Canadian as well as British rules, taxes and investment vehicles are rare if in existence - and expensive. No point getting advice on a tiny portion of my overall portfolio. And I’ve done OK. At 0.18% charges on funds like EMIM are certainly higher than what I am used to but its tolerable.Thrugelmir said:

Perhaps you need the services of an IFA to guide you when it comes investing internationally.Deleted_User said:dunstonh said:Transparency - how did you get a figure of "easily £300k"? I ran a quick worksheet on the following assumptions:-

1. £30k starting salary at 30

2. 5% increase p.a.

3. 2% fee going into fund and 1/2% p.a.

4. 20% of income into pot

5. 2% growth after fees and 2.5% without any fees

6. At 65 £100k differenceOn point 3, an IFA cannot charge an initial fee beyond the first year So, they could charge 2% for 12 months but after that, the initial fee would be zero. Barely any providers have initial charges any more. On that scenario, a fee of around £500-£750 is likely. Taken fully in year one.

The best advice the IFA can give when someone is calling about market turbulence is “bug off”.But you wouldn't give them any advice on that follow up call as they are not paying you. Mrs Miggins used the method you prefer of transactional advice. So, the response to Mrs Miggins would be "I can tell you but it will cost you £x. However, if you dont pay, I won't tell you". Mrs Miggins then does exactly what that person did on another thread here from the other day and transfers it all to cash and it costs tens of thousands of pounds.

Is handholding a worthwhile service worth massive amounts of money?Its not just handholding.

You have no basis to say that the clients want this charging model.Yes we do. a) the model reflects what people want b) research time and again (including commissions by the regulator) fund that percentage was by far the most popular with consumers. c) hourly rates were the least popular with consumers.

So popular, they put clients money into platforms only accessible through advisors so its harder to just take over the portfolio you paid a fee to set up.IFA platforms can be cheaper than DIY platforms. Most DIY platforms don't accept intermediaries. Most IFA platforms will take instructions from a client if they dont have an adviser. Some cannot or they will increase their charge to cover the increased costs.

The clients don’t get to decide. At least not based on transparent information. If they were given options with clear illustrations of the impact the fees will have, it would be a different matter.You are not in this country. So, how can you say what disclosure is like in the UK? I suspect you are very out-of-date. Indeed, disclosure in the UK (and EU) has got so detailed and transparent that people can now suffer information overload. Ironically, I find the disclosures on the DIY side to be far less transparent. Just look at some fo the DIY platforms and the way they hide the TC & IC and only show the OCF. Or give a typical TC & IC rather than an actual.

Why do you believe a MIFIDII disclosure is not transparent?

am not entirely happy with the selection of ETFs (why can’t I buy US domiciled ETFs?) but its not the providers fault. The ETFs themselves are very transparent, I know exactly whats in them today.

Everybody has done ok. Difficult not to have done. That's when complacency creeps in.0 -

@dunstonh

How do you identify that you consistently outperform multi-asset funds? There are a lot of them, all with varying equity ratios, risk ratios, let alone what sectors those equity ratios are invested in. Do you identify just 1 that is closest to a portfolio you manage and then compare? Or take an average?

0 -

What lack of knowledge with regards to ETFs? Can you be a little more specific?Thrugelmir said:

My point was in reference to your lack of knowledge with regards to ETF's. What else are you basing assumption on rather than actual facts?Deleted_User said:

We are not going to agree. Advisors understanding Canadian as well as British rules, taxes and investment vehicles are rare if in existence - and expensive. No point getting advice on a tiny portion of my overall portfolio. And I’ve done OK. At 0.18% charges on funds like EMIM are certainly higher than what I am used to but its tolerable.Thrugelmir said:

Perhaps you need the services of an IFA to guide you when it comes investing internationally.Deleted_User said:dunstonh said:Transparency - how did you get a figure of "easily £300k"? I ran a quick worksheet on the following assumptions:-

1. £30k starting salary at 30

2. 5% increase p.a.

3. 2% fee going into fund and 1/2% p.a.

4. 20% of income into pot

5. 2% growth after fees and 2.5% without any fees

6. At 65 £100k differenceOn point 3, an IFA cannot charge an initial fee beyond the first year So, they could charge 2% for 12 months but after that, the initial fee would be zero. Barely any providers have initial charges any more. On that scenario, a fee of around £500-£750 is likely. Taken fully in year one.

The best advice the IFA can give when someone is calling about market turbulence is “bug off”.But you wouldn't give them any advice on that follow up call as they are not paying you. Mrs Miggins used the method you prefer of transactional advice. So, the response to Mrs Miggins would be "I can tell you but it will cost you £x. However, if you dont pay, I won't tell you". Mrs Miggins then does exactly what that person did on another thread here from the other day and transfers it all to cash and it costs tens of thousands of pounds.

Is handholding a worthwhile service worth massive amounts of money?Its not just handholding.

You have no basis to say that the clients want this charging model.Yes we do. a) the model reflects what people want b) research time and again (including commissions by the regulator) fund that percentage was by far the most popular with consumers. c) hourly rates were the least popular with consumers.

So popular, they put clients money into platforms only accessible through advisors so its harder to just take over the portfolio you paid a fee to set up.IFA platforms can be cheaper than DIY platforms. Most DIY platforms don't accept intermediaries. Most IFA platforms will take instructions from a client if they dont have an adviser. Some cannot or they will increase their charge to cover the increased costs.

The clients don’t get to decide. At least not based on transparent information. If they were given options with clear illustrations of the impact the fees will have, it would be a different matter.You are not in this country. So, how can you say what disclosure is like in the UK? I suspect you are very out-of-date. Indeed, disclosure in the UK (and EU) has got so detailed and transparent that people can now suffer information overload. Ironically, I find the disclosures on the DIY side to be far less transparent. Just look at some fo the DIY platforms and the way they hide the TC & IC and only show the OCF. Or give a typical TC & IC rather than an actual.

Why do you believe a MIFIDII disclosure is not transparent?

am not entirely happy with the selection of ETFs (why can’t I buy US domiciled ETFs?) but its not the providers fault. The ETFs themselves are very transparent, I know exactly whats in them today.

Everybody has done ok. Difficult not to have done. That's when complacency creeps in.When I said “I did ok”. I was referring to finding a reasonably cost efficient set of vehicles which go well with my overall portfolio.0 -

in respect of my post here, it was using VLS as I suspected that was the range being referred to (as is so often the case). There is a bit of an assumption with some here that VLS is the best thing for everyone and nothing can possibly be better. I do also use multi-asset funds (but no longer VLS) for transactional advice cases.Cus said:@dunstonh

How do you identify that you consistently outperform multi-asset funds? There are a lot of them, all with varying equity ratios, risk ratios, let alone what sectors those equity ratios are invested in. Do you identify just 1 that is closest to a portfolio you manage and then compare? Or take an average?I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

“ am not implying anything. I am just stating the factual reason as to why many US ETFs are not available within the EU. Why they refuse to comply with EU disclosure requirements is something that would likely vary with different fund houses. I mentioned no specific fund house or ETF.”This is wrong. US ETFs are required to be completely open about their holdings. Passive are passive, so holdings are known. Active ETFs are required to publish holdings daily. It does not get more transparent. https://www.sec.gov/investor/alerts/etfs.pdf0

![[Deleted User]](https://us-noi.v-cdn.net/6031891/uploads/defaultavatar/nFA7H6UNOO0N5.jpg)

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.3K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards