We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Retirement Planner - Importance of Inflation?

Comments

-

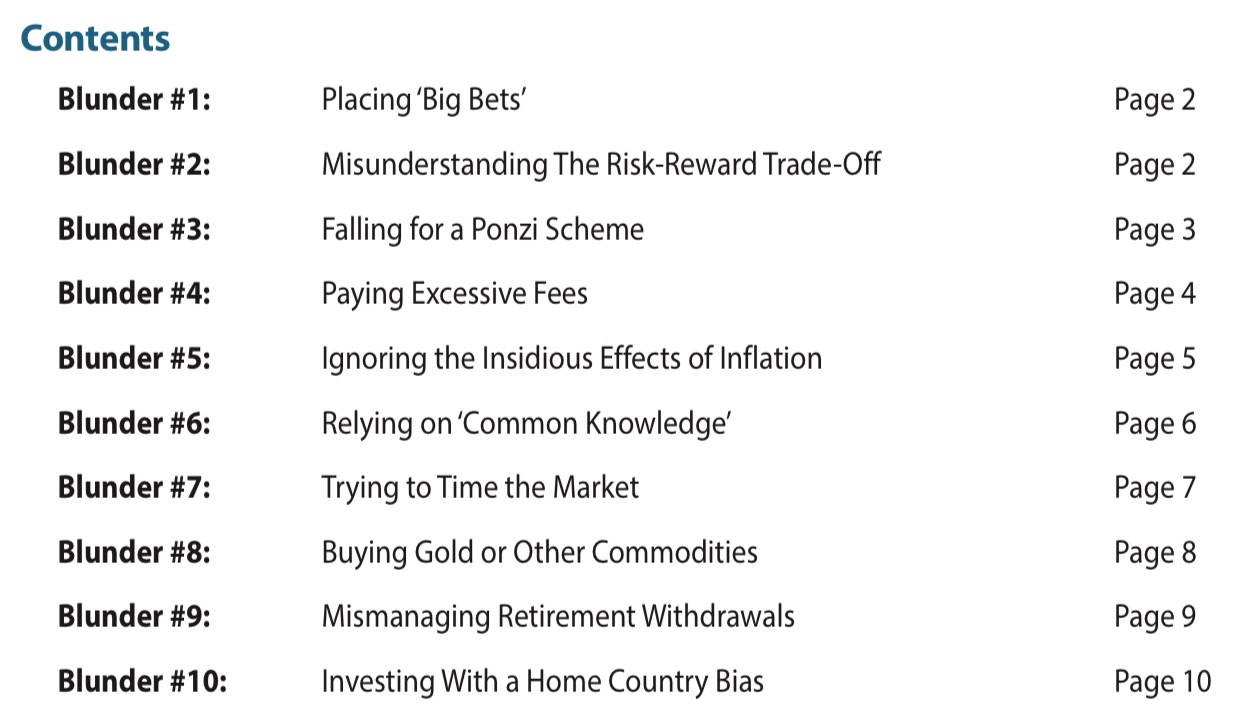

Just on this....another mildly irritating Fisher Investments advert trickled into my bookface feed this morning, but I thought I would pass them some mildly inaccurate personal details & read it.GSP said:Just how important is inflation in retirement planner’s?Title is “Ten Retirement Investment Blunders to Avoid”Headlines are these: There you go: don’t make blunder #5!

There you go: don’t make blunder #5!

I can’t easily post the link, but googling it, I find their website offers 13 blunders to avoid...wonder which 3 they left out for bookface readers

eta - ahhh, that was for ‘Mericans......

update2: it was a short read, mostly obvious. I did enjoy this quote though:

remember what the legendary US investor Benjamin Graham once said: ‘In the short run, the market is a voting machine, but in the long run, it is a weighing machine.’Plan for tomorrow, enjoy today!2 -

You can't run out of money as your SP is with you for life (and you have a large pension pot). I, personally, don't see how an extra £3k a year SP (on top of a lets say £300k pension pot) is going to make a significant difference against the a sudden and unexpected need for money later in life. Even at the 6% (not 10%) I used in the example above the pot will still be growing each year (on average) if drawing down the equivalent to a boosted SP. There is no way I would be buying a private annuity as the SP is my annuity. There will be plenty in the pot / savings to pay for any emergency and of course if all that fails there are safety net strategies such as equity release or downsizing.Deleted_User said:

Its insurance against living too long and running out of money. Delaying SP by a year is a much better value than buying an annuity at the cost of 1 year SP. Your level of confidence in the 10% annual growth of your investments is very impressive.pensionpawn said:

Why defer your state pension? Yes your SP will increase by around 10% each year however you will then be depleting your private pension instead. This isn't for me as my investments should (are) growing near that rate and secondly, if you croak it before you start taking your pension you've lost a chunk of money that you could have passed to your estate.Stubod said:Assuming you are not too fussed about leaving loads to next of kin / charity, it makes sense to me to burn through your "pot" and defer the state pension, particularly if you are a little risk averse. I think it offers around 5% increase for each year deferred?

I'd be more interested in the opposite, taking your pension earlier at a reduced rate. Also, as with annuities, taking your pension at a reduced rate from your SP age which allows for a significant percentage to be passed onto your wife / husband.

Regarding my faith in continuing to achieve 10%, well as we all know past returns are no guarantee of future returns. That said you can assume that you will only achieve around 5% and feel obligated to pile more into your pension (cutting back on holidays with the kids, not pushing the boat out at Christmas etc) whilst you are working only to find you have excess cash in your 60s+ and less opportunity / energy to fully enjoy it. Or you can keep faith with how you've managed your pension planning over the previous decades, enjoy life to the full during the younger family years, and ease back in retirement if growth doesn't pan out as hoped. My father once said to me that he came into the good money too old (mid 60's in the mid 1980's) to enjoy it. I think we'll all agree it's getting the balance right and that's a very personal choice.2 -

Thanks for this. Interesting read. As well as 5., I was interested in 7 and 10 as well, but 2 ended up being important for me as well. In all, some are closely linked to one another.cfw1994 said:

Just on this....another mildly irritating Fisher Investments advert trickled into my bookface feed this morning, but I thought I would pass them some mildly inaccurate personal details & read it.GSP said:Just how important is inflation in retirement planner’s?Title is “Ten Retirement Investment Blunders to Avoid”Headlines are these:There you go: don’t make blunder #5!

I can’t easily post the link, but googling it, I find their website offers 13 blunders to avoid...wonder which 3 they left out for bookface readers

eta - ahhh, that was for ‘Mericans......

update2: it was a short read, mostly obvious. I did enjoy this quote though:

remember what the legendary US investor Benjamin Graham once said: ‘In the short run, the market is a voting machine, but in the long run, it is a weighing machine.’

First on 5. Yes, you can see the effect of inflation as we go on. But I think that perhaps this is where you need to strip out your regular bills, shopping, insurance etc, everything you HAVE to pay for year in year out from your desired withdrawal amount and run that with a 2% inflation calculation ahead. Mine is £17k and a long way in future it does not outstrip my withdrawal amount now. By then, I would probably be indoors getting through each day not spending outside regular bills, but would have SP as a back up as well.

Thinking about 2., this is very interesting as it occurred to me there is an element of double counting going here. I have not seen this mentioned, but it is my thought. In 2. it mentions about the pitfalls of too conservative investing and that you need a bit of risk for growth to counteract inflation. Well why is this being done here, then there are separate calculations for inflation too. It’s been addressed twice it appears. EDIT: Scrub that inflation doubl counting thought!

7. goes without saying. Don’t withdraw when a market or what I would say is your growth is down.

10. yes puts the argument between cautious and withdrawing too much.

0 -

1. In the real world you may or may not get 5% return. Or you may get more. But you certainly won’t get it every year. People in drawdown can’t handle volatility unless a) they are wealthy and can easily cut expenditure by half or more or b) have a lot of db type income to cushion volatility. Reliability and steady future income become more important than percent return. People without significant DB are forced into bonds (zero expected return) or annuity (very low rate). Delaying pension is a much better deal than either.pensionpawn said:

You can't run out of money as your SP is with you for life (and you have a large pension pot). I, personally, don't see how an extra £3k a year SP (on top of a lets say £300k pension pot) is going to make a significant difference against the a sudden and unexpected need for money later in life. Even at the 6% (not 10%) I used in the example above the pot will still be growing each year (on average) if drawing down the equivalent to a boosted SP. There is no way I would be buying a private annuity as the SP is my annuity. There will be plenty in the pot / savings to pay for any emergency and of course if all that fails there are safety net strategies such as equity release or downsizing.Deleted_User said:

Its insurance against living too long and running out of money. Delaying SP by a year is a much better value than buying an annuity at the cost of 1 year SP. Your level of confidence in the 10% annual growth of your investments is very impressive.pensionpawn said:

Why defer your state pension? Yes your SP will increase by around 10% each year however you will then be depleting your private pension instead. This isn't for me as my investments should (are) growing near that rate and secondly, if you croak it before you start taking your pension you've lost a chunk of money that you could have passed to your estate.Stubod said:Assuming you are not too fussed about leaving loads to next of kin / charity, it makes sense to me to burn through your "pot" and defer the state pension, particularly if you are a little risk averse. I think it offers around 5% increase for each year deferred?

I'd be more interested in the opposite, taking your pension earlier at a reduced rate. Also, as with annuities, taking your pension at a reduced rate from your SP age which allows for a significant percentage to be passed onto your wife / husband.

Regarding my faith in continuing to achieve 10%, well as we all know past returns are no guarantee of future returns. That said you can assume that you will only achieve around 5% and feel obligated to pile more into your pension (cutting back on holidays with the kids, not pushing the boat out at Christmas etc) whilst you are working only to find you have excess cash in your 60s+ and less opportunity / energy to fully enjoy it. Or you can keep faith with how you've managed your pension planning over the previous decades, enjoy life to the full during the younger family years, and ease back in retirement if growth doesn't pan out as hoped. My father once said to me that he came into the good money too old (mid 60's in the mid 1980's) to enjoy it. I think we'll all agree it's getting the balance right and that's a very personal choice.2. Spending more and “enjoying life” in early years is wonderful but the future isn’t a certainty. Its a probability. Living a long time increases your probability of running out of investments, particularly if you enjoy life a little too much early on. Standard or reduced pension isn’t fun if thats all you have. As we get older we tend to make errors in managing investments. Thats why a few extra quid in guaranteed and inflation linked DB income purchased at a very low market-beating cost is a great deal for most people.0 -

I too am putting a few things in place for my retirement in 6 yrs time. I was thinking of starting a retirement isa, (invest 4k and get 1k free.) as mentioned by someone on here earler.but you have to be under 50. so can't do that.0

-

#8 is a blunder?

Retired 1st July 2021.

This is not investment advice.

Your money may go "down and up and down and up and down and up and down ... down and up and down and up and down and up and down ... I got all tricked up and came up to this thing, lookin' so fire hot, a twenty out of ten..."0 -

clive0510 said:I too am putting a few things in place for my retirement in 6 yrs time. I was thinking of starting a retirement isa, (invest 4k and get 1k free.) as mentioned by someone on here earler.but you have to be under 50. so can't do that.

Eh? What have I missed?

Do you mean a lifetime ISA where you have to be under 40 to open one?How's it going, AKA, Nutwatch? - 12 month spends to date = 3.24% of current retirement "pot" (as at end December 2025)0 -

I Don't know. I googled it and found the government website about it. and I'm sure it said 50. In my case it dooesn't matter either way as I'm 60 next year. so I can't do it, which is why I'm looking at other things to do with my money.Sea_Shell said:clive0510 said:I too am putting a few things in place for my retirement in 6 yrs time. I was thinking of starting a retirement isa, (invest 4k and get 1k free.) as mentioned by someone on here earler.but you have to be under 50. so can't do that.

Eh? What have I missed?

Do you mean a lifetime ISA where you have to be under 40 to open one?0 -

Do they mention themselves in #4?cfw1994 said:

Just on this....another mildly irritating Fisher Investments advert trickled into my bookface feed this morning, but I thought I would pass them some mildly inaccurate personal details & read it.GSP said:Just how important is inflation in retirement planner’s?Title is “Ten Retirement Investment Blunders to Avoid”Headlines are these:There you go: don’t make blunder #5!

I can’t easily post the link, but googling it, I find their website offers 13 blunders to avoid...wonder which 3 they left out for bookface readers

eta - ahhh, that was for ‘Mericans......

update2: it was a short read, mostly obvious. I did enjoy this quote though:

remember what the legendary US investor Benjamin Graham once said: ‘In the short run, the market is a voting machine, but in the long run, it is a weighing machine.’2 -

GSP said:

In the fund, the overall figure is where you see real growth or loss and there are so many factors in there. Take that money out of fund and that’s where it becomes affected by inflation to pay bills etc.AlanP_2 said:But actual investment returns include inflation surely?

For example, inflation increases the price of your BT Broadband & TV package, which (assuming BT make a reasonably fixed %'age Nett Profit) will lead to higher reported profits down the line and thus in to Dividends and Share Price but the "value" to you of those £s has been reduced by the same inflation rate.

There'll be exceptions where particular investments make a real return over a period and some make a real loss as they fail to keep up with inflation but surely all that you are trying to achieve in your cashflow is an "average" or "indication" on how things could go over 10/20/30 years? You don't know whether your chosen investments will be in the former or the latter category.

In my cash flow I use Personal Expense Inflation of 4% applied to our projected spend, Cash Return of 1.5%, Investment Returns of 3% and CPI at 2.5% for DB / SP increases.

So I am planning on real returns of 0.5% from investments and a loss of -1% on cash.

If the plan looks like it will work with those assumptions then I'm happy as I wouldn't expect future returns to be as poor in reality.

To me, there are attempts to produce an inflation figure in funds themselves, where they are also visibly hit outside your fund in spending. Could be there is double counting for those using inflation in their fund calculations, only to be hit outside as well?Only if you take out many years worth. Over a year or so, unless inflation was massive you wont see any meaningful change.This whole thread seems to be big fuss over nothing. If you think growth will be 5% and inflation 2% then modelling 3%growth lets youydo all numbers in todays value which is far less confusing than looking say 10 years ahead to an amount of X and then decreasing it by the inflation rate over that period to work out what its actually worth in today's terms which is all that matters.1

https://www.youtube.com/watch?v=ntG50eXbBtc

https://www.youtube.com/watch?v=ntG50eXbBtc

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.3K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.9K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.4K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards