We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Please help - Loan anguish

Comments

-

Basically, there are two ways in which loans operate. The first way is where the entire loan balance, including interest, is shown as the opening balance. This balance is the sum of all the monthly payments added together, and reduces each month by the amount paid. This is usually the method used where the interest rate is fixed, which means that the overall amount payable is a certainty. If the loan is settled early then a rebate of the interest is applied based upon a statutory formula. People often describe this as 'front loading' and see it as somehow wrong or even illegal. It is not.

The second method is where the opening balance is simply the amount borrowed and interest is applied each month based upon the daily balance, which is obviously much higher in the early stages. This method is usually used where the interest rate is not fixed and can be varied by the lender during the term. Again a settlement figure is calculated using the same formula.

There is nothing inherently different about either method in terms of the amount payable either in total or if settled early.

The settlement formula can be found here however they are utterly confusing to most and often become the cause of a great deal of argument.

The bottom line is simply that the APR should be used to compare different loans without getting hung up about the way in which they are administered.1 -

This response. Concludes my thread.~Brock~ said:Basically, there are two ways in which loans operate. The first way is where the entire loan balance, including interest, is shown as the opening balance. This balance is the sum of all the monthly payments added together, and reduces each month by the amount paid. This is usually the method used where the interest rate is fixed, which means that the overall amount payable is a certainty. If the loan is settled early then a rebate of the interest is applied based upon a statutory formula. People often describe this as 'front loading' and see it as somehow wrong or even illegal. It is not.

The second method is where the opening balance is simply the amount borrowed and interest is applied each month based upon the daily balance, which is obviously much higher in the early stages. This method is usually used where the interest rate is not fixed and can be varied by the lender during the term. Again a settlement figure is calculated using the same formula.

There is nothing inherently different about either method in terms of the amount payable either in total or if settled early.

The settlement formula can be found here however they are utterly confusing to most and often become the cause of a great deal of argument.

The bottom line is simply that the APR should be used to compare different loans without getting hung up about the way in which they are administered.Thanks to all who responded, but I can’t ask for any more than what this forum member has responded with - exactly what I wanted to know.

thanks all0 -

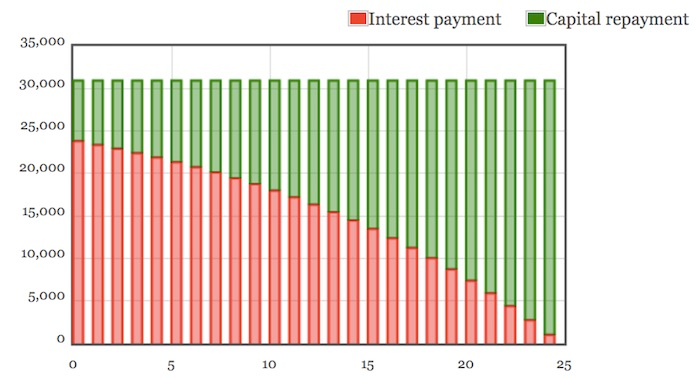

The image is a mortgage one but the principle is the same. Your payments are fixed but the proportion of that payment which is interest is very high at the beginning- this is not front loading though. You pay interest each month on the balance outstanding at that time - towards the end your balance is low so the interest is low and a bigger chunk of the outstanding balance is knocked off because your payment remains the same.I’m a Senior Forum Ambassador and I support the Forum Team on the Pensions, Annuities & Retirement Planning, Loans

The image is a mortgage one but the principle is the same. Your payments are fixed but the proportion of that payment which is interest is very high at the beginning- this is not front loading though. You pay interest each month on the balance outstanding at that time - towards the end your balance is low so the interest is low and a bigger chunk of the outstanding balance is knocked off because your payment remains the same.I’m a Senior Forum Ambassador and I support the Forum Team on the Pensions, Annuities & Retirement Planning, Loans

& Credit Cards boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com.

All views are my own and not the official line of MoneySavingExpert.1 -

So, you have not consolidated at all. You have taken out additional loans and doubled your debt, which is exactly what sourcrates' concern was.R.G said:

I haven’t paid the two Sainsbury’s loans off yet, no. The PO funds are sitting in my account and I’m thinking considering what to do.venison said:

Because it's never the best idea in the world to borrow money to repay borrowed money, I suppose the question should be have you repaid your two sainsburys loans and was the interest rate from the PO lower than that rate?R.G said:

Why the concern?sourcrates said:I’d be more worried about the decision to consolidate your debt than anything else.

A lender is a lender, they all operate under the terms of the consumer credit act, it’s pretty normal for everything to be done online these days, usually the terms are emailed to you.

The two Sainsbury’s loans are both at 3%. The total ‘settlement’, not balance, for both, combined, is £17,000, hence the new loan for £17,000.

At 3.4% with the new loan and the option to pay off early or overpay without charge, I don’t see the huge issue?!This new loan isn’t because I’m having to take it out to manage, it’s just to make things a little easier and if I over pay, I won’t be incurring much more interest.No free lunch, and no free laptop") 4

4 -

You’ve not understood.macman said:

So, you have not consolidated at all. You have taken out additional loans and doubled your debt, which is exactly what sourcrates' concern was.R.G said:

I haven’t paid the two Sainsbury’s loans off yet, no. The PO funds are sitting in my account and I’m thinking considering what to do.venison said:

Because it's never the best idea in the world to borrow money to repay borrowed money, I suppose the question should be have you repaid your two sainsburys loans and was the interest rate from the PO lower than that rate?R.G said:

Why the concern?sourcrates said:I’d be more worried about the decision to consolidate your debt than anything else.

A lender is a lender, they all operate under the terms of the consumer credit act, it’s pretty normal for everything to be done online these days, usually the terms are emailed to you.

The two Sainsbury’s loans are both at 3%. The total ‘settlement’, not balance, for both, combined, is £17,000, hence the new loan for £17,000.

At 3.4% with the new loan and the option to pay off early or overpay without charge, I don’t see the huge issue?!This new loan isn’t because I’m having to take it out to manage, it’s just to make things a little easier and if I over pay, I won’t be incurring much more interest.

I have two loans totalling £17,000.I have taken out another loan to pay these both off so I have one payment, not two. Which is better monthly for me.

Once I do this, there will be one payment and one loan.

But clearly, not £33,000 of debt, as the other two loans of 17,000 (which is their settlement figure combined) will not be in existence anymore.

I hope that clarifies things?!0 -

When you took out loan 1 and then loan 2, you did so presumably with the full intention of paying them off within the term you originally agreed right?

Fast forward to today, and you are now talking about extending them for many more additional years, both increasing the interest rate and the term thereby paying even more back in interest.

I appreciate that you aim to pay them off early in full, but what happens if in the next few years something else crops up, and again you start looking at credit agreements to fulfil that obligation? Now you have another loan on top of a loan that was a consolidation of two previous loans.....The maybe a few years later you are in the same boat but instead of having to consolidate 2 loans for £17,0000, you are, for example, looking to consolidate a £15,000 loan with another £10,000 loan. You are adamant this time will be different though, you will have them all paid off early and it will make things easier....except it doesn't as you continue to increase the monthly payment, making it harder and harder to save and pay off early.

I'm sure you can see where I am going with this. The reason we say it is because it's something we see time and time again, where people suddenly reach out having no idea how they ended up in over £50k worth of debt....

My strong advice is to cancel the loan, break the cycle before it even has time to think about developing, cut your costs and go hell for leather in paying down your two loans as two separate loans early as possible within the agreed terms.

Good luck with whatever you decide") 5

5 -

Nope, that’s fair advice and your points I cannot argue with as for many people, they will often extend, increase, replace old loans with new. But, that’s life.DrEskimo said:When you took out loan 1 and then loan 2, you did so presumably with the full intention of paying them off within the term you originally agreed right?

Fast forward to today, and you are now talking about extending them for many more additional years, both increasing the interest rate and the term thereby paying even more back in interest.

I appreciate that you aim to pay them off early in full, but what happens if in the next few years something else crops up, and again you start looking at credit agreements to fulfil that obligation? Now you have another loan on top of a loan that was a consolidation of two previous loans.....The maybe a few years later you are in the same boat but instead of having to consolidate 2 loans for £17,0000, you are, for example, looking to consolidate a £15,000 loan with another £10,000 loan. You are adamant this time will be different though, you will have them all paid off early and it will make things easier....except it doesn't as you continue to increase the monthly payment, making it harder and harder to save and pay off early.

I'm sure you can see where I am going with this. The reason we say it is because it's something we see time and time again, where people suddenly reach out having no idea how they ended up in over £50k worth of debt....

My strong advice is to cancel the loan, break the cycle before it even has time to think about developing, cut your costs and go hell for leather in paying down your two loans as two separate loans early as possible within the agreed terms.

Good luck with whatever you decide

Fast forward to today, and the world is in a place it’s never seen itself before. Even people like myself, who are very cautious and particular worrisome about change and making decisions like this, are having to.

I suspect that I will pay them their money back tomorrow as it really isn’t sitting well with me, and I’ll find another way.

I suspect that If I told you the circumstances of why this is the route I’ve gone down, and gave you all the facts, you’d probably agree that whilst being cautious, consolidating the two loans for now would be a viable option.

But then, we’re on a forum, and I’m not the desperate to lay bare my personal circumstances. After all, my initial question was pretty generic.

Thanks1 -

I have understood very well. Almost everyone who consolidates does so with the good intention of paying off the original debt. But the reality is that many then do not.R.G said:

You’ve not understood.macman said:

So, you have not consolidated at all. You have taken out additional loans and doubled your debt, which is exactly what sourcrates' concern was.R.G said:

I haven’t paid the two Sainsbury’s loans off yet, no. The PO funds are sitting in my account and I’m thinking considering what to do.venison said:

Because it's never the best idea in the world to borrow money to repay borrowed money, I suppose the question should be have you repaid your two sainsburys loans and was the interest rate from the PO lower than that rate?R.G said:

Why the concern?sourcrates said:I’d be more worried about the decision to consolidate your debt than anything else.

A lender is a lender, they all operate under the terms of the consumer credit act, it’s pretty normal for everything to be done online these days, usually the terms are emailed to you.

The two Sainsbury’s loans are both at 3%. The total ‘settlement’, not balance, for both, combined, is £17,000, hence the new loan for £17,000.

At 3.4% with the new loan and the option to pay off early or overpay without charge, I don’t see the huge issue?!This new loan isn’t because I’m having to take it out to manage, it’s just to make things a little easier and if I over pay, I won’t be incurring much more interest.

I have two loans totalling £17,000.I have taken out another loan to pay these both off so I have one payment, not two. Which is better monthly for me.

Once I do this, there will be one payment and one loan.

But clearly, not £33,000 of debt, as the other two loans of 17,000 (which is their settlement figure combined) will not be in existence anymore.

I hope that clarifies things?!

At the time of posting, you have not paid off the original loans and so your current debt is £33K, regardless of your future intentions.

A 'single monthly payment' is only better if the total amount due is less. Most consolidation loans simply do this by increasing the loan term, so the total debt is increased, even though the APR might be lower. In your case, you've swapped (once you do repay the original loans) two loans at 3% for one loan at 3.4%.No free lunch, and no free laptop3 -

The huge issue is that you now owe £34k and not £17kR.G said:

I haven’t paid the two Sainsbury’s loans off yet, no. The PO funds are sitting in my account and I’m thinking considering what to do.venison said:

Because it's never the best idea in the world to borrow money to repay borrowed money, I suppose the question should be have you repaid your two sainsburys loans and was the interest rate from the PO lower than that rate?R.G said:

Why the concern?sourcrates said:I’d be more worried about the decision to consolidate your debt than anything else.

A lender is a lender, they all operate under the terms of the consumer credit act, it’s pretty normal for everything to be done online these days, usually the terms are emailed to you.

The two Sainsbury’s loans are both at 3%. The total ‘settlement’, not balance, for both, combined, is £17,000, hence the new loan for £17,000.

At 3.4% with the new loan and the option to pay off early or overpay without charge, I don’t see the huge issue?!This new loan isn’t because I’m having to take it out to manage, it’s just to make things a little easier and if I over pay, I won’t be incurring much more interest.Vuja De - the feeling you'll be here later1 -

Are you having a wind up?pelirocco said:

The huge issue is that you now owe £34k and not £17kR.G said:

I haven’t paid the two Sainsbury’s loans off yet, no. The PO funds are sitting in my account and I’m thinking considering what to do.venison said:

Because it's never the best idea in the world to borrow money to repay borrowed money, I suppose the question should be have you repaid your two sainsburys loans and was the interest rate from the PO lower than that rate?R.G said:

Why the concern?sourcrates said:I’d be more worried about the decision to consolidate your debt than anything else.

A lender is a lender, they all operate under the terms of the consumer credit act, it’s pretty normal for everything to be done online these days, usually the terms are emailed to you.

The two Sainsbury’s loans are both at 3%. The total ‘settlement’, not balance, for both, combined, is £17,000, hence the new loan for £17,000.

At 3.4% with the new loan and the option to pay off early or overpay without charge, I don’t see the huge issue?!This new loan isn’t because I’m having to take it out to manage, it’s just to make things a little easier and if I over pay, I won’t be incurring much more interest.

Read the thread. There needs to be a transitional period where I have to get the new single amount, in my account, to pay the other two amounts off.

once this is done. One amount in one place of £17k plus interest.

regardless. As I HAVE ALSO SAID, which you have not read, is I’m giving PO their money back tomorrow morning.

0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.5K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.6K Work, Benefits & Business

- 603K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards