We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Pension Planning Query - Small Pot Recycling

ussdave

Posts: 390 Forumite

Just wondering if people can vet the below plan and point out anything I might have missed. Apologies for the long post - it's quite hard to describe everything without it turning into war and peace.

Currently 39 and a member of the USS pension scheme on approximately £52k (recent promotion). To date I have accrued £6k/year in (DB) benefits at retirement and a lump sum of 3x the pension amount (which I will forgo in order to increase my regular DB payment). Separately I also have £10k in the USS Investment Builder (DC), a S&S LISA with £1.5k and a normal S&S ISA which I've only recently opened.

The USS scheme is salary sacrifice at my University. I currently contribute 5% salary over the minimum, which is not matched, but with salary sacrifice seems like a no-brainer. I have experimented with higher contributions but have dropped to 5% recently whilst fudning marriage and a house move this year. Due to the combined DB/DC nature of the pension I will be able to draw a large amount of the DC Investment Builder fund completely tax free ((20 * DB yearly amount + Investment Builder amount ) * 25%).

My target retirement age will be around 58-60 with a take home pay of about £2k/month in today's money. I plan to be mortgage free by this point. My spouse is a few years younger, is a member of LGPS, has decent (similar) retirement benefits accrued so far and she will be increasing her contributions in a similar way to myself.

My plan is to increase my contributions gradually as my mortgage payments reduce, probably something like an additional ~2% of salary per year (on top of inflationary and promotion increases). As I want to bridge some years between leaving employment and drawing my DB pension I plan to periodically transfer money out of the Investment Builder part of the fund into a cheap SIPP. The idea with this is that I would end up with a SIPP I could draw the cash out of completely tax free whilst not working, supplimented with other savings (ISA initially, LISA at 60+). Assuming three years of drawdown and drawing only enough to remain below the tax threshold I believe that is approx £16k * 3 in today's money once you also include drawing 25% tax free each year.

Having also read up about how small pots work I'm considering additionally transfering out about 5k three times into separate SIPPs which would then be drawn as small pots from the age 57/58. The amount drawn would be tax free on the way in, 25% tax free and 75% taxed at normal rate on the way out and I believe does not impact MPAA. This money would then fund day to day living whilst I increased my salary sacrifice contributions so I could effectively recover the tax on the 75% portion that is taxed on withdrawal. From what I've read, this does not count as pension recyling as small pots are exempt from this.

The DB pension drawn from 60 is forecast to hit about 20k/year in today's money, plus I would have about £70-90k tax free when I took it. To bridge between my finishing date and 60 I will have funded the separate 'main' SIPP and my LISA and ISA to cover the difference between my target income and actual income, at least until state pension age.

State pension forecast is that I will have sufficient credits by the time I retire. My spouse may not quite hit the maximum so we'll review that and make voluntary additional payments if appropriate/we are allowed to.

Investments are all in high risk/global-equity-heavy funds at the moment as I won't be drawing on them for ~20 years. I will probably evaluate the risk level in a decade or so.

Does the above sound reasonable to everyone? Is there anything in there that I've misunderstood or is illegal? The small pots thing I'm especially concerned about.

Currently 39 and a member of the USS pension scheme on approximately £52k (recent promotion). To date I have accrued £6k/year in (DB) benefits at retirement and a lump sum of 3x the pension amount (which I will forgo in order to increase my regular DB payment). Separately I also have £10k in the USS Investment Builder (DC), a S&S LISA with £1.5k and a normal S&S ISA which I've only recently opened.

The USS scheme is salary sacrifice at my University. I currently contribute 5% salary over the minimum, which is not matched, but with salary sacrifice seems like a no-brainer. I have experimented with higher contributions but have dropped to 5% recently whilst fudning marriage and a house move this year. Due to the combined DB/DC nature of the pension I will be able to draw a large amount of the DC Investment Builder fund completely tax free ((20 * DB yearly amount + Investment Builder amount ) * 25%).

My target retirement age will be around 58-60 with a take home pay of about £2k/month in today's money. I plan to be mortgage free by this point. My spouse is a few years younger, is a member of LGPS, has decent (similar) retirement benefits accrued so far and she will be increasing her contributions in a similar way to myself.

My plan is to increase my contributions gradually as my mortgage payments reduce, probably something like an additional ~2% of salary per year (on top of inflationary and promotion increases). As I want to bridge some years between leaving employment and drawing my DB pension I plan to periodically transfer money out of the Investment Builder part of the fund into a cheap SIPP. The idea with this is that I would end up with a SIPP I could draw the cash out of completely tax free whilst not working, supplimented with other savings (ISA initially, LISA at 60+). Assuming three years of drawdown and drawing only enough to remain below the tax threshold I believe that is approx £16k * 3 in today's money once you also include drawing 25% tax free each year.

Having also read up about how small pots work I'm considering additionally transfering out about 5k three times into separate SIPPs which would then be drawn as small pots from the age 57/58. The amount drawn would be tax free on the way in, 25% tax free and 75% taxed at normal rate on the way out and I believe does not impact MPAA. This money would then fund day to day living whilst I increased my salary sacrifice contributions so I could effectively recover the tax on the 75% portion that is taxed on withdrawal. From what I've read, this does not count as pension recyling as small pots are exempt from this.

The DB pension drawn from 60 is forecast to hit about 20k/year in today's money, plus I would have about £70-90k tax free when I took it. To bridge between my finishing date and 60 I will have funded the separate 'main' SIPP and my LISA and ISA to cover the difference between my target income and actual income, at least until state pension age.

State pension forecast is that I will have sufficient credits by the time I retire. My spouse may not quite hit the maximum so we'll review that and make voluntary additional payments if appropriate/we are allowed to.

Investments are all in high risk/global-equity-heavy funds at the moment as I won't be drawing on them for ~20 years. I will probably evaluate the risk level in a decade or so.

Does the above sound reasonable to everyone? Is there anything in there that I've misunderstood or is illegal? The small pots thing I'm especially concerned about.

0

Comments

-

Yes, recycling only limits the Pension Commencement Lump Sum (usual 25%) and no part of a small pot is PCLS by definition. No MPAA either because only flexible withdrawing triggers that an again by definition small pots aren't. Not sure why you'd do 5k instead of 10k.ussdave said:Having also read up about how small pots work I'm considering additionally transfering out about 5k three times into separate SIPPs which would then be drawn as small pots from the age 57/58. The amount drawn would be tax free on the way in, 25% tax free and 75% taxed at normal rate on the way out and I believe does not impact MPAA. This money would then fund day to day living whilst I increased my salary sacrifice contributions so I could effectively recover the tax on the 75% portion that is taxed on withdrawal. From what I've read, this does not count as pension recyling as small pots are exempt from this.0 -

Apologies, forgot to include the reasoning in this.jamesd said:

Yes, recycling only limits the Pension Commencement Lump Sum (usual 25%) and no part of a small pot is PCLS by definition. No MPAA either because only flexible withdrawing triggers that an again by definition small pots aren't. Not sure why you'd do 5k instead of 10k.ussdave said:Having also read up about how small pots work I'm considering additionally transfering out about 5k three times into separate SIPPs which would then be drawn as small pots from the age 57/58. The amount drawn would be tax free on the way in, 25% tax free and 75% taxed at normal rate on the way out and I believe does not impact MPAA. This money would then fund day to day living whilst I increased my salary sacrifice contributions so I could effectively recover the tax on the 75% portion that is taxed on withdrawal. From what I've read, this does not count as pension recyling as small pots are exempt from this.

For the USS Investment Builder pot you have to transfer the entire pot when you move money out of it. Due to that and the benefits of salary sacrifice it makes sense to me to move the small pot(s) money out early on. Therefore I am concerned if I transfer too much the pot may grow beyond the 10k limit. I also figure that if, when it comes to withdrawal, the figure is below 10k I'll add the remainder to it through other savings.

I guess the other key part of this that I've not really made clear is that I'm trying to make the most of salary sacrifice for all pension contributions. Hence going for this slightly awkward approach rather than just opening various pots and contributing directly.0 -

I wouldnt worry too much about exceeding £10k.ussdave said:

Apologies, forgot to include the reasoning in this.jamesd said:

Yes, recycling only limits the Pension Commencement Lump Sum (usual 25%) and no part of a small pot is PCLS by definition. No MPAA either because only flexible withdrawing triggers that an again by definition small pots aren't. Not sure why you'd do 5k instead of 10k.ussdave said:Having also read up about how small pots work I'm considering additionally transfering out about 5k three times into separate SIPPs which would then be drawn as small pots from the age 57/58. The amount drawn would be tax free on the way in, 25% tax free and 75% taxed at normal rate on the way out and I believe does not impact MPAA. This money would then fund day to day living whilst I increased my salary sacrifice contributions so I could effectively recover the tax on the 75% portion that is taxed on withdrawal. From what I've read, this does not count as pension recyling as small pots are exempt from this.

For the USS Investment Builder pot you have to transfer the entire pot when you move money out of it. Due to that and the benefits of salary sacrifice it makes sense to me to move the small pot(s) money out early on. Therefore I am concerned if I transfer too much the pot may grow beyond the 10k limit. I also figure that if, when it comes to withdrawal, the figure is below 10k I'll add the remainder to it through other savings.

I guess the other key part of this that I've not really made clear is that I'm trying to make the most of salary sacrifice for all pension contributions. Hence going for this slightly awkward approach rather than just opening various pots and contributing directly.

You can transfer £30k to a well known SIPP provider in Bristol") and they will create 3 small pots of exactly £10k for you to take as and when required.

and they will create 3 small pots of exactly £10k for you to take as and when required.

Other providers are available who may also oblige.

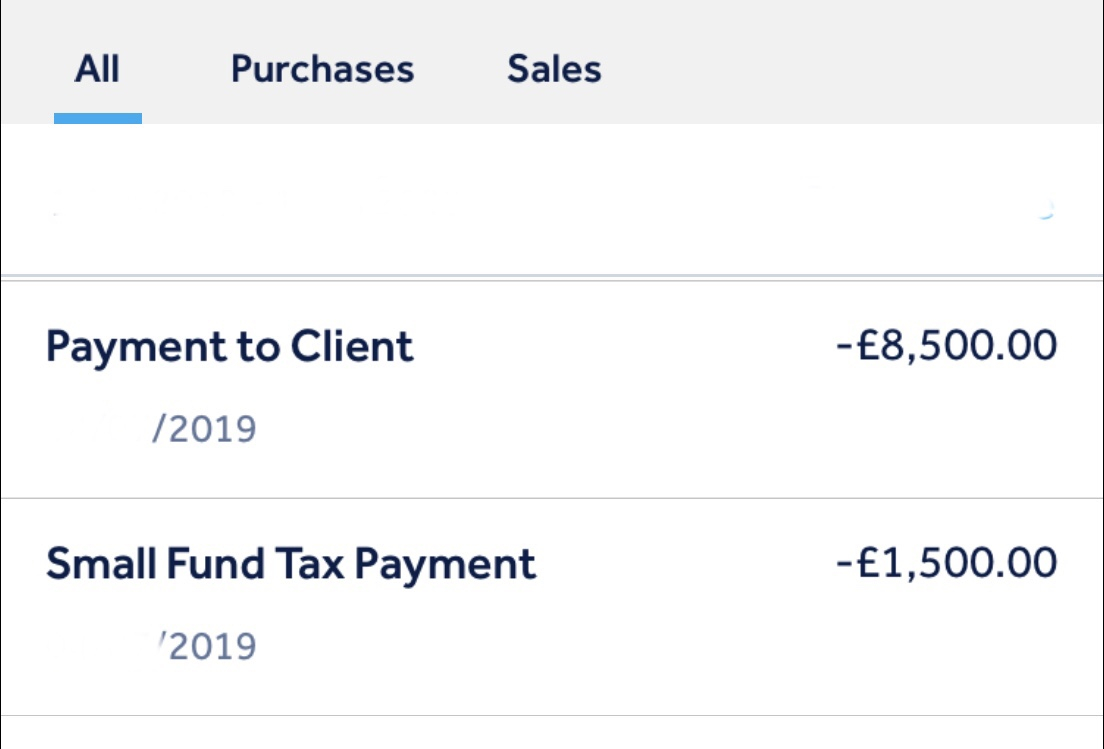

£10,000 small pot gives £2,500 tax free cash, £1,500 basic rate tax (default rate for small pots) and £6,000 net payment so £8,500 to yourself and £1,500 to HMRC.

3 -

I admire your long term planning, but the chances of things being the same in 2 years, never mind 20+ years, must be pretty small!0

-

@garmeg

That's interesting to know, thank you So I suppose I can make this a bit easier and just do a single larger transfer out of USS Investment Builder (which as mentioned, requires you to transfer the full pot out at once). Then I can transfer out almost the exact amount required for the small pots using the "well known SIPP provider in Bristol".

@Brynsam

Very true. In fact, the USS pension is almost certainly going to be dramatically overhauled in the next few years, not to mention any other pension law changes...and my circumstances/job could change.

Planning to try to optimise what is available to me now makes me feel a bit better though - even if I have to then adapt that later. Also fact-checking what I think I've understood from my research is quite handy 0 -

I am really struggling to see what benefit you hope to achieve with an early transfer out from the Investment Builder DC part. The IB itself offers all the benefits of a SIPP - flexible drawdown according to the usual DC scheme rules (from the age of probably 57+ for you), and can be taken earlier than your DB benefits. There is a good range of investment funds to suit almost all risk profiles, including some private equity investments which are not easily available in other funds. Plus it offers the best option for the largest tax-free lump sum by offering 25% of your total DC+DB equivalent value.What I do see in your plan is a benefit to the SIPP manager and fund managers at your expense as they will charge you fees and ongoing charges, otherwise be paid by the USS.0

-

In order to benefit from the 25% tax free for the combined DC + DB you have to take the DC and DB benefits at the same time - with acturial reduction of the DB part assuming that I'd be drawing it at 58-60ish.slithy_tove said:I am really struggling to see what benefit you hope to achieve with an early transfer out from the Investment Builder DC part. The IB itself offers all the benefits of a SIPP - flexible drawdown according to the usual DC scheme rules (from the age of probably 57+ for you), and can be taken earlier than your DB benefits. There is a good range of investment funds to suit almost all risk profiles, including some private equity investments which are not easily available in other funds. Plus it offers the best option for the largest tax-free lump sum by offering 25% of your total DC+DB equivalent value.What I do see in your plan is a benefit to the SIPP manager and fund managers at your expense as they will charge you fees and ongoing charges, otherwise be paid by the USS.

If it weren't for this point I'd pretty much go with leaving everything in the USS IB fund as, as you say, charges are mostly paid for within the USS funds.

To note though, I do still plan to have the USS IB fund topped up over the remaining years to achieve the maximum tax free cash I can for when I do draw those funds.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.9K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards