We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

750k Drawdown at 58

Comments

-

It's routine to have nothing but the state pension. I don't know whether that firm or other have changed practice. It is currently an exceptionally good time to transfer and has been excellent for a decade or so, mainly because of the effect of low interest rates on transfers. Most public sector schemes not included.GSP said:Heard a comment from another FA I was playing against who said if I tried for a transfer now I probably wouldn’t get it as I have no other income. Whether that’s true still, or ever was?

The main drawdown threat at the moment looks like a more sustained crash than we saw earlier this year and that's why I included a caution in the first post of the SWR thread.

Crashes in general tend to recover over a year or two. The government responses were notably better than the pretty good ones in 2008, when we were fortunate to have an expert in crashes as chairman of the Federal Reserve. The crash and go nowhere one I illustrated is at the exceptional end.

Looking longer term BritishInvestor used the US limiting case: sustained high inflation, which is what Bill Bengen - 4% rule person - has written worries him the most in drawdown. However:

1. around 90% of all annuities sold are level, no inflation increases.

2. defined benefit schemes normally have a portion with no inflation increases and a 5% cap is by far the most common for the rest

Those two sets, particularly the annuitants, will be severely affected by high inflation. Drawdown offers a couple or three advantages:

3. your loss isn't irreversible, you benefit from later, better, times

4. you can invest globally, potentially in places with less inflation

5. you can defer your state pension, paying yourself out of the drawdown pot while you do

Some of the safest types of income in this situation are:

6. unfunded public sector pensions, which typically have unlimited inflation increases

7. the state pension has uncapped inflation increases though it is possible in theory to change this

The state pension safety in times of high inflation is one of the many reasons why I typically suggest deferring. You can put yourself in a very secure position if it covers your core spending.

2 -

To put that into context:Thrugelmir said:The economic and financial realities of the impact of Covid are going to take time to sink in. This is by far the worst crisis in a hundred years. There can only be a rocky road ahead.

WW1 killed 867,829 to 1,011,687 in UK and colonies, 1.91% to 2.23% of prewar population.

1918 flu pandemic killed around 250k more in just Britain.

WW2 killed 450,900, 0.94% of prewar population in UK and Crown colonies as well as destroying much economic infrastructure.

Covid is nasty but it's not as bad, at least so far. It's very far from being the worst crisis in the last hundred years and while there are rocks around we've seen worse and drawdown safe withdrawal rates have been set to handle them.7 -

I'll answer inline - hopefully it will be readablejamesd said:

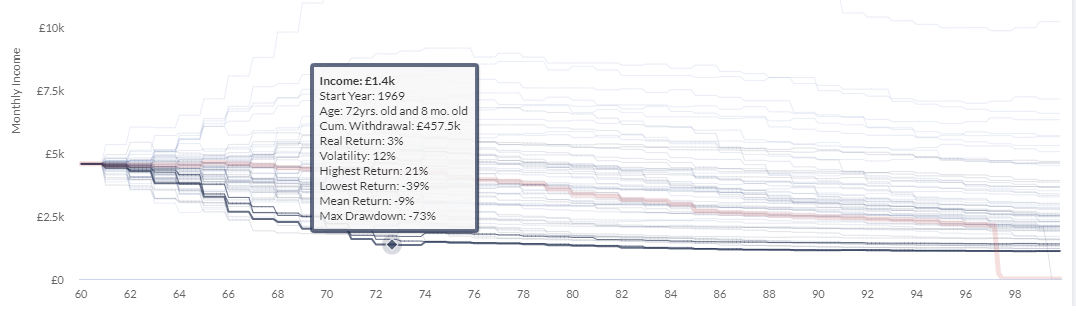

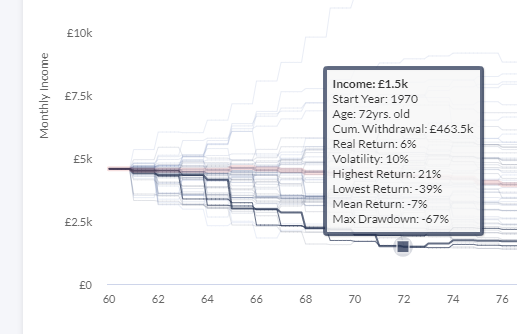

1969 start so that looks like the US worst case sequence that sets the 4% rule safemax there (for others, safemax is the highest income that in all of the sequences doesn't run out of money). Did you really start that one at about 4.8k monthly income with a 500k pot, an initial withdrawal rate of about 57.6k, 11.5%? Or maybe you started with a million?BritishInvestor said:

I take your point on the lower pessimism but I still think the potential drops in real income must be emphasised and could (if we use history as a guide) be worse than your illustration above. For example, historical worse case I see real income decimated if someone had followed that approach in the late 60s and had to live through the 70s inflationary/market slump horror.jamesd said:A fairly severe worked example might be a 40% equity drop in a 65:35 £500k mixture followed by nil investment growth and nil inflation (a simplifying alternative to 2% each). 5.5% initial, upper guard rail 20% higher at 6.6%, lower (prosperity) 20% lower is 4.4%. For comparison 4% rule (UK 30 years before costs) at 3.7% is £18,500 and an age 55 single life RPI annuity with 5 year guarantee quotes 1.624% which on £500,000 is £8,120. This initially looks like:

Year 1 take 5.5%, £27,500 and see equity drop, ending value £370,000.

...

Year 10 planned £14,613 is 6.7% so reduce to £13,151. Final value £206,606. (4% rule final value £212,500).

...

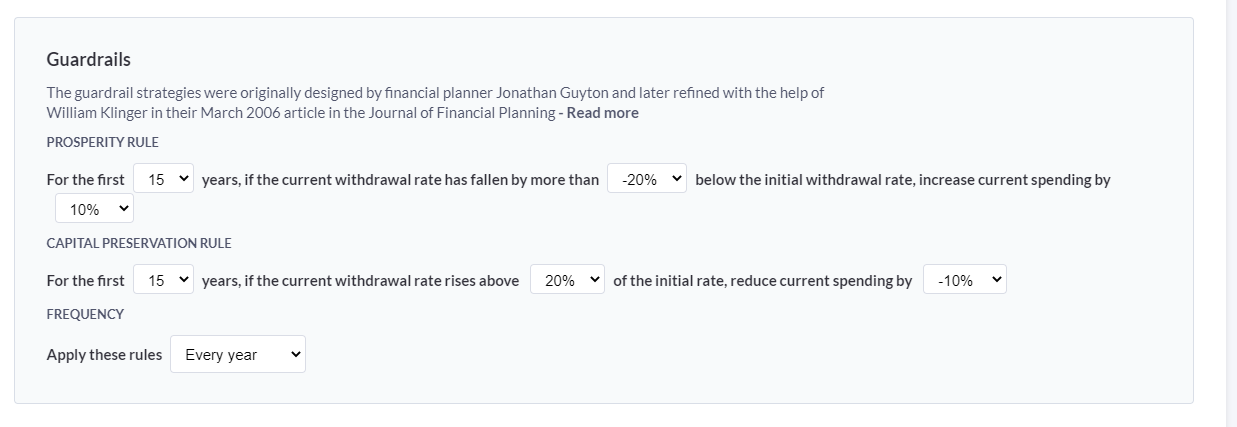

Personally I like the lower initial pessimism of Guyton-Klinger because it tends to favour higher income at younger ages, which is desirable if age-related spending decrease is expected.

As an aside I don't see 5.5% being sustainable which is odd as I'm using Abraham's tool - could be a different dataset he was using back then but just goes to show how sensitive the approach can be.

More than just decimated, that looks like a decimation in all but one of the initial years (using the kill one in ten of a Roman legion punishment meaning). It's the sort of sequence that led Klinger to use 20% in his followup work, if I remember that correctly.

Does that tool include the 20% cut if over the upper guardrail variation? It'd be interesting to observe how their cash flows and minimums differ if you fancy doing that.

I agree that there needs to be understanding of the drop potential. In some of my posts to individuals you'll see me noting the lowest, observing that it goes below target (or DB) and adjusting the constraints to increase it - usually a minimum income constraint in cfiresim for those, which cuts initial income. It's the sort of discussion I'd want to see an IFA having with their client and perhaps covering how that went in their reasons why document.

What success rate are you using with Abraham's tool? To get 5.5% he may have used 95% to skip the UK pre-WW2 worst case yet I don't see that mentioned in his The golden rule: working out a safe withdrawal rate. But it could just be a difference in the data set. But I describe 5.5% as with 90% success rate, which I assume I got from a blog post of his that also ended up at 5.5%. Incidentally, there he wrote "the highest percentage of the initial portfolio, indexed with inflation, which can be withdrawn without running out of money over a 30-year period. More than 100 years of market data for a 60/40 portfolio puts the SWR for the UK at 3.7%" and that's a convenient reference for the UK 3.7% before costs that a normally use.")

"1969 start so that looks like the US worst case sequence that sets the 4% rule safemax there"

That was the worst case in terms of real income falls after 12 years, but the worst case in terms of money running out in this scenario is Apr 1955.

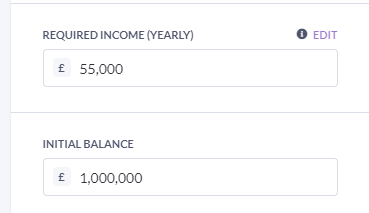

"Did you really start that one at about 4.8k monthly income with a 500k pot, an initial withdrawal rate of about 57.6k, 11.5%? Or maybe you started with a million?"

£1m @5.5%

"Does that tool include the 20% cut if over the upper guardrail variation?"

10% cut

It'd be interesting to observe how their cash flows and minimums differ if you fancy doing that.

"It's the sort of discussion I'd want to see an IFA having with their client and perhaps covering how that went in their reasons why document."

Yes I agree, but I'm not sure what the takeup of Timeline is amongst the adviser community to date. Someone whose views I respect estimated that around 1 in 20 adviser undertake the financial planning exercise "properly", and given retirement planning is a specialised subset of that I'd expect that number to be lower.

"What success rate are you using with Abraham's tool?

For real-world cases a starting point of 80-90% as per Abraham's suggestion, but that's just a starting point.

https://finalytiq.co.uk/longevity/

"To get 5.5% he may have used 95% to skip the UK pre-WW2 worst case yet I don't see that mentioned in his The golden rule: working out a safe withdrawal rate. But it could just be a difference in the data set"

Definitely possible that Abraham may have had different data sets back in 2015 than what is now in Timeline and indeed a slightly different approach to how he did this. Certainly since I've been using Timeline the product has changed enormously in terms of functionality.

"But I describe 5.5% as with 90% success rate, which I assume I got from a blog post of his that also ended up at 5.5%."

It may even be a tad more as I'm seeing 99% (for global equity and bond, UK investments might be slightly different)

"Incidentally, there he wrote "the highest percentage of the initial portfolio, indexed with inflation, which can be withdrawn without running out of money over a 30-year period. More than 100 years of market data for a 60/40 portfolio puts the SWR for the UK at 3.7%" and that's a convenient reference for the UK 3.7% before costs that a normally use."

I'd have to check that, but typically my timescales are closer to 40 years.

More than happy at some point run some Timeline numbers and compare to cFireSim, but as with all these things I think reading around the subject and really understanding it (as you have obviously done) has got to be the starting point for someone on this journey.

(Hopefully the above is clear - was a bit rushed as am on family duty today!!)0 -

Yep, so important to understand the historical market outcomes that have given us the SWR numbers.jamesd said:

To put that into context:Thrugelmir said:The economic and financial realities of the impact of Covid are going to take time to sink in. This is by far the worst crisis in a hundred years. There can only be a rocky road ahead.

WW1 killed 867,829 to 1,011,687 in UK and colonies, 1.91% to 2.23% of prewar population.

1918 flu pandemic killed around 250k more in just Britain.

WW2 killed 450,900, 0.94% of prewar population in UK and Crown colonies as well as destroying much economic infrastructure.

Covid is nasty but it's not as bad, at least so far. It's very far from being the worst crisis in the last hundred years and while there are rocks around we've seen worse and drawdown safe withdrawal rates have been set to handle them.

Just equities here, but bonds have also had some tough times (1915 etc)

https://finalytiq.co.uk/lessons-118-years-capital-market-return-data/

1 -

Indeed.jamesd said:

To put that into context:Thrugelmir said:The economic and financial realities of the impact of Covid are going to take time to sink in. This is by far the worst crisis in a hundred years. There can only be a rocky road ahead.

WW1 killed 867,829 to 1,011,687 in UK and colonies, 1.91% to 2.23% of prewar population.

1918 flu pandemic killed around 250k more in just Britain.

WW2 killed 450,900, 0.94% of prewar population in UK and Crown colonies as well as destroying much economic infrastructure.

Covid is nasty but it's not as bad, at least so far. It's very far from being the worst crisis in the last hundred years and while there are rocks around we've seen worse and drawdown safe withdrawal rates have been set to handle them.

Thruglemir is always a ray of sunshine & unbridled optimism on these boards, eh

For my part, I believe the world is a VERY different place than it was 100 years ago. Sure, there are and will be dips, and maybe we are entering a period of flatness, but where some businesses and sectors will struggle or fail, others will rise up.Plan for tomorrow, enjoy today!0 -

Out of interest ... has anyone looked at rates of inflation in the context of investment and interest rate returns? I would guess that investment returns wouldn’t be great, but I recall much higher interest rates during periods of high inflation. Just wondering what the ‘real’ margin might be?jamesd said:Looking longer term BritishInvestor used the US limiting case: sustained high inflation, which is what Bill Bengen - 4% rule person - has written worries him the most in drawdown. However:

1. around 90% of all annuities sold are level, no inflation increases.

2. defined benefit schemes normally have a portion with no inflation increases and a 5% cap is by far the most common for the rest

Those two sets, particularly the annuitants, will be severely affected by high inflation. Drawdown offers a couple or three advantages:

3. your loss isn't irreversible, you benefit from later, better, times

4. you can invest globally, potentially in places with less inflation

5. you can defer your state pension, paying yourself out of the drawdown pot while you do

Some of the safest types of income in this situation are:

6. unfunded public sector pensions, which typically have unlimited inflation increases

7. the state pension has uncapped inflation increases though it is possible in theory to change this

The state pension safety in times of high inflation is one of the many reasons why I typically suggest deferring. You can put yourself in a very secure position if it covers your core spending.0 -

The one certainty is we are on totally different pages. As the number of deaths didn't even cross my mind. I'll happily leave history to write safe withdrawl rates.jamesd said:

To put that into context:Thrugelmir said:The economic and financial realities of the impact of Covid are going to take time to sink in. This is by far the worst crisis in a hundred years. There can only be a rocky road ahead.

WW1 killed 867,829 to 1,011,687 in UK and colonies, 1.91% to 2.23% of prewar population.

1918 flu pandemic killed around 250k more in just Britain.

WW2 killed 450,900, 0.94% of prewar population in UK and Crown colonies as well as destroying much economic infrastructure.

Covid is nasty but it's not as bad, at least so far. It's very far from being the worst crisis in the last hundred years and while there are rocks around we've seen worse and drawdown safe withdrawal rates have been set to handle them.

I note you no longer write endlessly on the topic of P2P. Can only assume that the Golden Goose didn't turn out to well.0 -

Better to take a detached open minded pragmatic view. Than focus all of ones efforts on trying the find the Holy Grail of Investing. The aim of business to make a profit and make a return to it's owners has been around since the dawn of time.cfw1994 said:

Indeed.jamesd said:

To put that into context:Thrugelmir said:The economic and financial realities of the impact of Covid are going to take time to sink in. This is by far the worst crisis in a hundred years. There can only be a rocky road ahead.

WW1 killed 867,829 to 1,011,687 in UK and colonies, 1.91% to 2.23% of prewar population.

1918 flu pandemic killed around 250k more in just Britain.

WW2 killed 450,900, 0.94% of prewar population in UK and Crown colonies as well as destroying much economic infrastructure.

Covid is nasty but it's not as bad, at least so far. It's very far from being the worst crisis in the last hundred years and while there are rocks around we've seen worse and drawdown safe withdrawal rates have been set to handle them.

Thruglemir is always a ray of sunshine & unbridled optimism on these boards, eh

For my part, I believe the world is a VERY different place than it was 100 years ago. Sure, there are and will be dips, and maybe we are entering a period of flatness, but where some businesses and sectors will struggle or fail, others will rise up.0 -

The SWR numbers take historical inflation into account (if applicable to the strategy you have chosen).Steve_PL_too said:

Out of interest ... has anyone looked at rates of inflation in the context of investment and interest rate returns? I would guess that investment returns wouldn’t be great, but I recall much higher interest rates during periods of high inflation. Just wondering what the ‘real’ margin might be?jamesd said:Looking longer term BritishInvestor used the US limiting case: sustained high inflation, which is what Bill Bengen - 4% rule person - has written worries him the most in drawdown. However:

1. around 90% of all annuities sold are level, no inflation increases.

2. defined benefit schemes normally have a portion with no inflation increases and a 5% cap is by far the most common for the rest

Those two sets, particularly the annuitants, will be severely affected by high inflation. Drawdown offers a couple or three advantages:

3. your loss isn't irreversible, you benefit from later, better, times

4. you can invest globally, potentially in places with less inflation

5. you can defer your state pension, paying yourself out of the drawdown pot while you do

Some of the safest types of income in this situation are:

6. unfunded public sector pensions, which typically have unlimited inflation increases

7. the state pension has uncapped inflation increases though it is possible in theory to change this

The state pension safety in times of high inflation is one of the many reasons why I typically suggest deferring. You can put yourself in a very secure position if it covers your core spending.0 -

Quite agree with communication and technology so different and advanced on what it was, it’s not comparing apples with apples. The world still trades, but it is a very different place.cfw1994 said:

Indeed.jamesd said:

To put that into context:Thrugelmir said:The economic and financial realities of the impact of Covid are going to take time to sink in. This is by far the worst crisis in a hundred years. There can only be a rocky road ahead.

WW1 killed 867,829 to 1,011,687 in UK and colonies, 1.91% to 2.23% of prewar population.

1918 flu pandemic killed around 250k more in just Britain.

WW2 killed 450,900, 0.94% of prewar population in UK and Crown colonies as well as destroying much economic infrastructure.

Covid is nasty but it's not as bad, at least so far. It's very far from being the worst crisis in the last hundred years and while there are rocks around we've seen worse and drawdown safe withdrawal rates have been set to handle them.

Thruglemir is always a ray of sunshine & unbridled optimism on these boards, eh

For my part, I believe the world is a VERY different place than it was 100 years ago. Sure, there are and will be dips, and maybe we are entering a period of flatness, but where some businesses and sectors will struggle or fail, others will rise up.

I tried pulling together numbers for a cashflow retirement planner as I thought my FA’s one is a bit crude and I could provide a bit more detail. In truth easier said than done though! Without seeing a complete breakdown he used growth as 3%, inflation as 2% giving a real return of 1%. The outgoings were a consistent £36k. Surely these should go up with inflation as well, unless that’s built in (maybe it is!). My state pension was £9k. Surely that will look different in 20 years time. It’s going to need some work on it all though before I am happy and can see I will have to go through several developments of it chopping and changing before I get there.

My wife’s pension should start in two years when she is 55 and is currently £173k. From a fidelity retirement calculator that suggests currently we’ll be able to drawdown £7k a year in ‘average market conditions’, the middle of their 3 choices with that money ‘running out in her nineties. It obviously doesn’t take account of her state pension as well, so a lot of things to bring together. Of there’s inheritance as well, but will leave that!1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.7K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.8K Work, Benefits & Business

- 603.3K Mortgages, Homes & Bills

- 178.2K Life & Family

- 260.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards