We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Mortgage broker - ask me anything

Comments

-

Thank you…..what I mean is any product where she could raise 100k on it with the loan being repaid from sale on her death ie with no or voluntary repayments?K_S said:

@motorman99 ‘Equity release’ has a specific meaning with respect to later life lending, but I’m assuming you mean a normal capital-raise remortgage?motorman99 said:Thanks In advance for any assistance

my wife owns a buy to let property worth 450k, outright and unencumbered. She is 79.

she wants to gift her son 100k.

can she get an equity release on this please?

If the property is tenanted (non family) then you could potentially get a capital raise remo even at 79 for the purpose of gifting to family. What options you may have will depend on the details - what personal income (if any) you have, any debt, other commitments, etc.

If you actually meant an ‘Equity release’ mortgage then yes she should definitely be able to get one though that’s a much more complex product and has a lot of implications, DYOR before going down that route.Could you point me / her in any direction on this please, as I was told by a broker that equity release no longer possible on btl.Thank you

Bob0 -

Btw…

no debt, btl unencumbered. Rent plus Oap gives income of 30k, no commitments otherwise0 -

@motorman99 The most straightforward, cost-effective way to get 100k out of the BTL would be to do a BTL capital raise remo. But you’d have a monthly interest only payment to make, probably around £400-500/month based on current rates.

If you want no payments at all, then a roll-up equity release product is what you’re looking for. I don’t do later life lending and so do not know much about it. If a later-life broker has said that that is not an option, then that is probably the case.motorman99 said:

Thank you…..what I mean is any product where she could raise 100k on it with the loan being repaid from sale on her death ie with no or voluntary repayments?K_S said:

@motorman99 ‘Equity release’ has a specific meaning with respect to later life lending, but I’m assuming you mean a normal capital-raise remortgage?motorman99 said:Thanks In advance for any assistance

my wife owns a buy to let property worth 450k, outright and unencumbered. She is 79.

she wants to gift her son 100k.

can she get an equity release on this please?

If the property is tenanted (non family) then you could potentially get a capital raise remo even at 79 for the purpose of gifting to family. What options you may have will depend on the details - what personal income (if any) you have, any debt, other commitments, etc.

If you actually meant an ‘Equity release’ mortgage then yes she should definitely be able to get one though that’s a much more complex product and has a lot of implications, DYOR before going down that route.Could you point me / her in any direction on this please, as I was told by a broker that equity release no longer possible on btl.Thank you

Bob

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

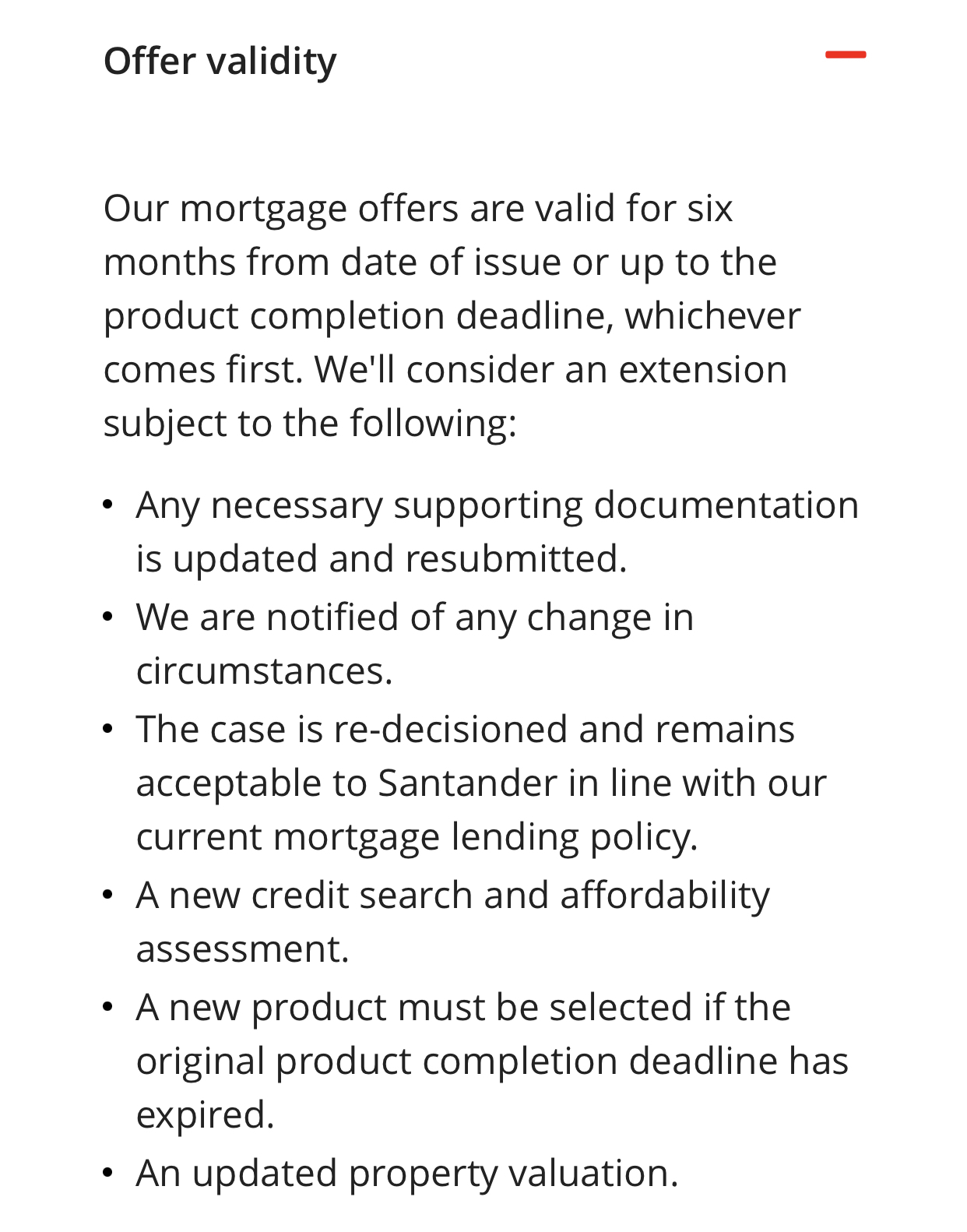

Thanks. The original product has expired is my understanding. Back to the drawing board for them I think.K_S said:

@silvercar This is their policy, you might as well re-consider re-reviewing the whole market if you have a few weeks+ to go.silvercar said:Speaking to the broker this week, but do you know Santander policy on extending a mortgage offer? Mortgage offer expires at the end of the month and it looks unlikely that exchange/ completion will happen within that time. I'm a Forum Ambassador on the housing, mortgages & student money saving boards. I volunteer to help get your forum questions answered and keep the forum running smoothly. Forum Ambassadors are not moderators and don't read every post. If you spot an illegal or inappropriate post then please report it to forumteam@moneysavingexpert.com (it's not part of my role to deal with this). Any views are mine and not the official line of MoneySavingExpert.com.0

I'm a Forum Ambassador on the housing, mortgages & student money saving boards. I volunteer to help get your forum questions answered and keep the forum running smoothly. Forum Ambassadors are not moderators and don't read every post. If you spot an illegal or inappropriate post then please report it to forumteam@moneysavingexpert.com (it's not part of my role to deal with this). Any views are mine and not the official line of MoneySavingExpert.com.0 -

Suggestions for lenders willing to lend to someone with a poor credit score. 2 missed payments in 2023 (disputing these)...these were partial payments due to a DMP recovering from financial and domestic abuse and one overdrawn account in 2019. All debts now cleared! I had DIP but my credit score dropped over night as the 2 2023 missed paymebts suddenly appeared and now mortgage application refused.

Against the property I offered on I have a 16.5% deposit0 -

Any experience on here about Buckinghamshire BS and affordability please?

I'm used to salary multiples on previous mortgages so I'd assumed 4.5x joint. However it looks as though we are potentially looking at Buckinghamshire and they seem to use affordability only. I tried their online calculator and was surprised to see quite a low amount being offered. We have no loans, credit cards, dependents or outstanding debts other than mortgage. We don't have big outgoings really, so I'm surprised. Any advice?0 -

@panpen As part of the post financial crisis reforms by the FCA, all residential lending is now based on affordability. Lenders still have LTI income multiples but they are only upper limits and not used in the affordability calculation itself except as a cap. Even with the same lender, the LTI multiple can vary across applications depending on LTV, loan size, profession, income-threshold, etc.

Very generally speaking, any of the following factors may impact your max borrowing with a particular lender - deposit/LTV, term/age/retirement-age, length of fix (usually <5 or 5+), income (and income thresholds), committed outgoings, background debt, dependents, etc etc.

With respect to Bucks BS, off of the top of my head they offer 5.5x LTI for high-income apps at low LTV. I would suggest just playing around with their calculator to figure out what the factor is that’s limiting your max borrowing. Affordability calculators are only as good as the information that is fed in so if you’ve filled it it accurately as per Bucks criteria, then the number is likely to be correct.PanPen said:Any experience on here about Buckinghamshire BS and affordability please?

I'm used to salary multiples on previous mortgages so I'd assumed 4.5x joint. However it looks as though we are potentially looking at Buckinghamshire and they seem to use affordability only. I tried their online calculator and was surprised to see quite a low amount being offered. We have no loans, credit cards, dependents or outstanding debts other than mortgage. We don't have big outgoings really, so I'm surprised. Any advice?I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

Would having one default (settled) on my credit file with a date of December 2023 look terrible if I was looking to get a mortgage in2026?Debt £7976 | Savings £350Aims: Buy first home 2026-8. £20k deposit0

-

@panpen Bucks max stated retirement age is 75 (I think) subject to plausibility. So if you’re 52 then you could try with a term of 22 years and see what it does.PanPen said:@K_S I see, many thanks. Maybe agerelated as I'm.early 50s. I have no plans to retire at 68, so could I extend term to see if that increases it? If so, will Bucks lend into my 70s?

I don't do a strenuous job.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards